B e f o r e :

HIS HONOUR JUDGE PELLING QC

SITTING AS A JUDGE OF THE HIGH COURT

Between :

____________________

Between:

| |

THE PENSIONS REGULATOR

|

Claimant

|

| |

- and -

|

|

| |

(1) PAYAE LIMITED

(2) ESTRELLA CONFERO LIMITED

(3) FRIENDLY PENSIONS LIMITED

(4) DAVID AUSTIN

(5) SUSAN DALTON

(6) ALAN BARRATT

(7) JULIAN HANSON

(8) DALRIADA TRUSTEES LIMITED

|

Defendants

|

____________________

Mr Jonathan Hilliard QC, Mr James Walmsley, Ms Elizabeth Houghton, Mr Nicholas Macklam and Mr Sam Chandler (instructed by The Pensions Regulator) for the Claimant;

The 1st to 6th Defendants did not appear and were not represented;

The 7th Defendant appeared in person on 6 December 2017 but otherwise did not appear and was not represented; and

The 8th Defendant did not appear and was not represented at trial but was represented in the proceedings by Pinsent Masons LLP

Hearing dates: 5-6 and 8 December 2017

____________________

HTML VERSION OF JUDGMENT APPROVED�

____________________

Crown Copyright ©

HH Judge Pelling QC:

Introduction

- This is the trial of a claim by the Claimant ("TPR") brought under s.16 of the Pensions Act 2004 ("PA04") by which TPR seeks to recover the whole of the sums lost as the result of what TPR characterises as an "

improper and dishonest

" pension "liberation" scheme by which approximately 245 members of occupational schemes with pension pots worth about £55,000 on average ("Members") were induced to transfer their respective pots from mainly occupational pension schemes operated by their employers ("Ceding Schemes") to schemes established, controlled or operated by the third to seventh defendants ("Receiving Schemes") by the promise that they would receive some money as a result of the transfer.

- Although the Members generally received some cash as an inducement to transfer their pension pots to the Receiving Schemes (referred to by the fourth to seventh defendants as "rebates"), the rest of the money was transferred out of the bank accounts operated in the name of the Receiving Schemes and was lost or has been expended by the eighth defendant in attempting to protect the interests of Members following its appointment as a trustee of the Receiving Schemes in the circumstances that I refer to below. In the result the Members have lost their pension pots (other than the cash sums paid to them) and have been exposed to the possibility of having to pay significant tax penalties because the sums received by them were at least arguably "unauthorised payments" within the meaning of the relevant tax legislation.

- The eighth defendant is an independent professional trustee appointed by TPR as independent trustee of the Receiving Schemes once it became aware of the matters with which this claim is concerned. Although the eighth defendant might have been expected to bring the claims against the first to seventh defendants, it does not have sufficient assets available to it to bring them. It is for that reason that TPR brings this claim and seeks by way of remedy the payment by the fourth to seventh defendants to the Receiving Schemes acting by the eighth defendant of the sums removed from the Receiving Schemes' bank accounts. The total sums claimed by TPR in these proceedings exceed £13m. The eighth defendant was joined to the proceedings by TPR but it did not appear and was not represented at the trial.

- The claims against the first to third defendants have been settled. In consequence, none of them appeared or were represented at the trial. The trial proceeded only against the fourth to seventh defendants. None of the fourth to sixth defendants appeared or were represented at the trial. Mr Hilliard QC made it clear that TPR did not seek to rely on the non-appearance of the fourth to sixth defendants as supporting any element of TPR's case. Accordingly, I leave it out of account. The seventh defendant appeared only for the second day of the trial in the circumstances I set out in more detail below. The result of the non-appearances of the first to sixth defendants and the limited participation of the seventh defendant was that the trial was completed in 3 days although originally scheduled to take 8 days.

- As I explain below, dishonesty is not a necessary ingredient of the cause of action created by PA04, s.16 but TPR's case has been advanced on the basis that the fourth to seventh defendants have acted dishonestly and it asks that I determine this case on the basis of those allegations. TPR has adopted this course because they wish any judgment they obtain against the individual defendants to come within the scope of s.281(3) of the Insolvency Act 1986 ("IA86").

- As already mentioned, the seventh defendant appeared on the second day of the trial, when he elected to give oral evidence and was cross examined. He informed me at the end of his evidence that he did not intend to further attend the trial or to make any closing submissions see T3/129/12 130/12, where he indicated that in relation to the scheme he was concerned with he "

didn't know what was happening" by which I understand him to deny dishonesty as alleged against him whilst accepting that he was involved in the misappropriation that I describe and make findings about later in this judgment.

- It was only shortly before the trial started that it became clear that the fourth defendant (described by Mr Hilliard as the "ring leader") would not appear at the trial. Although he had previously provided an admission but indicated he intended to appear at the trial, the fourth defendant subsequently indicated he wished to withdraw his admission but would not attend the trial. Although there was no formal application made by the fourth defendant to withdraw his admission, it was not opposed by TPR and I acceded to it for reasons I set out in a ruling I delivered on the first day of the trial.

- The seventh defendant did not appear on the first day of the trial. That being so, I invited Mr Hilliard to summarise early in his oral opening submissions those parts of the evidence tendered by TPR in relation to the claim against the seventh defendant. I then summarised the steps that the seventh defendant would have to take if he wished to challenge that evidence. This was all set out on the live transcript that was being taken. I directed that a copy of the relevant part of the transcript should be sent to the seventh defendant by email by TPR's solicitors as soon as possible that day. In the result, the seventh defendant attended the second day of the trial, the witnesses relevant to the claim against the seventh defendant (Ms Edwards and Mr Tyrrell) were tendered for cross examination and the seventh defendant cross examined those witnesses on a limited basis. The seventh defendant then gave evidence and was cross examined. Save for the evidence relevant to the claim against the seventh defendant all the other evidence relied on by TPR was admitted unchallenged.

- I accept the evidence of TPR's witnesses in so far as that evidence was not challenged and I accept the evidence of Ms Edwards and Mr Tyrrell in relation to the claim against the seventh defendant. I return to the evidence of the seventh defendant as necessary in more detail below.

The Relevant Legal Principles

The Substantive Law

- PA04, s.16 provides that:

"If, on the application of the Regulator, the court is satisfied that there has been a misuse or misappropriation of any of the assets of an occupational or personal pension scheme, it may order any person involved to take such steps as the court may direct for restoring the parties to the position in which they were before the misuse or misappropriation occurred."

By PA04, s.16(2), a person is "involved" if he appears to the court to have been "

knowingly concerned in the misuse or misappropriation of the assets". PA04, s.16 confers on TPR standing to commence proceedings in relation to the misuse or misappropriation of the assets of a relevant pension scheme which it would not otherwise have because it is not the trustee of any such schemes. In this case it enables TPR to pursue those knowingly concerned with such misuse or misappropriation where the trustee of the scheme or schemes concerned is unable to do so.

The Need To Prove Dishonesty

- Although in this case TPR has chosen to present its case on the basis that the first to seventh defendant have been dishonestly involved in the misuse or misappropriation relied on, Mr Hilliard submits that dishonesty is not a necessary ingredient of a claim under PA04, s.16.

- I accept that submission. Although the concept of being "knowingly concerned

" might suggest such a requirement, just as it does in the context of accessory liability for breach of trust, in my judgment construing PA04, s.16(2) as imposing such a requirement would defeat in part the purposes for which it was enacted. The purpose of PA04, s.16 is to enable TPR to pursue all persons involved in either the misuse or misappropriation of scheme assets. That necessarily includes former trustees or others who have misused assets without dishonesty. If PA04, s.16(2) is construed as importing a requirement for dishonesty by use of the word "knowingly" that would preclude claims being made against former trustees who have misused assets without dishonesty. That cannot have been intended to be the outcome. A scheme trustee would be entitled to bring such a claim. There is no obvious reason why TPR should be more fettered in the claims that it can bring under PA04, s.16 than a scheme trustee would be when making a claim for breach of trust, particularly when TPR is likely to bring PA04, s.16 proceedings only where the scheme trustee is unable or unwilling to do so through a lack of funds. In my judgment the effect of the word "knowingly" is merely to import a requirement that the defendant concerned should know of the facts that make his or her actions a misuse or misappropriation not that his or her actions constituted a misuse or misappropriation.

