This judgment was handed down remotely at 10am on 27 October 2023 by circulation to the parties or their representatives by e-mail and by release to the National Archives (see eg [2022] EWCA Civ 1169).

The Hon Mr Justice Butcher :

- The Claimants have applied for notification injunctions against the Ninth Defendant ('Halimeda'), the Seventeenth Defendant ('ROSATOM'), the Nineteenth Defendant ('FESCO') and the Twentieth Defendant ('Transneft'), and for worldwide freezing orders against the Eleventh Defendant ('Mr Rabinovich'), the Twelfth Defendant ('Ermenossa'), the Thirteenth Defendant ('Mr Kuzovkov'), the Fifteenth Defendant ('Mr Severilov'), the Twenty-First Defendant ('Mr Garber') and the Twenty-Second Defendant ('GHP').

- The notification injunction sought would require the relevant Defendants: (A) to give the Claimants' solicitors notice of an intention to (1) acquire or dispose of shareholdings worth US$ 1 million or more; (2) make any reorganisation or alteration of its capital structure; (3) take on or pre-pay debt facilities in excess of US$ 50 million; (4) commence, settle or discontinue litigation with a value in excess of US$ 10 million; or (5) to declare or pay dividends or otherwise distribute assets to shareholders or investors; and (B) to inform the Claimants' solicitors of all their assets worldwide exceeding US$ 1 million in value.

- The Claimants' claims relate to two alleged conspiracies. One is what has been called the 'NCSP Conspiracy', which concerns an interest which the First Claimant ('ZM') had in PJSC Novorossiysk Commercial Sea Port (or 'NCSP'). That conspiracy is said to have involved the Tenth Defendant ('Ms Mammad Zade') and the Twentieth Defendant ('Transneft'). The other, which is said to have involved Ms Mammad Zade and all the other Defendants except Transneft, is what has been called the 'FESCO Conspiracy', which relates to ZM's stake in FESCO. Insofar as the application related to the NCSP Conspiracy, and thus as far as Transneft was concerned, it was adjourned on the first day of the hearing. The remainder of the hearing concerned only the alleged FESCO Conspiracy.

- The alleged FESCO Conspiracy is said by the Claimants to have been 'intricate', 'coordinated', 'stealthy' and accompanied by 'subterfuge'. It is alleged to have had at least three limbs, which may be said to be (1) the Option Agreement limb, involving breaches of one or two Option Agreements; (2) the ROFO limb, involving breach of a Right of First Offer, and (3) the FESCO governance limb, in which it is said that the Claimants were excluded from the governance of FESCO.

The Basic Facts

- Because of the complex nature of the facts it is necessary, at the outset, to set out the main persons and entities involved, and their relationship, and the basic facts as to what happened. In this section of the judgment I am intending a neutral account.

ZM and FESCO

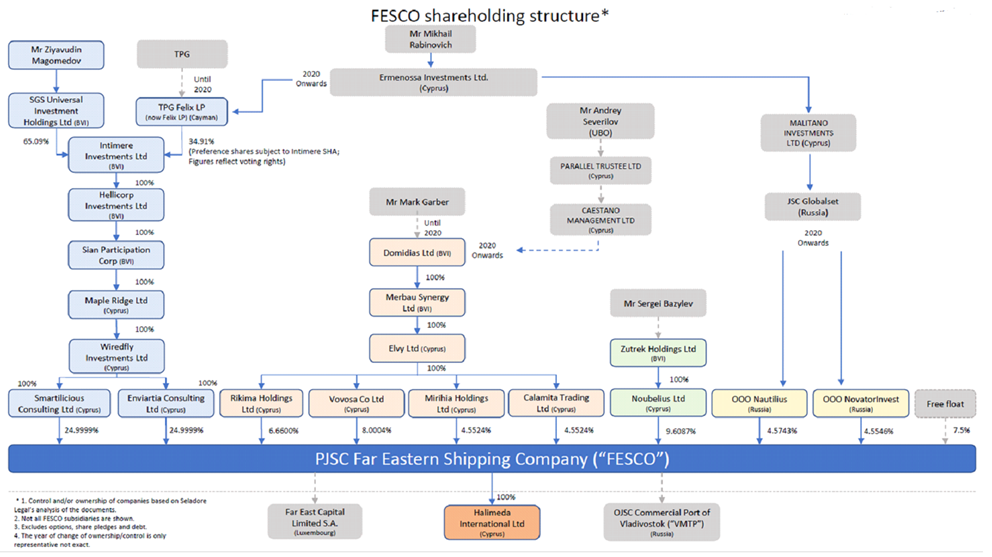

- ZM is a Russian businessman. He is the ultimate beneficial owner of the other Claimants. He has, or had, significant assets in the commercial shipping and logistics sector. One of his assets was a stake in FESCO. FESCO was founded in 1996 as the parent company of the FESCO Group. It is one of Russia's largest entities in the transportation and logistics sector, with a portfolio including port, railway and comprehensive logistics capabilities. The FESCO Group controls the Commercial Port of Vladivostok. FESCO is the 100% shareholder of Halimeda, a company incorporated in Cyprus.

- ZM acquired his stake in FESCO in or about 2012 through a complicated holding structure. The relevant relationships have been diagrammatically presented thus:

The companies in the left-hand column have been referred to as 'the SGS Branch' or the 'SGS Companies'.

- ZM acquired his stake through a leveraged buyout funded from several sources, including (i) approximately US$ 940 million in debt finance from international banks, (ii) US$ 260 million in equity finance from the US-based private equity firm, TPG, and (iii) a cash contribution from ZM himself.

Intimere and the ROFO

- TPG's investment was structured through a joint venture, which was between SGS and a TPG nominee, namely Felix LP (then called TPG-Felix LP) ('Felix'). The joint venture vehicle was the Third Claimant ('Intimere'). Felix held preference shares in Intimere. The relationship between the joint venture participants was governed by a shareholders' agreement dated 21 December 2012 ('the Intimere Shareholders' Agreement'), which was subsequently amended on a number of occasions. Pursuant to the Intimere Shareholders' Agreement, TPG was entitled to appoint one third of Intimere's directors, and a minimum of one of the nine members of FESCO's Board of Directors, while SGS could nominate five. The Intimere Shareholders' Agreement also contained provisions dealing with the possibility of sale; and in particular, in clause 9.03(a), there was a 'Right of First Offer' (or 'ROFO') when any sale of Intimere shares or change of control of Felix was contemplated, whereby the shareholder contemplating the sale or change of control was obliged first to offer its shares to the other shareholder.

- As part of the financing for the transaction, Halimeda raised funds totalling US$ 140 million (called 'the Margin Loans') from a separate group of external banks. The proceeds of the Margin Loans were then advanced by Halimeda to the Fifth Claimant ('Sian') under a Loan Agreement dated 7 December 2012 that allowed for borrowing up to US$ 150 million, and Sian loaned the funds onward to the Sixth Claimant ('Maple Ridge') for the purposes of the acquisition.

ZM's stake and other Options

- After this transaction, the Second to Ninth Claimants owned 49.99% of FESCO. It is also relevant to refer to options which the SGS Branch companies held over the recently-acquired interests in FESCO of two other groups, namely:

(1) The interest of the Eighth Defendant ('Domidias'). Domidias had acquired 23.77% of FESCO through a series of subsidiaries. Sian had an option to acquire this entire stake in FESCO. At the time, Domidias was ultimately beneficially owned by Mr Garber.

(2) The interest of Zutrek Holdings Ltd. Zutrek Holdings Ltd had acquired approximately 4.8% of FESCO via its subsidiaries, as well as an option to acquire a further 4.8% from East Capital AB. Zutrek Holdings Ltd was and continues to be ultimately beneficially owned by Mr Sergei Bazylev.