- Construing PA04, s.16 in this way does not expose trustees who have misused assets without dishonesty to claims that could not succeed if brought by a scheme trustee. Such a former trustee will be entitled to rely on exoneration provisions within scheme rules in relation to a claim by TPR under PA04, s.16 to the same extent and in the same circumstances as would such a former trustee when facing a claim for breach of trust by a scheme trustee. Similarly, persons against whom PA04 s.16 claims are brought will be entitled to rely on statutory relief provisions such as that contained in s.61 of the Trustee Act 1925 and s.1157 of the Companies Act 2006.

The Ingredients of a PA04 s.16 Claim

- If a claim under PA04 s.16 is to succeed it is necessary for TPR to prove on the balance of probabilities that:

(a) that the assets that it is alleged have been misused or misappropriated were assets of an occupational or personal pension scheme ("the Asset Requirement");

(b) that what it is alleged the defendants did or failed to do was a misuse or misappropriation of an occupational or personal pension scheme assets ("the Act Requirement"); and

(c) the defendant concerned was a person involved in the misuse or misappropriation alleged ("the Involvement Requirement").

In this case TPR alleges that, aside from the sums paid to the Members, the whole of the Members' pension pots were either misused or misappropriated by transfer out of the Receiving Schemes' bank accounts other than for the purposes of administering the Receiving Schemes in the ordinary course or have been expended by the eighth defendant in attempting to recover what has been inappropriately removed. As Mr Hilliard put it in his written opening submissions, the Receiving Schemes were thus "

denuded of the money transferred into them and the individuals who were persuaded to transfer their pensions have, as things stand, lost their pensions altogether". The Act Requirement is alleged to have been satisfied by the removal of the Members' pension pots from the Receiving Schemes' bank accounts. The Involvement Requirement is alleged to be fulfilled by the defendants' involvement in those removals.

The Dishonesty Test where Dishonesty is Alleged

- As I have said, notwithstanding that there is no necessity for TPR to prove dishonesty, it has chosen to advance its case on the basis that each of the fourth to seventh defendants was not merely concerned in the misuse or misappropriation alleged but that they were each dishonestly concerned in such conduct. It is now clear that the test for dishonesty is the same in all civil and criminal proceedings where such an allegation is made see Ivey v. Genting Casinos (UK) Limited trading as Crockfords [2017] UKSC 67 ("Ivey") at paragraph 63. For dishonesty to be established it is necessary first to establish (subjectively) the knowledge or belief of the person concerned as to the relevant facts and then to determine (objectively) whether the person's conduct was honest by applying the standards of ordinary decent people see Ivey (ante) at paragraph 74. In a context such as this, it requires the defendant's knowledge of the transaction concerned to be such as to render his participation contrary to ordinary standards of honest behaviour see Barlow Clowes International Limited v. Eurotrust International Limited [2005] UKPC 37, [2006] 1 WLR 1476 at paragraphs 15-16.

Evidential Issues

- As I have said already, TPR's evidence against all save the seventh defendant has not been challenged. In considering the factual issues as between the seventh defendant and TPR that are material to this dispute I have approached those issues by testing the evidence of each of the witnesses wherever possible against contemporary documentation, admitted and incontrovertible facts, and inherent probabilities. This is entirely conventional - see Onassis and Calogeropoulos v. Vergottis [1968] 2 Lloyds Rep 403 at 407 and 431 and is particularly appropriate where (as here) the allegations relate to events that occurred some years ago and the oral evidence is based on recollection of such events - see Gestmin SGPS SA v. Credit Suisse (UK) Limited [2013] EWHC 3560 per Leggatt J at paragraphs 15-22.

- TPR having chosen to advance its case on the basis that the defendants have been dishonestly involved in the misuse and misappropriation alleged, I remind myself of, and apply, the following general principles. First, the legal and evidential onus of proof rests throughout on TPR to prove on the balance of probabilities the allegations it relies on. Secondly, whilst the standard of proof in a civil case is always the balance of probabilities, the more serious the allegation, or the more serious the consequences of such an allegation being true, the more cogent must be the evidence if the civil standard of proof is to be discharged see Re H (Minors) (Sexual Abuse: Standard of Proof) [1996] AC 563 per Lord Nicholls at 586, where he said:

"'The balance of probabilities standard means that a court is satisfied that an event occurred if a court considers that on the evidence the occurrence of the event was more likely than not. In assessing the probabilities, the court will have in mind as a factor to whatever extent it is appropriate in the particular case that the more serious the allegation the less likely it is that the event occurred and hence the stronger should be the evidence before court concludes that the allegation is established on the balance of probabilities. Fraud is usually less likely than negligence

Built into the preponderance of probabilities standard is a generous degree of flexibility in respect of the seriousness of the allegation.'"

Finally, it is necessary to remember that it does not necessarily follow from the fact that a witness has been shown to be dishonest in one respect that his evidence in all other respects is to be rejected. Experience suggests that people may give dishonest answers for a variety of reasons including an entirely misplaced wish to strengthen a true case that is perceived to be evidentially weak as opposed to a desire to advance a dishonestly conceived case in a dishonest manner. What such conduct will usually mean however is that the evidence of such a witness will have to be treated with great caution save where it is corroborated, either by a witness whose evidence is accepted or by the contents of contemporaneous documentation, or is against the witness's interests or is admitted.

The Facts

The Claims in Summary

- The issues that arise in relation to each of the fourth to seventh defendants are (a) whether Receiving Scheme assets were misused or misappropriated, (b) whether each of the fourth to seventh defendants were involved in such misuse or misappropriation and (c) if they were, whether they or any of them were dishonestly involved in such misuse or misappropriation. Applying the principles set out above, I am satisfied that TPR has each of these elements against each of the fourth to seventh defendants. My reasons for reaching that conclusion are set out below.

- This claim is concerned with activity concerning a total of 11 Receiving Schemes that fall into three broad categories. There were a number of other schemes identified in the Re-amended Particulars of Claim ("PoC") but they are not relevant to this trial.

- The first group of Receiving Schemes are referred to in these proceedings as "the Barratt Schemes". They are so called because the sixth defendant ("Mr Barratt") was either a trustee or the sole trustee of each of the Barratt Schemes until the eighth defendant was appointed in his stead. The Barratt Schemes consisted of (a) the Callahan Consulting Pension Scheme ("Callahan"), (b) the Daycroft Pension Scheme ("Daycroft"), (c) the Fort Bruce Pension Scheme ("Fort Bruce"), (d) the Gresham Investment Pension Scheme ("Gresham"), (e) Gresham 2012 Pension Scheme ("Gresham 2012") and (f) the Western Cross Pension Scheme ("Western Cross").

- The second group of schemes are referred to as "the Dalton Schemes". They are so called because the fifth defendant ("Ms Dalton") was either a trustee or the sole trustee of each of the Dalton Schemes until the eighth defendant was appointed in her stead. The Dalton Schemes consisted of (a) the Abbey Mage Pension Scheme (Abbey Mage"), (b) the Dellaney Gibbons Pension Scheme ("Delaney Gibbons"), (c) the Regency Pension Investments Pension Scheme ("Regency") and (d) the Williams Bell Pension Scheme ("Williams Bell").

- The third category consists of a single fund called the Friendly Pensions Retirement Scheme ("FPRF"). The sole trustee of the FPRF was a corporate trustee called Friendly Trustees Limited ("FTL") until the eighth defendant was appointed in its stead. The seventh defendant ("Mr Hanson") was the sole director of FTL between 15 July 2014 and its dissolution on 9 June 2015. Its sole shareholder was the fourth defendant.

- TPR alleges that the fourth defendant ("Mr Austin") controlled the activities of both Mr Barratt and Ms Dalton while they respectively acted as sales agents and while they acted as trustees of the Receiving Schemes. In their sales agent capacity, their role was to procure Members to transfer their pension pots from a Ceding Scheme to one of the Receiving Schemes by offering the rebates. Although routed to Members via other entities, in reality these payments were financed either by cash taken from the Receiving Schemes or from commissions payable to the Receiving Schemes in respect of investments made using Receiving Scheme money. TPR alleges that those investments were entirely inappropriate for reasons that I expand upon later in this judgment. It is alleged that there was a fundamental conflict between the role of sales agent and that of trustee. It is alleged that Mr Hanson was controlled or heavily influenced in his activities by Mr Austin.