Maple Ridge Loan

- In the period following the acquisition, the bank lending was refinanced by US$ 875 million in Loan Notes issued by a subsidiary of FESCO, Far East Capital Limited SA ('FEC'). Approximately US$ 796 million was lent on to Maple Ridge, to enable it to repay the prior acquisition finance ('the Maple Ridge Loan'). On 13 December 2018, the benefit of the Maple Ridge Loan was assigned to Halimeda.

TPG's desire to exit Intimere

- TPG had indicated to ZM from at least September 2017 that it wished to sell its interest in the SGS Branch.

Legal proceedings against ZM in Russia

- The Claimants say that 'from around early 2018 it seems that ZM fell out of favour with the political/business leadership in Russia and retaliatory steps then began to seize assets of strategic interest to the Russian state.' On 30 March 2018, ZM and his brother, Magomed Magomedov ('MM'), were arrested on charges brought by the Russian Ministry of Internal Affairs and the Federal Security Service ('FSB') of 'organised crime' and 'embezzlement' (POC para. 2). The brothers have always denied these charges, and the Claimants' evidence is that ZM believes them to have been politically motivated.

- As a result of these criminal proceedings, ZM's funds were the subject of an interim arrest by order of the Tverskoy District Court in Moscow on 5 April 2018, pending the completion of the criminal investigation, and on 28 April 2018 there was a further interim arrest of shares in ZM's Summa Group and 13 companies controlled by it, including FESCO, by order of the Preobrazhensky District Court of Moscow (POC, paras. 217-8). It is the Claimants' case that these arrests were of assets greatly exceeding the amounts involved in the crimes of which ZM was accused.

- The Magomedov brothers remained under arrest. On 24 September 2019 the Basmanny District Court of Moscow granted an extension of the term of the arrest over shares of various legal entities, including FESCO. FESCO appealed that order, but the appeal was unsuccessful. On 29 August 2022 the Meshchansky District Court of Moscow ordered an extension of the arrests in the criminal proceedings until 5 December 2022. (POC para. 222) On 19 October 2022 the Russian General Prosecutor applied for the confiscation of all assets which had previously been arrested in the criminal proceedings.

- ZM and MM were convicted in the criminal proceedings against them on 24 November 2022. They were sentenced to terms of imprisonment of 19 years and 18 years respectively. The sentences passed '[also] included confiscation orders against all of their assets. The confiscation includes the shares held by the Domidias and Zutrek branches, as well as those of SGS (Smartilicious [viz the Eighth Claimant] and Enviartia [viz the Ninth Claimant])'. (POC para. 224)

- '[D]espite having already requested confiscation of the FESCO shares in the criminal proceedings against [ZM], in or about late November 2022, the General Prosecutor's office commenced parallel civil proceedings in the Khamovnichesky District Court of Moscow against, among others, [ZM], [MM], Mr Bazylev, Mr Rabinovich and Mr Severilov, seeking the confiscation of all shares in FESCO. The corporate entities through which these individuals hold FESCO shares (including Smartilicious and Enviartia) are also named as defendants to these civil proceedings.' (POC para. 226)

- In circumstances which the Claimants allege to have been profoundly unfair, procedurally, on 11 January 2023, the judge in the Khamovnichesky District Court of Moscow granted the General Prosecutor's application in full and made a (further) order for the confiscation of the FESCO shares. (POC para. 227)

- ZM and other defendants appealed against this ruling, but on 15 May 2023 the City of Moscow Court refused the appeal and upheld the judgment of the Khamovnichesky District Court. A further appeal has been filed. (POC para. 228)

The Fate of the Options

- I have already set out that, as part of the arrangements under which ZM had acquired a stake in FESCO, Sian had acquired an option over Domidias's stake in FESCO. This has been referred to as 'the 2012 Option'.

- It is the Claimants' case that in 2018 and 2019 ZM instructed Ms Mammad Zade to exercise the 2012 Option, but that she failed to do so. It is the Claimants' case that this option expired on 28 November 2020. It is Domidias's case that it expired in 2019, and there are at least some contemporary emails which indicate that the parties thought that the 2012 Option would expire in late 2019. In late 2019, there was negotiation of a new option, which would be in favour of the Fourth Claimant ('Hellicorp'), a subsidiary of Intimere, to acquire Domidias's interest in FESCO. This has been called the '2019 Option'. The Claimants contend that this was 'a highly unusual agreement', in respects to which it will be necessary to return.

- Mr Garber had sold Domidias to an entity beneficially owned by Mr Severilov, on 28 September 2020. Notice to exercise the 2012 or 2019 Options was given by Sian and Hellicorp on 4 November 2020. Domidias has not complied with those notices, and has contended that (a) the 2012 Option had expired, and (b) the 2019 Option was never finally agreed.

- Sian and Hellicorp have brought proceedings in the Commercial Court (CL-2021-000165), which were commenced on 19 March 2021, and which have been referred to as 'the Commercial Court Option Proceedings'. The primary claim is for specific performance of the 2012 Option in favour of Sian and alternatively for specific performance of the 2019 Option in favour of Hellicorp. The defendants to that action, Domidias and its subsidiary Merbau Synergy Ltd ('Merbau'), have issued an application for summary judgment, which is scheduled for hearing from 13 to 15 February 2024. The pleadings in that action were before the court on the present application.

The Fate of the ROFO

- As already set out, under the Intimere Shareholders' Agreement, SGS had a ROFO if TPG was looking to sell its interest in the joint venture.

- On or about 14 July 2020, TPG and Mr Rabinovich's company Ermenossa reached an agreement in respect of the sale of the Felix shares.

- On 15 July 2020, Felix sent SGS a ROFO offer, indicating that a change of control over Felix had been proposed to occur; and offering to sell to SGS all Felix's Preference Shares for an aggregate purchase price of US$ 35 million. The Claimants contend that the ROFO Offer was accepted by SGS on 14 August 2020, and that the parties (through their legal representatives, Cleary Gottlieb on behalf of Felix and DLA Rus on behalf of SGS) thereafter negotiated and reached a concluded agreement on all required aspects of the deal by 7 October 2020.

- In the meantime, on 18 August 2020, Ermenossa wrote a letter to the Russian Federal Anti-Monopoly Service ('FAS'), which said that SGS's acquisition of the shares in Intimere would result in SGS obtaining more than a 50% stake in FESCO, and that this would require FAS approval. It concluded:

'WE ASK YOU:

To issue a written warning to the officials of [SGS] and [Felix] about the inadmissibility of the acquisition of shares/participatory interests in [Intimere] owned by [Felix] by way of accepting the ROF Offer without obtaining the prior consent from the [FAS].'

- The FAS wrote to Felix and SGS on 13 and 19 October 2020 saying that the transaction should be suspended until an FAS decision was made. TPG and Felix then contended that the sale to SGS could not complete and, on 18 November 2020, Ermenossa completed the acquisition of Felix.

- SGS brought an LCIA Arbitration ('the LCIA Option Arbitration') against Felix under the Intimere Shareholders' Agreement on 14 October 2020. The tribunal, which consisted of Helen Davies KC, Christopher Style KC and Michael Brindle KC, determined, by a Partial Final Award dated 26 April 2022, that Felix had been in breach of the Intimere Shareholders' Agreement. The tribunal concluded:

(1) That approval of the ROFO transaction had not been required pursuant to Russian competition law or the Law on Strategic Companies;

(2) That there would have been no breach of Russian law if SGS had proceeded with the ROFO transaction notwithstanding the FAS letter;

(3) That Felix held its shares in Intimere on trust for SGS; and

(4) That SGS was entitled to an order for specific performance of the ROFO.