- The losses that have been suffered from the Receiving Schemes in summary break down into four broad categories of loss. First, certain sums were transferred from the Receiving Schemes bank accounts to Mr Barratt and Ms Dalton personally Mr Barratt received sums totalling £245,550 directly from the Receiving Schemes and Ms Dalton received sums totalling £72,986.20 from the Receiving Schemes. These are alleged to have been payments made in breach of trust that were not justifiable as payments of fees.

- Secondly, most of the money received into the Receiving Scheme bank accounts were transferred to two companies controlled by Mr Austin being (a) Friendly Investments Company Limited ("FIC"), a company formed by Mr Austin ostensibly as an investment company that was placed in liquidation by reason of its insolvency in June 2015 and (b) Friendly Pensions Limited ("FPL"), a company formed by Mr Austin in 2014 that was placed in creditors voluntary liquidation on 23 December 2015. It is necessary to note in passing that in 2014 a Mr Nick Ayton became involved with FPL first as a director and then a shareholder. This ended in a dispute between him and Mr Austin. Between them FIC and FPL received £5.595m from the Barratt Schemes and £4.795m from the Dalton Schemes. TPR alleges that Mr Austin had control of the Barratt and Dalton scheme accounts through his control of Mr Barratt and Ms Dalton and that he procured the transfer of these sums to FIC and FPL without any consideration being given as to whether such transfers were appropriate investments for pension schemes.

- Thirdly, sums totalling £1,460,412 were transferred from the Barratt Schemes and £500,000 from the Dalton Schemes for investment in a property development in St Lucia and in a commercial property bond. It is alleged that both were inappropriate investments and that each was made without the trustees considering whether they were appropriate investments to make. Significant parts of the commission generated by these investments and the payments referred to in the previous paragraph ended up either in the hands of Mr Austin or his family members (via a number of subsidiary transfers) or funding payments to the Members as promised following the transfer of their pension pots.

- Finally, £120,000 was transferred by FPRF to Broadbridges Consulting Limited ("Broadbridges"), another corporate vehicle controlled by Mr Austin, at least in part for the purpose of enabling Mr Austin to fund his litigation with Mr Ayton. It is alleged that there was and could be no justification for such conduct.

- TPR claims against Mr Austin the whole of the sums credited to the Receiving Schemes bank accounts from the Ceding Schemes (£13,737,202.10), against Ms Dalton the whole of the sums credited to the Dalton Schemes bank accounts (£5,900,947), against Mr Barratt the whole of the sums credited to the Barratt Schemes bank accounts (£7,713,317.71) and against Mr Hanson the whole of the sum credited to the FPRF bank accounts. (£122,937.37). Although this includes sums remaining credited to the accounts at the date when the eighth defendant was appointed trustee of the Receiving Schemes, it is submitted that the fourth to seventh defendants are liable for the costs of attempting to correct the alleged misuse and misappropriation and those sums have been expended in that activity.

The Asset Requirement

- For a s.16 claim to succeed, TPR must prove on the balance of probabilities that the assets that it is alleged have been misused or misappropriated were assets of an occupational or personal pension scheme. None of the defendants other than Mr Hanson disputes that the Receiving Schemes were occupational pension schemes within the meaning of PA04, s.16. Mr Hanson puts TPR to strict proof that FPRF is such a scheme. I find that TPR has proved this element of its claim for the reasons set out in paragraphs 30-40 below.

- S.318 of PA04 defines an occupational pension scheme as having the same meaning given to that phrase by s.1 of the Pension Schemes Act 1993 ("PSA93"). S.1 of PSA93 defines an occupational pension scheme as being a "pension scheme":

"(a) that

(i) for the purpose of providing benefits to, or in respect of, people with service in employments of a description, or

(ii) for that purpose and also for the purpose of providing benefits to, or in respect of, other people,

is established by, or by persons who include, a person to whom subsection (2) applies when the scheme is established or (as the case may be) to whom that subsection would have applied when the scheme was established had that subsection then been in force,

"

A "pension scheme" for these purposes is defined by s1(5) as meaning:

"

a scheme or other arrangements, comprised in one or more instruments or agreements, having or capable of having effect so as to provide benefits to or in respect of people

(a) on retirement,

(b) on having reached a particular age, or

(c) on termination of service in an employment."

S.1(2) and (3) provides that:

"This subsection applies

(a) where people in employments of the description concerned are employed by someone, to a person who employs such people,

(b) to a person in an employment of that description, and

(c) to a person representing interests of a description framed so as to include

(i) interests of persons who employ people in employments of the description mentioned in paragraph (a), or

(ii) interests of people in employments of that description.

(3) For the purposes of subsection (2), if a person is in an employment of the description concerned by reason of holding an office (including an elective office) and is entitled to remuneration for holding it, the person responsible for paying the remuneration shall be taken to employ the office-holder."

- Where the founder of the relevant scheme is a limited company which had a director at the point in time when the scheme was established and the director was in an employment of the description concerned then that person is a person to whom s.1(2)(a) applies see Pi Consulting (Trustee Services) Limited v. TPR [2013] Pens LR 433 per Morgan J at paragraphs 71-72. In other words, as long as there is a director of the company establishing the scheme at the date when the scheme is created who is eligible under the scheme the requirements of s.1 is satisfied. There is no evidence here that any of the directors of the founding companies were entitled to remuneration so s.1(3) is not satisfied but that does not matter for present purposes for the reasons identified by Morgan J at paragraphs 68-71 of his judgment in Pi Consulting (ante).

- Whether a scheme has been established for a purpose identified in s.1 is to be judged objectively from the scheme's terms and rules rather than the subjective intentions of the founder see Pi Consulting (ante) per Morgan J at paragraphs 39-41. However, it is important to note that that conclusion was based in part on a concession by counsel for TPR that was qualified by an assumption that the documents creating the schemes were not shams and on the agreement by all parties (recorded in paragraph 38 of the judgment) that the relevant scheme was genuinely recorded in the documents relating to it. In this context "sham" has the meaning accorded to it by Diplock LJ in Snook v. London and West Riding Investments Limited [1967] 2 QB 786 at 802:

"it means acts done or documents executed by the parties to the "sham" which are intended by them to give to third parties or to the court the appearance of creating between the parties legal rights and obligations different from the actual legal rights and obligations (if any) which the parties intend to create. But one thing, I think, is clear

that for acts or documents to be a "sham," with whatever legal consequences follow from this, all the parties thereto must have a common intention that the acts or documents are not to create the legal rights and obligations which they give the appearance of creating. No unexpressed intentions of a "shammer" affect the rights of a party whom he deceived."

It is not in any sense a necessary ingredient of the allegations made by TPR in this case that the scheme documents should be regarded as shams and no such allegation is made by TPR see Transcript, Day 1, page 40, lines 21-22. None of the defendants make such an allegation. In my judgment, it would have to be clearly and distinctly alleged in the pleadings and proved that the documents were shams before I could conclude that they were. It follows that I proceed on the basis that the scheme documentation genuinely records the schemes concerned.

- Given Mr Hanson's position in relation to FPRF I turn to the detail concerning that scheme first. The FPRF scheme is contained in a document that purports to be a deed made between FPL and FTL dated 28 June 2014. The document is executed but the signatures of those signing have not been witnessed and thus technically the document cannot be a deed see s.1(3) of the Law of Property (Miscellaneous Provisions) Act 1989. In my judgment, this is immaterial. There is no formal requirement imposed by either the PA04 or the PSA93 (or any of the other relevant statutory provisions that have been drawn to my attention) or the general law which requires the scheme to be contained in a deed before it can be valid. In those circumstances, it is unnecessary to consider further the position had there been such a requirement. That is so because a trust can be created informally in the absence of a statutory requirement of formality see Snell's Equity 33rd Ed., Paragraph 22-035.

- It is now necessary to consider the terms of the FPRF Scheme document in order to test whether objectively the scheme was established for a purpose set out in PSA93 s.1. The sponsor (that is the entity establishing the scheme) is FPL. It was incorporated on 20 March 2012 with its sole shareholder and director being Mr Austin. He was a director of the company on 28 June 2014 (the date when the FPRF scheme was established as explained in paragraph 33 above). He ceased to be a director on 12 July 2014. He was thus a director at the date when the FPRF scheme was established.

- The purpose of the scheme is described in clause 1.1 as being "

to provide relevant benefits

for such Employees and Connected Persons of the Sponsor and other Employees and such other persons as may be permitted by the Revenue as shall be admitted to participation in the Scheme". Those eligible to join are further defined in clause 7.1 as being "

all Employees

" and "Employee" is defined in clause 77 as meaning "an employee or other jobholder of an Employer or a director of an Employer whose remuneration is not a receipt of a profession or accountable to another employer or company". "Employer" is defined as being the Sponsor or any other participating employer. The qualification to the definition of director is not alleged to be of any application to Mr Austin. It does not mean that a director has to be remunerated if he or she is to be eligible. It means merely that to be eligible any remuneration receivable must not a professional fee or accountable for to another employer or company. This is consistent with Morgan J's analysis in Pi Consulting (ante) and recognises that it would be open to a director not receiving remuneration to transfer his occupational pension pot to a Scheme established by a company of which he was a director. It follows that he was an Employee at the date when the scheme was established by reason of him being a director of FPL and for that reason the requirements of PSA93, s.1 are satisfied in relation to the FPRF scheme, which in consequence I find was an occupational pension scheme for the purposes of PA04, s.16.

- I now turn briefly to the other schemes. I do so briefly because as I have explained none of the defendants other than Mr Hanson have put in issue the validity of the schemes that concern them and Mr Hanson is concerned only with the FPRF scheme.

- Mr Hilliard has very properly drawn to my attention various issues concerning the documentation of the various schemes. These fall into three categories. First some of the scheme documents purport to be deeds but do not comply with the technical requirements for deeds by reasons of the absence of witnesses. I need say no more about that since it is immaterial to the validity of the schemes concerned for the reasons set out above in relation to the FPRF documentation.

- Secondly, there are some backdating issues where documents have been executed after the date when they purported to take effect. Nothing of itself turns on this unless it could be said that the formal requirements contained in PSA93 were not satisfied on either the date when the document was executed or the date to which it was backdated. No such situation has been drawn to my attention either in the written or oral submissions made on behalf of TPR or in Schedule A to the PoC, where the issues I am now considering have been summarised in relation to each scheme.

- Thirdly, in relation to the first deeds for the Gresham and Regency schemes (the first Barratt and the first Dalton Scheme respectively), no rules have been attached. This is relevant for present purposes only if it renders the scheme not an occupational pension scheme applying the principles already considered in detail in relation to the FPRF scheme or too uncertain to be capable of constituting a trust. This is not the effect of the omission because I accept Mr Hilliard's point summarised in section (2) of Footnote 26 to his written opening submissions and expanded upon orally (see Transcript, Day 1, pages 50-52) namely that even if the relevant deeds are construed as standalone documents they are sufficiently certain in their effect to mean they are not void.

- Even if this last conclusion is wrong it does not matter because I also accept his submission that that would have not have provided a defence based on a failure to satisfy the Asset Requirement because the Ceding Schemes were without doubt occupational or personal pension schemes, the pension pots were intended to be transferred only to a Receiving Scheme that was a valid occupational pension scheme and if the Receiving Scheme was not such a scheme then the funds received would have been held either on resulting or a Quistclose[1] trust and therefore remained occupational pension scheme assets held on trust for the Ceding Scheme trustees unless and until transferred to a valid Receiving Scheme. In those circumstances I am satisfied and find that the Asset Requirement is satisfied in respect of each element of the claims.

Validity of Transfers In

- None of the defendants assert that the Members transferring in their pension pots did so invalidly. Mr Hilliard however very properly drew attention to the questionability of Members signing contracts of employment with shell companies as a mechanism for fulfilling this requirement in relation to the Receiving Schemes. I suggested to Mr Hilliard in the course of his opening that these contracts were shams in the sense identified above and he agreed see Transcript, Day 1, page 53, line 14 to page 54 line 5. They were shams because to the knowledge of both parties they did not reflect reality. The company concerned was almost invariably a shell company and the Member was not in reality employed by it.

- In my judgment, this point does not provide a defence to any of the defendants. First, taking the FPRF scheme as an example, clause 68.1 of the Scheme rules permits transfers in from "

any other person [who] was previously a member of a Registered Pension Scheme

" irrespective of whether they were an employee or former employee of the sponsor. Secondly that scheme's rules provided that the scheme was established for the benefit not merely of "Employees" but also "Connected Persons" who were defined by clause 77 to mean "

any other person whom the Trustee may permit to contribute to the Scheme

". The scheme rules were thus drawn so widely as to permit Members to validly transfer into the FPRF scheme so long as either they had previously been a member of a registered scheme or otherwise were permitted to contribute by the trustee of the scheme. This formulation is reflective of the machinery of each of the other schemes with the possible exception of those where no rules were attached to the Scheme Deeds. In relation to the latter (and if, for any reason, I am wrong about what I have so far said in relation to the other schemes concerning validity of transfer) the resulting or Quistclose trust analysis set out above would apply with the result that the funds received would be held on trust for the Ceding Scheme trustees unless and until the fund was validly transferred to a Receiving Scheme.

The Act and Involvement Requirements Barratt and Dalton Schemes

- The issues I now turn to concern whether what was done or not done with Barratt and Dalton Receiving Scheme assets was a misuse or misappropriation within the meaning of PA04, s.16 and whether Mr Austin, Ms Dalton and Mr Barratt were persons involved in such misuse or misappropriation. For the reasons set out in paragraphs 44-82 below, I find that TPR has proved each of these elements against each of these defendants.

- The concepts of misuse or misappropriation are disjunctive and are each potentially extremely wide. This is not the occasion to attempt to define comprehensively what comes within the scope of each and it may be that attempting to do so should be avoided since by so doing the scope of the words used in the legislation may be inappropriately narrowed. It is sufficient for present purposes to say only that I am satisfied that dealing with scheme assets in breach of trust comes within the scope of the words used as does the transfer of scheme assets without the authority of the trustees as does directing a trustee to make, or misleading a trustee into agreeing to, a transfer that is in breach of trust.

- It is necessary to describe in some detail the way in which the liberation business was operated because that provides much of the context in which the actions of the fourth to sixth defendants must be judged.

- Initial contact was made with Members via a lead generation operation which operated using a variety of cold calling and web based techniques. Although Mr Austin denies that he "

masterminded the process

" or that he knew how prospective leads were generated see paragraph 20G(2)(ii) of his amended Defence, where he asserts that he "cannot comment" on how prospective transferees were procured because "

all the introducers operated out of their own business premises

" that is plainly not true for the reasons set out in paragraphs 68 and following of Mr Hilliard's written opening submissions. One of the lead generators was Select Pension Investment Limited ("SPI"), a company controlled by Mr Austin for which both Mr Barratt and Ms Dalton worked as sales agents. Indeed SPI is one of the generators that Mr Austin refers to expressly in paragraph 20G(2)(ii) of his amended Defence.

- As Mr Austin asserts, SPI operated from an office in Spain. However, Mr Austin was clearly linked with that company. Not only was Camilla Austin (Mr Austin's daughter) made a sole director of the company from 2 January 2014, but as early as November 2012, Mr Austin was setting out detailed proposals on behalf of SPI concerning the conduct of lead generation. That much is apparent from the subject heading of an email of that date from Mr Austin to a third party lead generator controlled by Mr Chorlton entitled "Providing Leads" which included the statement that the "

company that you will be having the introducer agreement with is [SPI]

" the size and importance of the business is apparent from Mr Austin's description of the likely fee income that would be generated for Mr Chorlton's company:

"

on the numbers that we talked about if you get a 5% response to your 120000 successful PPI claimants then that is 6000 clients with an av pension size of £20k is £120m of potential total investment. 10% of that (your introducer fee) is £12m

"

The email then went on to describe in detail how to script the calls for call centre staff. I accept Mr Hilliard's submission that it is clear from at least this time that Mr Austin was heavily involved in negotiating introducer arrangements on behalf of SPI.