- SGS decided not to pay the US$ 35 million ROFO price, and to seek damages in lieu. This is said to have been done because of the confiscation of the FESCO shares by the Russian State. SGS has been granted an order discharging the order for specific performance. The application for damages is pending.

The Sian and Maple Ridge Loans and the Governance of FESCO

- As set out above, in consequence of the initial acquisition, Sian and Maple Ridge had been lent substantial sums. Halimeda was (either originally or by assignment) the creditor.

- On 12 February 2020, a letter was sent by Halimeda to Maple Ridge and Sian demanding repayment of the loans and suggesting that the debtors make a proposal for a repayment plan. The Claimants say, however, that when and how this letter was received by those companies is unclear.

- During the course of 2020, KPMG, who were FESCO's auditors, undertook a project (called 'Project Moonlight') looking at the tax efficiency of the group structure. It was presented to FESCO's Strategy, Investment and General Affairs Committee in March 2020. It set out various proposals to address tax inefficiencies. On 14 April 2020, the Strategy Committee resolved that the FESCO Board should be recommended to approve the Project Moonlight plan. The Strategy Committee also procured a legal opinion from Cleary Gottlieb, dated 14 May 2020, which addressed whether the directors of FESCO would be in breach of duty if they agreed, as part of the restructuring, to an extension of time for the repayment of the loans.

- The Claimants contend that Ms Mammad Zade then took steps to postpone or avoid a FESCO Board meeting which would consider Project Moonlight. What undoubtedly happened was that there was a meeting of the FESCO Board on 3 September 2020. The Board approved the commencement of legal proceedings by Halimeda against Maple Ridge and Sian in respect of the loans. The Claimants contend that that decision was explicable only on the basis that a member or members of the Board had been improperly induced or coerced into voting for it.

- On 16 September 2020, a request was submitted in the name of Halimeda to commence an LCIA arbitration to enforce the Maple Ridge loans ('the Maple Ridge LCIA Arbitration').

- On 28 September 2020, Halimeda obtained ex parte injunctions from the Limassol District Court in Cyprus against Maple Ridge, Smartilicious and Enviartia. The application was said to be in support of the recently commenced Maple Ridge LCIA Arbitration. The injunctions, inter alia, prevented Smartilicious and Enviartia from exercising their voting rights at the forthcoming FESCO AGSM, which in the event was held on 16 November 2020, and at which Mr Severilov was appointed Chair of the Board. These injunctions became final on 5 October 2020, when the respondents failed (in disputed circumstances) to attend the return date.

- On 30 September 2020 an application for Sian's compulsory winding up was issued in the name of Halimeda in the High Court of the BVI, on the basis of Sian's debt to Halimeda ('the Sian Liquidation proceedings').

- The Cyprus injunctions were set aside by the Cyprus District Court on 16 November 2020, on the basis, in summary, that they had 'disproportional consequences on the applicants [viz Maple Ridge and its subsidiaries] in comparison with what the respondent [Halimeda] intended to succeed for its benefit, whose beliefs that the directors will act in a certain way are mere suspicions.' There is an appeal pending against this decision.

- On 27 November 2020, Mr Shagav Gadzhiev (who is ZM's nephew, has been representing his interests, is a director of the Second to Fourth and Tenth Claimants and has been the main source of instructions for the Claimants' solicitors on this application) filed an Affidavit in the Sian Liquidation proceedings. This deposed to his belief that 'over the course of 2020 [ZM] and the companies in the SGS Investment Branch including Sian have fallen victim to a campaign of interference with their contractual relations and with other shareholders.

Sian believes, and respectfully suggests that it is to be inferred, that this campaign has been carried out pursuant to an unlawful means conspiracy involving at least Halimeda, FESCO and the Domidias Investment Branch and those persons controlling and instructing the same (the 'Hostile Parties').'

- On 5 January 2021, Maple Ridge served its Defence in the Maple Ridge LCIA Arbitration. This alleged 'a conspiratorial effort undertaken by [Halimeda], its parent company [FESCO], and other corporate entities and individuals, [of which] the ultimate purpose

is to strip [ZM] of his FESCO shareholdings'; and also referred to the legal process against him in Russia, and said '[it] is certainly not the first time in recent history that a wealthy Russian business person has been incarcerated whilst strategic assets are 'returned' to Russian state control.'

- On 28 January 2021 the Second to Ninth Claimants commenced an action in the BVI against Halimeda, Domidias, Merbau, Ms Mammad Zade and Mr Rabinovich ('the BVI UMC proceedings'). This put forward a case of a conspiracy involving at least the named defendants to that action, FESCO, Felix, 'and unknown others', which had and has as its ultimate objective the wresting of the FESCO Group shareholding from the SGS Investment Branch, and therefore from [ZM], 'for less than its fair value and for the sole benefit of the Hostile Parties and/or those that control them.' The Statement of Case in that action (both originally and more so as amended) is in many respects similar to the Particulars of Claim in the present proceedings.

- On 19 May 2021, Wallbank J in the BVI High Court (Commercial Division) granted Halimeda's application and appointed liquidators over Sian in the Sian Liquidation proceedings. Sian had resisted that application on a number of grounds, including that the conspiracy which it alleged gave rise to a set off. Wallbank J said that a number of the points 'evaporated as the desperate tabulae in naufragio that they were.' He said that the Sian debt 'is indeed currently due and payable'. In relation to whether the conspiracy allegations gave rise to a 'genuine cross-claim of substance or a sum equal to or exceeding the amount of the debt', Wallbank J held that they did not. He found that: (1) any loss which the SGS companies had suffered had been caused by FESCO's refusal to implement Project Moonlight, but that Halimeda's only alleged actions post-dated that, giving rise to a causation issue; (2) there was a lack of evidence of Halimeda's role in the conspiracy; and (3) there was no sufficient evidence that Project Moonlight concerned the Sian debt.

- As to (2), Wallbank J said this:

'It is not good enough simply to impute the knowledge and intentions of others onto Halimeda, as a separate legal person, at all stages. Sian says that the nature of conspiracies is such that the conspirators do not leave evidence lying around. It is inherently difficult to prove them, as one is forced heavily to rely upon inference. That is right, but the Court must decide a case upon evidence. It can draw inferences, but based upon evidence. A conspiracy theory such as is being advanced by Sian, though it has that superficially attractive feature of explaining everything, requires a lot of parts and players all to fall into their right places, at their proper times and to function seamlessly with no more plausible or probable bona fide or innocent explanation. The mere possible existence of such a conspiracy does not suffice for raising a sufficient cross-claim against Halimeda. Sian would have to go further. Causation is necessary.'

- Wallbank J also considered another argument of Sian, namely that the liquidation application was an abuse of process. In that context he said:

'I am prepared to accept for present purposes that there is some truth to Sian's conspiracy theory.

I say that because of the following two factors:

1. The alleged conspiracy theory here follows a pattern that the Court has seen in other cases played out in Russia and other countries of the CIS;

2. It is all too convenient for these liquidation proceedings to be targeting precisely the linchpin company, control over which would determine whether Halimeda's ultimate principal or his apparent business rival will have control over the corporate group as a whole.

These are big picture points. But there is a tension between big picture points and looking at detail. For my part, dwelling for a moment on the big picture, I can see the force in Sian's argument that Halimeda's winding up application has been brought for a collateral purpose as part of a hostile take-over strategy, and thus that Halimeda is abusing the process of the Court. But it is not the law that the Court should decide the matter by simply looking at what appears to be the big picture.'

Having looked at the matter in that light, Wallbank J continued:

'A purpose on the part of business rivals to wrest control of a group thus, of itself, does not turn the application into an abuse of process. The question is whether there are exceptional circumstances. Here, there are not in my respectful judgment:

One, because there is no prima facie case that Halimeda caused Sian any loss through an unlawful means conspiracy, as so far alleged by Sian.

And, secondly, it is inherent in the nature of commerce that where a company does not or cannot pay its debts when they fall due, that the company is at risk of being wound up. That is a commercial risk a businessman runs when he uses, or is content to use, a given corporate structure.'

- On 22 June 2022, Halimeda issued a jurisdiction challenge to the BVI UMC proceedings brought by the Second to Ninth Claimants.

- On 11 November 2022, the East Caribbean Court of Appeal dismissed Sian's appeal against Wallbank J's decision on the appointment of liquidators. In relation to the issue of abuse of process, Henry JA said, at [72]-[73]:

'The learned judge rejected the argument of abuse of process for two reasons. The first is based on the finding that there is no prima facie case of a UMC. That finding logically erodes the foundation for an abuse of process determination. In the second, the judge found that the winding up petition was an incident of doing business, implying that he was satisfied that the real purpose of the application was to recover the debt. Those findings were open to him on the circumstances of this case. The judge applied the applicable law and having assessed the evidence, arrived at those conclusions, which in my estimation were reasonable and justifiable on the evidence before him.'

- In the Maple Ridge LCIA Arbitration, the tribunal (Sir Jeremy Cooke, Nicholas Craig KC and Andrew Foyle) issued an award on Preliminary Issues, on 6 February 2023. This was decided on assumed facts, particularly as to the conspiracy alleged by Maple Ridge. The tribunal decided all the issues in favour of Halimeda, save one (and an additional argument concerning abuse of process). On that one the tribunal decided, on the basis of the assumed facts, that Maple Ridge's pleaded claim for loss was capable in law of providing a set-off against a claim on the loans. This left over, therefore, the question of whether the assumed facts as to the conspiracy were correct, and whether the actual facts did give rise to a set-off. As I understand it, a hearing in the arbitration to determine these matters is fixed for three weeks in October to November 2024.

- On 19 May 2023 Mr Gadzhiev filed evidence in the BVI UMC proceedings brought by the Second to Ninth Claimants. The hearing of the defendants' jurisdiction challenge in that action was fixed for 10 July 2023. On 4 July 2023, the solicitors for the claimants in that action wrote to the solicitors for the defendants to say that their clients intended to discontinue the BVI UMC proceedings and to commence proceedings in England in their place. The current proceedings were then commenced on 20 July 2023. On 24 July 2023 the Second to Ninth Claimants formally discontinued the BVI UMC proceedings.

The commencement of the present proceedings and application

- On 31 August 2023 the Claimants applied ex parte for permission to serve the Claim Form on those Defendants who could not be served here, and for orders permitting alternative service, and also for the urgent hearing of the present application.

- Mr Justice Bright conducted an ex parte hearing to seek answers to certain questions he had in relation to the applications for service out, on 1 September 2023. On 4 September 2023 he granted permission to serve out and orders for alternative service, and listed a hearing for consideration of this application on 8 September 2023. On the same date the Claimants issued the present application.

- On 5 September 2023 the Claimants applied ex parte to change the listing from 8 September to 11 September. Bright J declined that application, and indicated that the hearing could take place either on 8 or 15 September 2023. The Claimants opted for the latter. At the hearing on 15 September, which was before HHJ Pelling KC, the judge indicated that he did not consider that the matter could be heard in one day. The respondent Defendants sought the adjournment of the application, and the judge directed that it be heard on 10-12 October 2023. The matter was then adjourned, without the respondent Defendants having given any undertakings. HHJ Pelling KC ordered that the Claimants pay the respondent Defendants their costs thrown away.

Legal Principles

- The legal principles relevant to an application such as the present are well-known and were not the subject of much debate before me. They can be summarised as follows.

- There are in all such cases at least three matters to be considered, namely:

(1) Whether the claimant has a good arguable case on the merits against the defendant;

(2) Whether there is a real risk that judgment will go unsatisfied by reason of the unjustified disposal by the defendant of his assets, unless he is restrained by court order from disposing of them;

(3) Whether it is just and appropriate as a matter of discretion to grant the injunction.

- As to the first, a 'good arguable case' was described by Mustill J in Ninemia Maritime Corp v Trave Schiffahrtsgesellschaft GmbH (The 'Niedersachsen') [1983] 2 Lloyd's Rep 600, at 605, as '

one which is more than barely capable of serious argument, but not necessarily one which the judge considers would have a better than 50 per cent chance of success.'

- When applying this test, the court should not attempt to try the issues but take into account the apparent strength or weakness of the respective cases to decide whether the claimant's case, on the merits, is sufficiently strong to reach that threshold. That includes assessing the apparent plausibility of statements in the affidavits. (Alternative Investment Solutions (General) Ltd v Valle De Uco Resort & Spa SA [2013] EWHC 333 (QB) at [7]). The central concept at the heart of the test is whether there is a 'plausible evidential basis' (Lakatamia Shipping Co Ltd v Morimoto [2019] EWCA Civ 2203, at [38]).

- As to the second, the following summary was provided by Haddon-Cave LJ in Lakatamia v Morimoto at [34]:

[34] I also gratefully adopt (as the Judge did) the useful summary of some of the key principles applicable to the question of risk of dissipation by Mr Justice Popplewell (as he then was) in Fundo Soberano de Angola v dos Santos [2018] EWHC 2199 (Comm) (subject to one correction which I note below):

(1) The claimant must show a real risk, judged objectively, that a future judgment would not be met because of an unjustified dissipation of assets. In this context dissipation means putting the assets out of reach of a judgment whether by concealment or transfer.

(2) The risk of dissipation must be established by solid evidence; mere inference or generalised assertion is not sufficient.

(3) The risk of dissipation must be established separately against each respondent.

(4) It is not enough to establish a sufficient risk of dissipation merely to establish a good arguable case that the defendant has been guilty of dishonesty; it is necessary to scrutinise the evidence to see whether the dishonesty in question points to the conclusion that assets [may be][*] dissipated. It is also necessary to take account of whether there appear at the interlocutory stage to be properly arguable answers to the allegations of dishonesty.

(5) The respondent's former use of offshore structures is relevant but does not itself equate to a risk of dissipation. Businesses and individuals often use offshore structures as part of the normal and legitimate way in which they deal with their assets. Such legitimate reasons may properly include tax planning, privacy and the use of limited liability structures.

(6) What must be threatened is unjustified dissipation. The purpose of a WFO is not to provide the claimant with security; it is to restrain a defendant from evading justice by disposing of, or concealing, assets otherwise than in the normal course of business in a way which will have the effect of making it judgment proof. A WFO is not intended to stop a corporate defendant from dealing with its assets in the normal course of its business. Similarly, it is not intended to constrain an individual defendant from conducting his personal affairs in the way he has always conducted them, providing of course that such conduct is legitimate. If the defendant is not threatening to change the existing way of handling their assets, it will not be sufficient to show that such continued conduct would prejudice the claimant's ability to enforce a judgment. That would be contrary to the purpose of the WFO jurisdiction because it would require defendants to change their legitimate behaviour in order to provide preferential security for the claim which the claimant would not otherwise enjoy.

(7) Each case is fact specific and relevant factors must be looked at cumulatively.

([*] Note: I have replaced the words "are likely to be" in sub-paragraph (4) with "may be").