- Once a lead had been generated sales agents then attempted to persuade persons identified as leads to transfer their pension pots from Ceding Schemes, to the Receiving Schemes. This business was carried out by SPI by individual sales agents paid on a commission basis. The sales agents included Mr Barratt, Ms Dalton and Max Ayton, the son of the Mr Ayton referred to above). Mr Austin was heavily involved in that part of the business as is apparent for example from (a) the fact that he devised at least one of the sales scripts used by SPI's sales agents and (b) the fact he gave direct instructions to the sales agents see by way of example the emails of 26 April 2013, 1 May 2013 (addressed to Mr Barratt in his capacity as a sales agent), 23 May 2013, 12 June 2013 and 15 August 2013. It is apparent too from the exchange of emails on 30 May 2013, when Ian Mitchell of FPL sought guidance from Mr Austin as to how to respond to questions being asked by potential transferring Members concerning the activities of the Receiving Schemes. Mr Austin not only agreed that Mr Mitchell should ask for the questions in writing but asked Mr Mitchell to "

run them past me when you get them". Mr Austin controlled what information was passed to prospective transferring Members see by way of example the exchange of emails between Mr Ayton and Mr Mitchell copied to Mr Austin on 21-22 August 2013 from which it is clear that the information that Mr Max Ayton is authorised to supply has been authorised only following a conversation between Mr Mitchell and Mr Austin.

- A key feature of the way in which Members were persuaded to transfer their pension pots to Receiving Schemes was payment of a financial inducement to transfer, which the defendants referred to in their internal correspondence as "rebates". This element of the scheme was structured so as to ensure that it was concealed from any of the persons or individuals who might stop the transfers from taking place that is Ceding Scheme trustees and administrators and any Independent Financial Advisors who might become involved. It was this that led Mr Mitchell to propose and Mr Austin to at least impliedly approve directions to sales agents that included a direction not to include on the systems they used records that "

divulge any information relating to the deals that have been made between agent and the client. The notes that we keep on the system will also be called upon should we be subject to investigation by the Pensions Regulator

". This was reiterated from time to time in instructions given by Mr Austin to agents including Mr Barratt and Ms Dalton see by way of example the email of 23 May 2013 from "Jane" (in fact Mr Austin as I explain in more detail below) where he outlined a scheme for transferring funds from Ceding Schemes to SIPPs rather than Receiving Schemes in order to overcome objections from Ceding Schemes. Having outlined how the mechanism would work, Mr Austin then reminded the recipients (including Ms Dalton and Mr Barratt) that such a transfer would require advice from a IFA and then added "

Client needs to make sure of course that they do not mention commission sharing arrangement to IFA otherwise case will be dead". The "commission sharing arrangement" was another euphemistic way of describing payments back to Members. This approach was of course critical because the payments to Members were in reality at least arguably unauthorised payments and IFAs would be bound to advise clients that such was the case. Such payments are also a badge of liberation fraud and thus likely to trigger negative advice from IFAs.

- The third stage in the process was the administration of the transfer of Members' pension pots from the Ceding Schemes to the Receiving Schemes. This too was led by Mr Austin. Three aspects of this process demonstrate this to be so. Much of the day to day transfer administration was managed by Mr Mitchell on the instructions of Mr Austin. From early 2013, the administration team managed by Mr Mitchell operated using FPL as the vehicle. First, it was Mr Austin who gave instructions concerning which email accounts were to be used by the transfer administration team see Mr Austin's email to Mr Mitchell of 29 April 2013, the terms of which are clearly consistent only with Mr Austin having ultimate control.

- Secondly, Ceding Schemes would occasionally raise concerns relating to the transfer of a Member's pension pot to a Receiving Scheme. Email traffic between Mr Mitchell and Mr Austin show Mr Austin to be drafting complaint letters or directing the administration to send such letters, advising on the tactics to be used in relation to such letters see by way of example the email exchange between Mr Mitchell and Mr Austin on 5 August 2013 in which a deliberately deceptive approach to such letters was suggested by Mr Austin and agreed by Mr Mitchell - and of him being sent different versions of such letters prepared by Mr Mitchell "

so the companies are not receiving the same letter over and over". Mr Mitchell would not be sending such an email and attachments to Mr Austin unless it was Mr Austin who was controlling what happened.

- Finally, as explained by reference to the terms of the Receiving Scheme rules, the Receiving Schemes were structured so as ostensibly to be schemes for employees of the scheme sponsor although in fact transferring Members were never employees of the Receiving Schemes' sponsors. In fact, the scheme sponsor was invariably a shell company which in reality had no business and no employees. In order to persuade some Ceding Scheme administrators and trustees of the bona fides of the Receiving Scheme, employment contracts were drawn up by which it appeared that the transferring member was an employee of the sponsor of the Receiving Scheme. As noted above, these employment contracts were shams in the sense defined earlier in this judgment. Mr Austin orchestrated this entirely deceptive process see by way of example the exchange of emails of 23 April 2013 which should be read in the context of the email from Ms Lisa Tirrell, a Ceding Scheme administrator to the transferring Member dated 22 April 2013.

- In the light of this material (which is by way of example only) I accept Mr Hilliard's submission that Mr Austin was fully in charge of the administration team. The reality was reflected in an email that Mr Austin sent to Mr Mitchell dated 29 April 2013 by which he instructed Mr Mitchell "When you are sending emails you need to cc me in on all of them please" and his email to the whole team dated 31 May 2013 saying " Ian [Mitchell] needs to take you all out today for an expensive lunch on me to celebrate the end of the month" when coupled with the emails that precede it in the string dated 29 and 31 May 2013 in which Mr Mitchell and one of the administration team report on the completion of transfers of two pots into Receiving Schemes. It is reflected too in Mr Austin's email of 28 April 2013 to Alan Fowler (a lawyer then assisting in amending the Receiving Schemes' trust deeds). In it Mr Austin described Ian Mitchell as "

my manager in London dealing with scheme administration

".

- Two remaining elements of the business that is the subject of this claim remain to be considered the establishment of the Receiving Schemes and the management of their bank accounts. Although a significant amount of material has been deployed in relation to what became of the money after it left the Receiving Scheme accounts, I regard that as largely immaterial to the issues I have to decide other than to the extent it demonstrates that the transfers out of the Receiving Scheme accounts were not made in the ordinary course of administering an occupational pensions scheme, throws light on the roles played by the fourth to seventh defendants and impacts on the dishonesty issues that arise.

- The various Barratt and Dalton Schemes were established in a period between late 2012 and mid-2013. I have already noted the wide terms in which those schemes' membership class was defined. The membership of each Receiving Scheme never exceeded 100 members see by way of example Mr Austin's email to Mr Fowler (as already noted, a pensions lawyer retained by Mr Austin) concerning Gresham 2012 dated 13 March 2013. Investment regulations do not apply to schemes with less than 100 members as they do to schemes with more than 100 members.

- Mr Austin was clearly in control of the establishment and management of the Receiving Schemes. So for example, it was Mr Austin who met with Mr Fowler to discuss trust deeds for the schemes and to whom advice was given by Mr Fowler concerning the schemes and their operation see by way of example the emails between him and Mr Fowler of 13 March 2013 (concerning Gresham 2012) and 15 March 2013 (concerning investment of Gresham 2012 scheme funds in a loan to FIC), 17-22 March 2013 (concerning a draft new form of trust deed and rules for use by the Receiving Schemes) and 28 and 29 April 2013 (concerning the number of trustees that each scheme should have) and it was to Mr Austin and Mr Mitchell that Mr Fowler provided advice see by way of example his email to them dated 30 April 2013. It was Mr Austin who paid Mr Fowler's fees see the email from Mr Austin to Mr Fowler of 26 March 2013. That Mr Austin was in control, is also demonstrated by the reporting email from Mr Mitchell to Mr Austin of 17 April 2013 and the apologies email from Mr Mitchell to Mr Austin of 10 August 2013.