- In ArcelorMittal USA LLC v Ruia [2020] EWHC 740 (Comm), at [219] Henshaw J set out a number of other statements of principle which are relevant to the issue of whether a risk of dissipation has been shown, as follows:

i) The claimant should depose to objective facts from which it may be inferred that the defendant is likely to move assets or dissipate them; unsupported statements or expressions of fear have little weight (O'Regan v Iambic Productions (1989) 139 N.L.J. 1378 (per Sir Peter Pain)).

ii) Where dishonesty is alleged, it is sometimes possible to infer a risk of dissipation from the fact of the dishonesty (Norwich Union v Eden (25 January 1996, unreported, Hirst and Phillips LJJ), cited in VTB Capital plc v Nutritek International Corp [2012] EWCA Civ 808 at § 177; Metropolitan Housing Trust v Taylor [2015] EWHC 2897 (Ch) § 18 per Warren J).

iii) However, it is appropriate in each case for the court to "scrutinise with care whether what is alleged to have been the dishonesty of the person against whom the Order is sought in itself really justifies the inference that that person has assets which he is likely to dissipate unless restricted" (Thane Investments Ltd v Tomlinson (No.1) [2003] EWCA Civ 1272 § 28; VTB v Nutritek International § 177 citing Jarvis Field Press v Chelton [2003] EWHC 2674 (Ch)).

iv) For example, in VTB the Court of Appeal concluded at § 178 that it would have been right to take into account a finding of a good arguable case that a defendant had been engaged in a major fraud, and that he operated a complex web of companies in a number of jurisdictions which enabled him to commit the fraud and would make it difficult for any judgment to be enforced: such factors would be capable of providing powerful support for a case of risk of dissipation.

v) Relevant factors include the nature, location and liquidity of the defendant's assets, and the defendant's behaviour in response to the claim or anticipated claim; past events may be evidentially relevant, but only if they serve to demonstrate a current risk of dissipation of the assets now held (National Bank Trust v. Yurov [2016] EWHC 1913 (Comm) §§ 69-70 per Males J).

vi) Where a defendant knows that he faces legal proceedings for a substantial period of time prior to the grant of the order, and does not take steps to dissipate his assets, that can be a powerful factor militating against any conclusion of a real risk of dissipation (see e.g. Candy v Holyoake [2017] EWCA Civ 92; [2018] Ch 297 § 62 and Petroceltic Resources Ltd v Archer [2018] EWHC 671 (Comm) §§ 58, 64-65).

vii) "A cautious approach is appropriate before deployment of what has been called one of the court's nuclear weapons", and "the risk is not to be inferred lightly. Bare or generalised assertion of risk by a claimant is not enough." (Tugushev v Orlov et al [2019] EWHC 2031 (Comm)) § 49 and 49(ii).

- The mere fact of delay in bringing an application for a freezing order, or that it has first been heard inter partes, does not, without more, mean that there is no risk of dissipation. 'If the court is satisfied on other evidence that there is a risk of dissipation, the court should grant the order, despite the delay, even if only limited assets are ultimately frozen by it.' Further, 'even if delay in bringing the application demonstrates that the claimant does not consider that there is a risk of dissipation, that is only one factor to be weighed in the balance in considering whether or not to grant the injunction sought.' (Madoff Securities International Ltd v Raven [2011] EWHC 3102 (Comm) at [156] per Flaux J).

- Where the claimant relies on the nature of the wrong alleged against the defendant for the purposes of supporting its case on a risk of dissipation, the strength of its case on the merits has to be considered in each context. As Henshaw J put it in ArcelorMittal v Ruia (at [213])

'I have, however, dwelt in some detail above on the transactions relating to the sale of Essar Steel India because they form a key part of AMUSA's case, not only on the merits of its conspiracy claim but also on risk of dissipation. This is an application where the events relied on to found the claim also form a key plank of the basis for alleging there to be solid evidence of risk of dissipation. In such cases, a claimant's allegations as to the underlying events need to be considered not only in the context of the good arguable case hurdle for the grant of a freezing order, but also in the context of the risk of dissipation hurdle. A case that might narrowly pass the former test will not necessarily provide sufficient foundation for finding there to be solid evidence of a risk of dissipation. It depends on the nature and strength of the case and the totality of the evidence said to demonstrate risk of dissipation.'

- Further, if and to the extent that the substantive claims cast any light on the risk of dissipation, the fact that a defendant has respectable defences to those claims has a bearing on the existence of a real risk of dissipation. (Petroceltic Resources v Archer [2018] EWHC 671 (Comm) at [21]).

- Evidence going only to difficulties of enforcement will not establish the requisite risk of dissipation. As Colman J said in Laemthong International Lines Co Ltd v ARTIS [2004] EWHC 2226 (Comm) at [54]:

'If the risk in question were merely that a claimant could not enforce a judgment because the assets were in a remote place or were likely to be illiquid or insufficient to meet a judgment, the 'just and convenient' test would become a cloak for the provision of security for the claim.'

- As to the third matter, this involves a consideration of all the circumstances of the case. Henshaw J described the matters relevant here at paragraph [230] of ArcelorMittal v Ruia, as follows:

'It is, in any event, necessary when contemplating a freezing order (as with any injunction) to consider whether it would in all the circumstances be just to impose it. This stage of the process involves taking account of the strength of the case on the merits and the risk of dissipation of assets, but also the circumstances as a whole and where the balance of justice lies. There is no exhaustive list of factors to be taken into account. Some factors often likely to be relevant are mentioned in Gee on Commercial Injunctions (6th ed) at § 12-042: the balance of prejudice between the parties; whether an order would interfere unacceptably with the interests of third parties; or whether an injunction might destroy the defendant's business.'

- One matter which might be relevant at this stage of the enquiry is if the injunction would serve no useful purpose. However, usually the court will not be deterred from granting a freezing order merely by the fact that assets may already have been dissipated. As Cooke J put it, in an oft-cited dictum in Antonio Gramsci Shipping v Recoletos Ltd [2011] EWHC 2242 (QB), if the court is satisfied of a risk of dissipation on other grounds:

'

there is no reason why the court should not shut the gate, however late the application, in the hope, if not the expectation, that some horses may still be in the field or, at the worst, a miniature pony.'

- In respect of four of the Defendants what is sought is a notification injunction, not a freezing order. It was not in issue that the essential test for such an injunction is the same as that for a conventional worldwide freezing order. This is clearly right, for the reasons set out by Gloster LJ in Holyoake v Candy [2017] EWCA Civ 92 at [36]. A notification injunction in wide terms should be granted only on the basis of such evidence of dissipation as would justify a freezing order: Holyoake v Candy at [39]-[42]. Furthermore:

'

a court should not assume that a notification injunction is necessarily less onerous than a conventional freezing order. For example, the notification injunctions here were in certain respects more onerous than a conventional freezing order would have been

' (Holyoake v Candy at [46]).

The cases made against the respondent Defendants

- It is necessary to consider, in more detail, the nature of the case made against the respondent Defendants.

- The broad nature of the case can be taken from two paragraphs of the Particulars of Claim:

[para. 46] 'This Claim concerns two conspiracies which between them involve all of the Defendants, and which each involve other persons acting or purporting to act on behalf of the Russian State and unknown others (the "Hostile Parties" and the "Conspiracies"). The Conspiracies had and have as their ultimate objective the wresting of assets from [ZM] or obtaining them for less than their fair value, and for the sole benefit of the Hostile Parties (including Transneft and ROSATOM, each of which are companies owned by the Russian State) and/or some of them and/or those that control them.'

[para. 246] 'In the premises, the parties to the FESCO Conspiracy (namely all the Defendants save for Transneft) conspired and combined together, wrongfully and with intent to injure [ZM] and/or the Claimants comprising the SGS Branch by unlawful means, in order to expropriate assets from [ZM] and/or companies controlled by him, for the benefit of the Hostile Parties (and/or some of them) and/or those that control them.'

- The claim is brought on the basis that, insofar as English, Cypriot or BVI law applies to it (including on a distributive basis), it is primarily a case in unlawful means conspiracy or alternatively a conspiracy to injure; and insofar as Russian law applies to it, it is brought under Article 1064 and/or Article 10 and/or Article 1080 of the Russian Civil Code.

- The particular cases as to unlawful means alleged against each respondent Defendant can be summarised as follows.

- In the case of Mr Rabinovich:

(1) There is 'an inferential case' made that he bribed Mr Kuzovkov in exchange for his acquiescence in the failure by the FESCO Board, of which Mr Kuzovkov was a member, to restructure or extend the loans to Maple Ridge and Sian and to authorise the bringing of the Sian Liquidation proceedings and the LCIA Maple Ridge Arbitration.

(2) There is 'an inferential case' that bribes were paid to other members of the FESCO Board.

(3) It is alleged that he 'procured Domidias' breaches of the 2012 and/or 2019 Option Agreements'.

(4) It is alleged that he procured Felix's breach of the Intimere Shareholders' Agreement.

(5) It is alleged that he 'and/or ROSATOM' instigated unlawful threats to Mr Evdokimov 'by high-ranking Russian Government officials' 'so as to procure [Mr Evdokimov] to withdraw his support for the SGS Branch's acquisition of Felix's interest in Intimere'.

(6) He misused SGS's confidential information in instructing/approving that Ermenossa write to the FAS in terms which were false and intended to frustrate SGS's exercise of the ROFO right.

- In the case of Ermenossa, it is said that Mr Rabinovich's conduct is to be attributed to it. Essentially the same allegations which are made against Mr Rabinovich in (1), (2), (4) and (6) in the preceding paragraph are also made against Ermenossa.

- In the case of Mr Kuzovkov, it is alleged that:

(1) He breached his duties to FESCO in voting not to restructure or extend the Maple Ridge and Sian loans and authorised Halimeda to commence proceedings instead, and that it is to be inferred that he was bribed to do this;

(2) It is to be inferred that he (and/or Ms Mammad Zade) pressured or induced certain directors of SGS Branch companies to act contrary to the interests of their principals.

(3) He was involved in the negotiation of the 2019 Option Agreement, which 'conferred an improper incentive on Mr Garber.'

- In the case of Mr Severilov:

(1) It is alleged that his acquisition of Domidias was prompted (and possibly financed) by Mr Rabinovich, Ermenossa and/or ROSATOM, as part of the conspiracy;

(2) That he procured Domidias's breach of the 2012 and/or 2019 Option Agreements;

(3) That, after making 'a cursory offer on behalf of ROSATOM for SGS's stake in FESCO' he 'threatened that there would be a hostile takeover of FESCO' at a meeting in August 2020;

(4) That he breached his duties to the FESCO Board by enforcing the Maple Ridge and Sian loans, and that this was 'also an abuse of process of the arbitral tribunal and the Cypriot court'.

- As to Halimeda:

(1) That it called in the Maple Ridge and Sian loans 'without authority and ... in abuse of the arbitral process and the process of the High Court of the BVI';

(2) That it 'wrongfully obtained the Cypriot injunctions in abuse of the process of the Cypriot Court' and that this was 'malicious prosecution of the respondents to those injunctions'.

- As to ROSATOM:

(1) That Ermenossa was acting on ROSATOM's behalf, and the relevant acts of Ermenossa are to be attributed to ROSATOM;

(2) That ROSATOM instigated the threats to Mr Evdokimov to procure him to withdraw his support for the SGS Branch;

(3) That the offer and threat made by Mr Severilov at the August 2020 meeting were made on behalf of ROSATOM;

(4) That individuals acting on behalf of ROSATOM subsequently met with Mr Gadzhiev and threatened that if the Claimants did not agree to sell their stake in FESCO to ROSATOM, 'means of force' would be used.

- As to FESCO:

(1) That since Mr Severilov became Chair of the Board, it had continued to seek to enforce the Maple Ridge and Sian loans;

(2) It had 'sought and obtained relief against [ZM] and SGS Branch Companies in the Moscow Arbitrazh Court'.

- As to Mr Garber:

(1) That he had breached his duties to FESCO as a member of its Board by causing Domidias to enter into the 2019 Option agreement, which 'provided him with an improper incentive conditional on the sale of the SGS Branch's stake in FESCO';

(2) That he breached his duties to FESCO when he voted to authorise Halimeda to commence the Sian Liquidation proceedings and the Maple Ridge LCIA Arbitration, and, inferentially, that he was bribed to do so;

(3) That the non-exercise of the Options and the sale of Domidias to Mr Severilov 'were carried out by Mr Garber acting in concert with Hostile Parties'.

- As to GHP, Mr Garber's alleged wrongful acts were attributable to and apply to his company, GHP.

Are Grounds Made Out for Injunctions?

- It will be necessary to consider, in relation to each of the respondent Defendants, separately, whether the requirements for the grant of a freezing or notification order are met.

Overarching points

- Before doing so, there are certain overarching matters applicable to the present application, which should be addressed at the outset.

- This was a case in which some of the respondent Defendants, on this application, challenged whether there was a good arguable case against them. I put it in that way because some Defendants, and in particular FESCO and Halimeda, did not, for present purposes, directly challenge whether there was a good arguable case, though they relied on what they said was the weakness of the case in the context of risk of dissipation. Others, namely Mr Rabinovich and Ermenossa, initially adopted that stance, but then came to contend that there was no good arguable case. The other respondent Defendants denied that there was a good arguable case against them.

- This added to the complexity of an exercise which is already by no means straightforward. There was before the court an enormous volume of material. The witness statements ran to about 400 pages; the exhibits to the Claimants' evidence were of over 5000 pages; there were over 215 pages of Skeleton Arguments. Eighteen counsel were instructed and three full days were taken up in argument. The court has to navigate between Scylla and Charybdis. On the one hand, there is the danger of proceeding on the basis that there is a good arguable case merely because there are complex allegations and an abundance of material, and because the court will not be able to resolve disputed issues. On the other, there is the danger of what has been called conducting a 'mini trial': the court getting too immersed in the detail and seeking to form a view on issues which cannot be resolved at this stage.

- There are particular problems in a case, such as the present, which alleges a conspiracy and rests, avowedly in many respects, on inference. As Wallbank J said in the Sian Liquidation proceedings, allegations of conspiracy may serve to explain many matters, if the conspiracy is taken as being sufficiently wide, but the court has to consider the evidence. What I regard this as entailing, on the present application, is that, even if I have been satisfied that there is a good arguable case in relation to at least one Defendant, I have not assumed that there is a good arguable case against another Defendant on the basis simply that the allegations against that second Defendant form part of and fit in with the Claimants' conspiracy case. Instead, it seems to me it is necessary to scrutinise the evidential base of the case against each Defendant separately.

- Moreover, I have also taken the approach that, in cases in which I have found there to be a good arguable case against a Defendant, it is best not then to give any much more detailed analysis of the strengths and weaknesses of the case made against that Defendant, unless necessary to deal with the position of another Defendant. Any such analysis would be likely to be overtaken by what will emerge during the course of the case and/or, as it was put by Knox J in In Re a Company 005009 of 1987 [1988] 4 BCC 424, be such as 'merely [to] embarrass the judge who will have to determine the question at the trial'. That was said in the context of a strike out, and the relevant considerations are not identical, but it nevertheless appears to me to be apt in the present context, and to be, as was said by Lloyd J in Bank of America Trust v Morris (22 October 1988), 'wise guidance'.

- As I will set out below, I have reached the conclusion in relation to a number of the respondent Defendants that there can be said to be a good arguable case against them. In doing so, I am not, of course, holding that the case against them will succeed. There appear to be seriously arguable objections to the Claimants' case as a whole.