- It is necessary now to consider the role of Ms Dalton and Mr Barratt. As I have explained already, their primary role was that of SPI sales agents for which they received commission in respect of every lead where the member concerned was persuaded by the agent concerned to transfer his or her pension pot to a Receiving Scheme. Since the new Receiving Schemes required trustees and the sponsoring companies directors, they were asked to take on those roles by or on behalf of Mr Austin but thereafter simply did his bidding. Although this is denied by Mr Austin, both Mr Barratt and Ms Dalton assert that is what happened. Since their assertions are against their respective interests and is supported by the documentation that is available I prefer what they assert over what Mr Austin asserts.

- In paragraph 20G(1) of her amended Defence, Ms Dalton pleads that:

"Mr Austin placed me in a position where I was "asked" to be a Trustee with no option."

In paragraph 39(5) she adds that:

"

I wasn't lending my name as a Trustee, I was acting as a Trustee under the guidance and control of Mr Austin

Mr Austin

acted as a Shadow Trustee."

In relation to the bank accounts of the schemes of which she was trustee she asserts in paragraph 77 of her amended Defence that:

"Mr Austin was in control of the cheque books."

- Mr Barratt's pleaded position is that all payments were made "

under the direction of Mr Austin

and invariably I was not even informed

", that he did not lend his name as a trustee and director but "

fulfilled the duties requested of me by Mr Austin

" and that "

Mr Austin controlled everything even the Trustees" - see paragraphs 20F(d) and (e) and paragraph 62 of the Schedule to his amended Defence.

- In any event, the email traffic that is available demonstrates what Ms Dalton and Mr Barratt plead to be true. This is most relevantly demonstrated in the role that Mr Austin played (most of the time acting via Mr Mitchell) in supervising the opening of bank accounts by Ms Dalton and Mr Barratt in the names of the schemes of which they were trustees, by the opening of other accounts in the name of some schemes that were kept secret from the trustees and by the way in which the accounts were managed and controlled thereafter. There are a large number of internal emails that illustrate each of these points. It would lengthen this judgment unnecessarily if I was to refer to all of them. However, I set out below a selection that illustrate each of the themes that I have mentioned. The material I refer to amply supports the conclusion that Mr Austin was the driving force of the pension transfer operation the subject of this claim, that he was a "shadow trustee" as Ms Dalton describes of each of the Receiving Schemes and that each of Mr Barratt and Ms Dalton did his bidding while ostensibly being independent trustees of the various Receiving Schemes as both accept in their respective Defences.

- There is no documentation for any of the Receiving Schemes that would normally be found in relation to pension schemes such as minutes or file notes recording decision making or investment analysis. The bank accounts that were set up by Mr Barratt and Ms Dalton were opened using UK addresses that were not their own see by way of example the run of emails starting with that dated 1 August 2014 from Pitmans (the solicitors then retained to provide advice concerning the schemes) requesting the addresses of Mr Barratt and Ms Dalton. Entirely consistently with the role of Mr Austin being as I have described, that email was sent to him rather than two ostensibly independent trustees. This was chased by Pitmans by email to Mr Austin on 6 August 2014. This resulted in an internal email from Mr Austin to Mr Mitchell in which he asked for the personal postal addresses of each adding "

Sue's is her mothers. Alan is his brothers". This resulted in a reply from Mr Mitchell in which he supplied the addresses "

on the trust deeds

" but added "

this

is not the address that I collected the cheque books from in 2013

". Mr Austin responded that the addresses required were the ones from which Mr Mitchell collected the cheque books, which then produced from Mr Mitchell a different and single address. A number of points emerge from this. First it is clear that addresses were being supplied to the banks that were different from the addresses on the trust deeds. It is difficult to think of a legitimate reason for this practice. Secondly, Mr Austin was managing matters so that no direct contact was made between the solicitors providing advice about the schemes and their ostensible trustees. Thirdly it would appear that Mr Austin acting by Mr Mitchell exercised control over the cheque books (and therefore the accounts) from the moment the accounts were opened.

- Mr Austin acting by Mr Mitchell orchestrated and pushed forward the opening of the accounts see by way of example Mr Mitchell's work log entries concerning bank accounts for Callahan Consulting, Fort Bruce recruitment and Williams Bell where the forms are recorded as having been completed by 24 May 2013. The "Action" required is described as being " Email to Sue and Alan separately to request

to initiate with the banks". Independent trustees would not need to be instructed in the need for such a task. What is described is consistent with the position being as described by Ms Dalton and Mr Barratt in their respective Defences as set out earlier. Similarly consistent is the report back from Mr Barratt to Mr Mitchell of the opening of the relevant accounts see by way of example the email of 6 June 2013. It is illustrated too by the email from "Jane" to Mr Barratt and copied to Mr Mitchell dated 30 June 2013. The terms of the email show that the sender is controlling the process.

- I am satisfied on the evidence available to me that "Jane" was a pseudonym used by Mr Austin and the "[email protected]" email account was an email account used by Mr Austin. It is alleged by TPR that this was part of a scheme by which Mr Austin sought to disguise or conceal his involvement in the transfer of pension pots to the Receiving Schemes. The email is signed "Jane Lieb". This individual was Mr Austin's sister. She had no role to play within the SPI organisation. That Mr Austin used the Jane Lieb account in this way is put beyond doubt by the email exchange between Mr Austin and Ms Dalton referred to in paragraph 69 below. This conclusion is consistent with the evidence given by Mr Tyrrell (whose evidence I accept) at paragraph 44 of his statement, where he confirms that he was told by both Ms Turgut and Mr Mitchell that "Jane" was Mr Austin and that it was to disassociate him from the transfer element of the operation. It is also consistent with Mr Austin's sister's response when asked who she thought was operating the account when she said "Well, I could only imagine it might be David".

- The Fort Bruce cheque book was received not by its ostensible trustee but by Mr Mitchell. That is not something that an independent trustee acting in the best interests of the Members would have permitted. Had it happened such a trustee would have demanded that the cheque book be handed over to him. That did not happen.

- The degree to which the process was controlled by Mr Austin acting by Mr Mitchell is illustrated by an email string commencing with an email to Ms Dalton from HSBC of 21 June 2013 asking for details concerning new accounts that had been requested by her and asking for copies of the relevant trust deeds. A competent and independent trustee would have responded directly. In fact Ms Dalton forwarded the email to Mr Mitchell with a copy to "Jane". Ms Dalton's covering email said:

"Hi Ian

Just spoken with Jane re the communication below from HSBC.

She asked if I could forward this to you to liase (sic) with you on the sending of the trust document.

She has advised me that we are looking for Pension Scheme Accounts, not current or saving accounts.

Let me know how you want me to proceed."

The terms of this email are entirely consistent with the role of Ms Dalton as trustee being as she described in her Defence. It demonstrates that she had no understanding of the technicalities of being a pension scheme trustee or of her doing anything other than she was directed to by either Mr Austin or Mr Mitchell on his behalf. She was willing to refer to Mr Austin as "Jane" in internal emails even though she knew his true identity, as is apparent for example from the fact that in this email she said that she had spoken to "Jane" in a context that means it could only have been Mr Austin. Following a request for clarification from Mr Mitchell as to which scheme trust deed was required, Ms Dalton responded, tellingly in my judgment, "I think so! I will leave it to you, the expert!!!

".

- On being told by HSBC that a personal attendance was required in order to open the accounts, Ms Dalton reported to "Jane" (that is Mr Austin) by email to the Jane email account dated 27 June that this was required but that she would not be able to attend until 9 July. This caused "Jane" to email Mr Mitchell recording that Ms Dalton would travel to Rochdale for the account opening on 9 July. Mr Mitchell reported the successful opening of accounts by Ms Dalton on 11 July 2013. Mr Austin responded "Account type says community. Does that mean trust accounts? Shouldn't they have pension scheme in the account name or am I missing something?". This is the email of someone who in truth is in control of and is orchestrating the affairs of the schemes of which Ms Dalton is ostensibly the trustee. It also illustrates the degree to which Ms Dalton was a cypher.