- Specifically, the respondent Defendants, and in particular Mr Severilov, made a point which seems, on its face, to have a considerable amount of force. This is that the alleged objective of the Conspiracy was the expropriation of the Claimants' stake in FESCO by persons acting on behalf of the Russian State. However, if that was the objective, the Russian State did not have any need of the assistance of private individuals, or of the elaborate corporate manoeuvres which are alleged as part of the Claimants' case. The Russian State had, on the Claimants' own case, initiated the prosecution of ZM in 2018 without any involvement of the alleged Conspirators. At that point, all ZM's stake in FESCO was the subject of an interim arrest. The prosecution continued, and eventually all ZM's interest was confiscated by a Moscow Court, as part of the criminal proceedings, in November 2022.

- That does give rise to questions as to the coherence of the case of conspiracy advanced. The respondent Defendants suggest that what is said to have been done in furtherance of that conspiracy would have been wholly superfluous, because the Russian State could (and did) have all the powers it needed, and could take all the relevant steps to seize ZM's interest in FESCO without any assistance from third parties. It also gives rise to questions of causation of loss. The point put is that, once ZM's interest in FESCO had been arrested, it was available for confiscation by the Russian authorities; and has in the event been confiscated. There are issues as to whether, either because the original arrest deprived the shares of value to ZM, or because the ultimate confiscation would have happened whatever was done by way of the alleged Conspiracy, the Conspiracy caused any loss in regard to the holding in FESCO.

- A further, and related, issue is raised by various of the respondent Defendants, and in particular by Mr Rabinovich and Mr Severilov, to the effect that they, on the face of things, are among the victims of Russian state action in relation to holdings in FESCO. By the civil proceedings commenced by the General Prosecutor in late November 2022, which named Mr Rabinovich, Mr Severilov as well as ZM, and the corporate entities through which these individuals held shares in FESCO, confiscation was sought of all shares in FESCO. The decision of the Khamovnichensky District Court of 11 January 2023 held, in effect, that the shares in FESCO were the product of corruption, and that as Mr Rabinovich and Mr Severilov must have been aware of this, their shares were to be confiscated as well as ZM's interests. Both Mr Rabinovich and Mr Severilov sought to appeal that ruling.

- On its face, this is difficult to square with the Claimants' conspiracy case. The Claimants' answer is to contend that it is to be inferred that there was an arrangement or understanding between the Russian authorities whereby Mr Rabinovich and Mr Severilov would have their shares returned or be compensated for them in some way. The Defendants attack that as an implausible and unnecessary inference.

- The Court clearly cannot resolve this dispute at this stage, but I have taken the existence and prima facie strength of these points into account in making assessments of the overall strength of the Claimants' case, and their existence is, in my judgment, relevant at the stage of assessing whether a real risk of dissipation has been shown.

- I turn to consider the application against the various respondent Defendants in turn.

Mr Rabinovich and Ermenossa

- I commence with Mr Rabinovich and Ermenossa, who are said by the Claimants to be central protagonists in the alleged Conspiracy.

- In relation to the question of whether there is a good arguable case against Mr Rabinovich and Ermenossa, and as I have already mentioned, those Defendants' original position on this application was that, while it was not accepted that there was such a case, it was appropriate to concentrate instead on the issue of whether there had been shown to be a real risk of dissipation. During the hearing, however, they came to contend that there was no good arguable case.

- The case alleged against Mr Rabinovich and Ermenossa appears, at present, to have aspects which differ in strength and plausibility.

- I do, however, consider that it can be said that there is a good arguable case in relation to at least some aspects of the case against Mr Rabinovich/Ermenossa. In saying this I am, of course, not expressing any concluded view that they are correct; merely that they are supported at this stage by sufficient evidence to make them a good arguable case.

- In particular it appears to me that there is a sufficient evidential basis that there was some sort of coordination between Mr Rabinovich, Mr Severilov and ROSATOM by August 2020, that a 'hostile takeover' of FESCO was threatened, and that this was accompanied by menacing behaviour. This is based on the evidence of Mr Gadzhiev of a meeting of 26 August 2020, and of a subsequent visit of four men on or about 28 August 2020 (paragraphs 82.9-82.14 of Bushell 1). It is true that Mr Rabinovich was not at either meeting. Furthermore, cogent criticisms have also been made of the reliability of Mr Gadzhiev's account, given that the meeting of 26 August 2020 was not referred to in the initial Statement of Claim served in the BVI UMC proceedings in February 2021, and was described in anodyne terms in Mr Gadzhiev's own Affidavit in those proceedings. Nevertheless, as Mr Lord KC pointed out, Mr Gadzhiev's account made to the press (RBC) in February 2021 as to what had happened in August 2020 had involved the following: (1) that Mr Severilov had said that he was Mr Rabinovich's trustee (assuming that to be a correct translation); (2) that Mr Severilov had communicated an offer to buy FESCO 'at a price significantly below the market'; and (3) that after Mr Gadzhiev had refused to accept the offer, 'he was told that "they [viz Mr Rabinovich's representatives] would use "forceful methods"'. Furthermore, even in the BVI Statement of Claim served in February 2021, there was a reference, albeit somewhat cryptic (paragraph 89(3)) to Mr Severilov's having made the offer 'on behalf of ROSATOM'. These provide support for the account which Mr Gadzhiev has now given (through Mr Bushell) in these proceedings.

- Given this evidence, which cannot be further tested on this application, I think that there is a case against Mr Rabinovich/Ermenossa which can be said to surmount the good arguable threshold. For reasons which I will express when dealing with the cases against Mr Garber and Mr Kuzovkov, I am not, however, persuaded that there is a good arguable case, on the present material, that bribes were paid to Mr Garber or Mr Kuzovkov, whether by Mr Rabinovich or anyone else.

- I therefore turn to the question of whether there has been shown to be a real risk of dissipation.

- In my judgment a real risk of dissipation has not been shown by solid evidence. Mr Rabinovich was first sued, by the Second to Ninth Claimants, in respect of broadly the same FESCO Conspiracy, with many of the same allegations, in the BVI in January 2021. That claim sought damages, including against Mr Rabinovich, of over US$ 1 billion. Furthermore, the evidence is that he has known about the present proceedings since 25 July 2023. There is, however, no evidence that he (or Ermenossa) has taken any steps in the period since January 2021 to dissipate his (or its) assets. The Claimants' evidence itself suggests that he has maintained substantial assets, and in particular a valuable house in Highgate, in his own name, and without a mortgage during this period and to date. In my judgment this is a case in which an absence of evidence of dissipation notwithstanding notice of the claim is a powerful factor militating against any conclusion of a real risk of dissipation.

- Further, and while it is of limited significance in light of my conclusion in the previous paragraph, I consider that this is a case in which the Claimants do not genuinely consider that there is a real risk of dissipation. This is what I deduce from the fact that, when proceedings were commenced in the BVI, no freezing order was sought against Mr Rabinovich or Ermenossa. Furthermore, even after the present proceedings were commenced, the present application was not made for a further period of over six weeks thereafter, and then was made inter partes.

- The nature of the matters alleged against Mr Rabinovich/Ermenossa do not compel the conclusion that there is a real risk of dissipation. They are not, for example, allegations of the previous perpetration of a fraud through multiple companies established for that purpose, or previous instances of the movement of funds to avoid liabilities or thwart enforcement.

- Furthermore, it is appropriate in considering whether there is a real risk of dissipation to consider whether there are respectable defences available to these Defendants. I am of the view that there are, in particular for the reasons I have given in paragraphs 86-89 above.