- The true role of Mr Austin being as I have described above is also supported by his instruction to Mr Mitchell contained in an email of 23 February 2014 in the following terms:

"Ian

Can you please get ready all the paperwork to have accounts opened for the Gresham schemes with Cater Allen also.

Please keep this confidential at this stage as don't want Alan [Barratt] finding out"

This is not in any way consistent with Mr Barratt being an independent trustee or of him being thought of as such by Mr Austin or the true position being anything other than Mr Austin being in control of the operation the subject of these proceedings.

- Once cheque books had been obtained for the accounts opened in the name of the Receiving Schemes, Ms Dalton and Mr Barratt signed books of blank cheques which were then held in the FPL office and used by or in accordance with directions given by Mr Austin. Again there are a large number of emails that demonstrate the practice. It is necessary that I refer only to a few to illustrate the practice. That pre-signed cheques were provided by the trustees is shown by an email exchange between Mr Austin and Ms Turgut (FPL's accounts and office manager) on 1 November 2013. Neither were trustees of any of the Receiving Schemes. The string starts with an email from Ms Turgut asking whether she should send a cheque to Pitmans in settlement of their invoice "

re Callahan". This ought to have been a matter for the trustee (Mr Barratt). In fact Mr Austin responds "yes do cheque". The response from Ms Turgut was "No more Callahan cheques!!!!!!". Mr Austin responded to the effect that "

you will need to get Alan to do this through telephone banking. I am pretty sure you need a card and card reader to pay online". This is a significant exchange because it shows that pre-signed cheques were being used as a matter of course by Mr Austin without prior recourse to the relevant trustee and also because his ultimate response shows that Mr Barratt was expected do what he is asked to do by Ms Turgut.

- By an email of 28 May 2013, Mr Austin directed an employee who was not a trustee to "please pay a cheque for £20K from Regency Pension Scheme to Susan Dalton tomorrow. It is for trustee fees

.". This was acknowledged by the person to whom it was addressed the following morning when she said that she would be "paying in lunch time". This could only have been carried into effect using pre-signed cheques. Mr Austin was not a trustee and so should not have been authorising payments away of scheme funds. No formalised basis for the payment of trustee fees has ever been identified and the services being provided did not merit fees being paid. There is no documentary material available to me that justifies the payment of £20,000 either before or after the event. There is no invoice that supports it and no time sheet or other record that demonstrates how it has been calculated. In my judgment, Ms Dalton knew perfectly well that she had no entitlement to receive this sum on these grounds and also because she was in truth simply a cypher doing as she was told by or on behalf of Mr Austin and thus provided no value other than a means by which the liberation operation carried on by Mr Austin could proceed.

- The lack of engagement by Mr Barratt as a trustee is illustrated by an exchange of emails between him and Ms Karen Turgut concerning trustee fees. By an email of 31 July 2013, Ms Turgut asked Mr Barratt for his bank account details "

so I can pay in a cheque for Trustee Fees?". Mr Barratt's response was to given the bank, sort code and account number and add "

How much will the chq be for?". The response from Ms Turgut was "The cheque amount will be £5000.". This is an extraordinary question to ask of a trustee and extraordinary responses explicable only on the basis that the cheques had been pre-signed, were controlled by staff answerable only to Mr Austin and that the trustee (in this case Mr Barratt) was simply a cypher. This email also supports the proposition for which TPR contends namely that there was no proper basis on which trustee fees in the sums paid in fact to Mr Barratt and Ms Dalton could be justified. All the points made earlier concerning the £20,000 payment to Ms Dalton apply with equal force to this payment to Mr Barratt. That Mr Austin controlled what was paid out of the Barratt Schemes and to whom and that Mr Barratt simply went along with those decisions is also illustrated by the email of 29 October 2013 from Mr Austin to Ms Turgut.

- By an email of 13 March 2014, Mr Austin (using the Jane Lieb email account) gave instructions to Ms Dalton concerning funds held in accounts in the name of the Receiving Schemes of which she was trustee. Those instructions concerned the transfer of funds from Scheme accounts to the FPL accounts with Santander (something which no independent trustee would have been willing to consider given the credit risk implications of so doing) and concluded as follows:

"

From Dellaney Gibbons

Transfer balance of £4258 remaining to Sue Dalton Barclays trustee fees

From Williams Bell

Transfer balance of £2794 remaining in account to Sue Dalton Barclays trustee fees

Can you also ring YB to check the balances today to make sure these figures are right. Karen is not available today. "

This is significant because it supports the conclusion that there was no objectively justifiable basis for the sums being paid to Ms Dalton, that, in this case, the sum chosen depended simply on the balance remaining in a particular account and that what was paid out depended exclusively on the instructions of Mr Austin. It also shows that Ms Dalton was no more in control of the funds of which she was trustee than was Mr Barratt. Far from knowing what balances were held on which scheme accounts of the schemes of which she was trustee, it is clear that these records were maintained and accessed by Karen Turgut, FPL's then incumbent office and Account Manager.

- The absence of any entitlement on the part of Ms Dalton to the payments made to her is apparent from the email that followed completion of these transactions in her email to Mr Austin of 14 March 2014, she copied email instructions giving effect to the instructions given to her by Mr Austin using the Jane Lieb email account referred to above saying "for your information, thanks. Much appreciated". This is not the reaction of someone receiving fees to which she was entitled as of right. The email exchange is interesting also because it provides confirmation that "Jane Lieb" is in fact Mr Austin. The original instruction to make the transfer was given by Mr Austin using the Jane Lieb email account but the email from Ms Dalton confirming that the instructions had been complied with and thanking him for the payments to her was sent to Mr Austin's own account.

- It is necessary that I refer specifically to a small number of further examples showing how in practice the various Receiving Schemes and their funds were operated. On 23 July 2013, Mr Austin instructed Mr Mitchell to transfer £600,000 to FIC from Regency. He added that "The cheque for Regency and the deposit book for Friendly is in the draw." There is no evidence of Mr Austin seeking or understanding that he is required to obtain the prior agreement of Regency's trustee (Ms Dalton) for such a transfer. On 28 August 2013, Ms Turgut informed Mr Barratt by internal email that she had made three payments totalling £285,000 from the Fort Bruce, Callahan and Gresham accounts. Mr Barratt was trustee of each of these schemes. Although he asked who the beneficiaries of the payments were, he did not express any surprise that the sums should have been transferred without his authority. He was apparently entirely satisfied with the response, which was "Friendly Pensions".

- Other examples of transfers from scheme accounts to FPL on the instructions of Mr Austin include those given on 17 September 2013 to Mr Mitchell for the transfer of £120,000 from Fort Bruce to the FPL account, an instruction from Mr Austin to Ms Turgut to transfer £190,000 from the Fort Bruce account and £250,000 from the Gresham 2012 account to FPL's account and (although not in the end executed) an instruction from Ms Turgut to Mr Barratt contained in an email of 21 October 2013 to transfer £250,000 from the Daycroft account to FPL's account followed by a chaser in fairly peremptory terms. It is inconceivable that such an instruction would be given to a trustee unless the operation worked in the manner that I have described above.

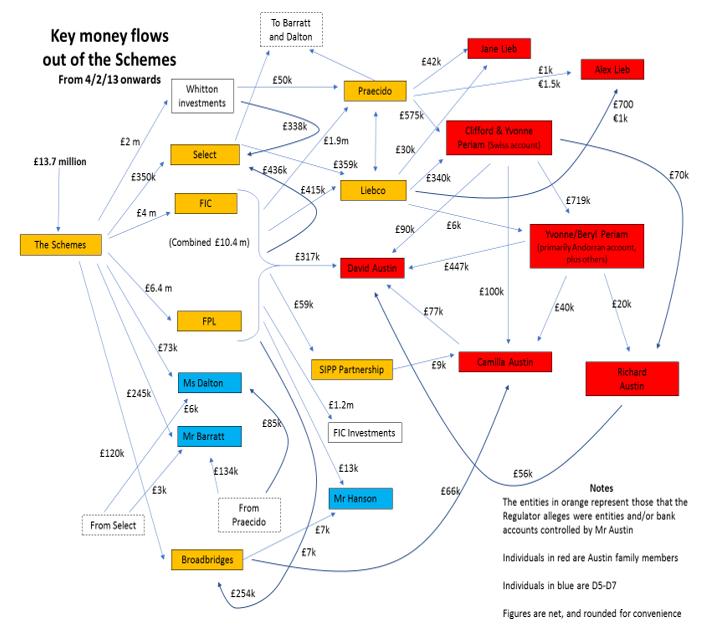

- The result of this activity was significant personal gains by Mr Austin and his family, Mr Barratt and Ms Dalton from the Receiving Schemes. It is entirely unnecessary for me to set out all the detail that surrounded the transfer of funds to Mr Austin and his family. It involves the circular transfer of funds through accounts controlled by a significant number of entities controlled by Mr Austin including FPL, FIC and the first and second defendants before ultimately ending up in the personal accounts of Mr Austin and his family. The detail is set out in the seventh witness statement of Ms Tania Edwards, whose evidence on this issue has not been challenged by any of the defendants and the documentation referred to by her. I accept that evidence. The way in which cash flowed into the hands of Mr Austin and his family are set out in the following key flow diagram:

The sums ultimately received by Mr Austin and his family from the Receiving Schemes derived from the documentary evidence totals £1,355,946.30 and 2,472.92. The same material proves that Mr Barratt received sums totalling £382,208.16 and Ms Dalton £168,205.69. This diagram also reflects the monies that flowed through the FPRF Scheme to Mr Austin on the instructions of Mr Hanson, which I explain in detail below.

- Not all the sums received by the Receiving Schemes were paid as cash in the manner I have described. Much of it was invested but invested in a manner that was entirely inappropriate for pension funds and without any or any real involvement of the people ostensibly primarily responsible for such activity the trustees. Given that TPR's case on this issue has not been challenged by any of the defendants it is not necessary that I set out the detail of its case on this issue. It is necessary to remember only what Ms Dalton and Mr Barratt plead in their defences concerning the degree of control exercised over their activities as trustee by Mr Austin. It is not suggested by either of them and there is no documentary evidence of any consideration by either as to the investment of the money received by the Receiving schemes of which they were respectively trustees. The documentary evidence that is available demonstrates very clearly that it was Mr Austin who controlled all investment activity.

- The investments made included the investment in the Freedom Bay development project and a product called the "Affinity Bond". These are referred to in the diagram at paragraph 75 as the "Whitton Investments". The first concerned a property development in St Lucia. According to the statement of Mr Copeland, a director of the eighth defendant, this investment entitled the investor to what is described as "fractional ownership" in villas on the development. As Mr Copeland puts it, it was "

effectively a time share

". The development started but any benefit from the investment depended on the development being completed. It has not been and the developer has been placed in receivership. The prospect of there being any recovery of the sums invested is described by Mr Copeland as being "

severely limited". The investment was a high risk investment which was not in the event secured. Although funds were supposed to be held in escrow pending construction of the properties, that did not happen see paragraph 81 of Mr Copeland's witness statement. There is no evidence of any due diligence having been carried out in relation to it. Had it been, it would have been apparent that the investment was highly illiquid (thus preventing trustees moving with ease to other investments as the interests of the Members required and the business climate dictated), and that the insolvency risk was high unless the escrow arrangement worked as it was presented something that does not appear to have been considered or investigated by either Ms Dalton or Mr Barratt. No trustee acting reasonably would have invested significant sums in this project. High levels of commission were payable for these investments.

- The Affinity Bond was another high-risk investment issued by Affinity Property Corporation Plc. Although it offered a headline return of 6% per annum, only 2% was payable annually with the rest being payable on maturity 10 years after issue. It is unsecured, non-transferable and without early redemption rights. This last factor has resulted in Affinity refusing to accept that the bonds are currently realisable. It resulted in the payment of higher than average commissions to introducers. It is entirely unclear whether the bonds will be redeemed on maturity. There was thus a very significant insolvency risk that is necessarily irremediable. This description alone ought to have alerted anyone acting reasonably in the best interests of Members that this was not an investment that ought to have been contemplated by the Scheme trustees. In fact, Mr Austin, Ms Dalton and Mr Barratt were aware that this was so. The context of the next email that I refer to is that at a time when Ceding Schemes were increasingly reluctant to transfer pots to the Receiving Schemes, Mr Austin sought to avoid this difficulty by persuading Members to transfer to SIPPs rather than occupational pension schemes such as the Receiving Schemes. That required a SIPP provider to administer the SIPPs concerned. On 29 July 2013, Mr Austin emailed a number of individuals including Ms Dalton and Mr Barratt (in their capacity as sales agents procuring the transfer of pots at this stage from Ceding Schemes to SIPPs) concerning the Affinity Bond investment in these terms:

"Unfortunately Brooklands have decided to only allow H[igh] N[et] W[orth] or sophisticated investors to purchase the Affinity Bond. This effectively disallows all our investors move ahead down the SIPP route with them.

As a result we need to seek a new Sipp provider that has approved Affinity and will allow the client to invest 100% of the fund within one unregulated product.

"

- Any trustee acting reasonably in the interest of a Member would not contemplate investing in any investment 100%, particularly when what is being invested in is unsecured, depends for its apparently attractive yield on redemption 10 years after the initial investment and is non-transferable. Even people as apparently inexperienced and lacking in understanding concerning investment as Mr Barratt and Ms Dalton ought to have appreciated that the investment was not suitable in light of the position adopted by Brooklands. The email from Mr Austin shows first his intention that investment in the Affinity Bond should continue notwithstanding the position adopted by Brooklands and secondly that it was he who was taking the investment decisions rather than the trustees to whom his email was addressed.

- The other area of investment was into first FIC and then FPL - companies controlled by Mr Austin. This was obviously something that independent trustees acting reasonably in the best interest of Members would undertake only after the most careful due diligence enquiries and probably only with the benefit of extensive external advice. In fact Mr Austin controlled the schemes because he controlled Mr Barratt and Ms Dalton and thus he controlled investment and exercised that control by investing in FIC and FPL. Aside from the obvious failure of the trustees to exercise any control or influence over this practice, Mr Austin deliberately misrepresented his role in order to ensure that the process could continue see by way of example his response to a Barclays Bank official concerning the manner in which such investments were generated. He described the schemes that included the Receiving Schemes as independent by stating that

"

I was introduced to the trustees of these occupational pension schemes because they offer a low cost, efficient and regulated wrapper with a wide remit of acceptable HMRC approved investments. "

Having explained that the mechanism for investment depended on clients being persuaded to transfer their pension pots to those funds, he then continued:

"Up until the schemes investment in the Friendly Bond, I have not had any business dealings with the schemes but I was made aware of the pension schemes and the trustees running the schemes through an involvement in a business called Sipp Partnership Limited of which I am the sole shareholder and director.

Neither the directors of the sponsoring employer nor the trustees of the schemes

. Share any directorships with any of the companies that I am involved with. The trustees

do not own any shares in any of my companies

"

Given what is set out above, it is plain that this is a thoroughly dishonest and misleading description of what in fact was happening in the operation that I have concluded was controlled from beginning to end by Mr Austin who also controlled the actions of the trustees including Mr Barratt and Ms Dalton. There can be no doubt that Mr Austin knew that this description of how the operation worked was deceptive given what I have said already. Equally deceptive was Mr Austin's description of the investments into FIC contained in a witness statement signed by him in an attempt to persuade Barclays bank to unfreeze FIC's bank account. Having described FIC as being in business "

to invest in companies active in the development of infrastructure and technologies in the renewable energy sector and to invest in environmentally and/or socially responsible commercial activities in the UK and Europe

" carried on by the issue of "

unlisted retail bonds

" he then stated that purchasers of the bond included the Receiving Schemes and that the largest investors were Regency and Gresham. In fact the only purchasers were the Receiving Funds. He then asserted (and this is not in dispute) that the schemes were entitled to invest in unregulated investments which included the bonds before adding at paragraph 14 that "

The Pension Schemes are administered by independent trustees who are not connected to me

" and at paragraph 17 that:

"The individual retail customers are being independently advised by independent introducers with no connection to [FIC] or the Pension Scheme trustees to join the Pension Schemes

"