- The final issue is whether in all the circumstances it is just and convenient to make the order sought against Mr Rabinovich and Ermenossa. I consider that it is not. I have had regard to the objections to the case made, and the absence of cogent evidence of a risk of dissipation. I have also had regard to the balance of prejudice. I accept that the grant of an injunction would be prejudicial to Mr Rabinovich, in particular because it would have an impact on KYC checks that he may face in relation to business opportunities, make financing substantially more difficult and time-consuming, and may lead to the loss of commercial opportunities, especially if the injunction was publicised by the Claimants. The extent of any such prejudice might be difficult to quantify in money terms. On the other hand, and because I do not consider that a real risk of dissipation has been shown, I do not consider that there is substantial prejudice to the Claimants in refusing an injunction.

Mr Severilov

- I turn to the case in relation to Mr Severilov.

- In his case, he challenged head on the suggestion that there was a good arguable case on the merits against him. Once again, that case has elements which appear to differ as to their strength and plausibility.

- Again, however, and for reasons I have already given in relation to Mr Rabinovich, I accept that there is a good arguable case that there was some sort of coordination between Mr Severilov, Mr Rabinovich and ROSATOM and that there was a threat of a 'hostile takeover' in August 2020. Again, the ramifications of, and inferences to be drawn from this, if established, would be a matter for trial.

- As in the case of Mr Rabinovich, therefore, I accept that there is a case against Mr Severilov which clears the good arguable hurdle.

- I turn to the question of whether it has been shown by solid evidence that there is a real risk of dissipation. I do not regard the Claimants' case on the merits against Mr Severilov as itself constituting solid evidence to that effect. The matters in which Mr Severilov can be said to be directly involved do not constitute behaviour involving or analogous to the movement of assets to avoid judgment.

- Furthermore, the Claimants have been making allegations of a conspiracy, though not naming Mr Severilov as a defendant, since early 2021. The evidence is that Mr Severilov has known about those proceedings since Domidias and Merbau were served with them on 5 March 2021. There is also evidence that Mr Severilov has expected the present proceedings vis à vis Domidias since at least October 2022. The present proceedings became known to Mr Severilov on 26 July 2023. The Claimants' solicitors exhibited a copy of the Claim Form to a witness statement in the Commercial Court Option Proceedings on 11 August 2023. The Claim Form and application for a WFO were served on Mr Severilov on 4 September. The previous hearing was adjourned without any order made or undertakings given. Notwithstanding these matters, there is no evidence of dissipation by Mr Severilov.

- The Claimants seek to rely on the fact that the alleged bribe paid to Mr Kuzovkov was paid via a bank called Locko Bank. I have set out below why I do not consider that I can place weight, at this hearing, on the allegation of a bribe being paid to Mr Kuzovkov. In any event, the supposed link with Mr Severilov appears weak. While the Claimants have said that Locko Bank 'is owned and controlled by Mr Severilov and Mr Rabinovich', this does not appear to be correct. The evidence which was shown to me indicates that Mr Severilov had a share in the bank of 4.792%; and even taken with Mr Rabinovich's share, they had a total of less than 20%. In any event, the fact, if it is a fact, that there was a payment via an account at the bank does not show that an owner of a minority stake in the bank knew about it, and is not solid evidence that there is a real risk that he will dissipate assets.

- The Claimants also rely on the evidence that Mr Bushell gives as to what the Claimants received from a "confidential third-party source" as to what a Mr Tylenev, a former director of Cypriot companies ultimately owned by Mr Severilov, had told the source. [ref Bushell 1 para 374.4] This was to the effect that the principal activity of Mr Severilov's Cypriot companies was to launder money from Russia and that he had set up a number of companies with Mr Tylenev's passport details without his knowledge. Mr Severilov has put in witness statement evidence: that Mr Tylenev used to be his employee; that Mr Severilov lent him money to publish a book, which Mr Tylenev did not repay, and in respect of which Mr Severilov obtained a judgment against Mr Tylenev in the Arbitrazh Court of Moscow Oblast; and that Mr Tylenev has now been made bankrupt as a result. While I cannot say whether this is, as Mr Severilov suggests, the motive for what Mr Tylenev has said, I do take the view that the double hearsay of Mr Tylenev's allegations cannot be taken as solid evidence of a risk of dissipation.

- Again, I take into account in considering the risk of dissipation the fact that, for reasons which I have given, there are respectable defences available to Mr Severilov.

- In my judgment, a real risk of dissipation has not been shown. Furthermore, the Claimants' conduct of the proceedings indicates, in my view, that they do not have a genuine concern that there will be dissipation.

- Finally, in relation to the issue of whether it is just and convenient to make the order sought, I conclude that it is not. This is for very much the same reasons as in the case of Mr Rabinovich/Ermenossa.

Halimeda and FESCO

- I turn to the cases against Halimeda and FESCO.

- What is sought against each of these Defendants is a notification injunction. As already set out, the requirements for such an injunction are the same as for a WFO.

- Each of these Defendants took, and maintained, the stance that they would not, for present purposes, contest that there is a good arguable case; though they maintained that the weakness of the cases made against them was relevant to whether there had been shown to be a real risk of dissipation.

- Each of these Defendants did, however, vigorously contest that there had been shown to be a real risk of dissipation. In my judgment, they were clearly right to say that no such risk had been shown by solid evidence.

- In relation to Halimeda, it has been litigating issues relevant to the present claims since 2020. The allegation that Halimeda was a party to a conspiracy was made in the Sian Liquidation proceedings in November 2020. Halimeda was sued by the Second to Ninth Claimants, in the BVI, on the basis of substantially similar allegations as are now made, in January 2021. There is, however, no evidence of anything done by Halimeda, in the interim, which can be said to show a real risk that it might dissipate assets. This does seem to me to be a case in which this is a powerful factor against a conclusion that there is a risk of dissipation.

- The points which the Claimants have relied upon to indicate a risk of dissipation by Halimeda are not, in my judgment, persuasive ones.

- The first is that there is said to be new evidence which has now made it possible to seek an injunction; and there is a suggestion that the net is closing in around the Defendants, making it more likely that they will now dissipate assets. However, the new evidence to which reference is made is only new to a limited extent, and most of it was presented to Halimeda in other litigation some months ago. Evidence of the alleged bribery and of alleged incentive payments to Mr Garber were included in Maple Ridge's draft re-amended pleading in the Maple Ridge LCIA Arbitration in April 2023. Most of the rest of the additional evidence referred to by the Claimants in this connexion was set out in Mr Gadzhiev's evidence in the BVI UMC proceedings in May 2023. None of the new evidence relied upon in this connexion relates to things done by Halimeda.

- The second is the suggestion that, as Halimeda was a participant in the conspiracy that is itself indicative of a risk of dissipation. However, in relation to Halimeda, its participation in the conspiracy is said to be (1) that it enforced the loans against Maple Ridge and Sian; and (2) that it obtained an injunction in the Cyprus courts. Neither seems to me to be of a nature which is itself significant evidence that Halimeda may dissipate assets.

- The third is that points applicable to the risk of dissipation by FESCO are applicable to Halimeda. I consider those below.

- The fourth is that Halimeda sold shares in PJSC Transcontainer in 2018 for a price of US$ 227 million, and Mr Bushell has said that he does not know what happened to the proceeds. This historical disposal of an asset cannot be regarded as evidence of a risk of dissipation; especially as the evidence from Mr Privalov is that the proceeds were used for a normal business purpose, namely repaying loans which Halimeda had obtained from FESCO.

- In relation to FESCO, the position is similar. While FESCO was not named as a defendant in the BVI UMC Proceedings, the evidence is that it was apprised, throughout, of the claims and allegations made both by and against Halimeda, its wholly-owned subsidiary. Again, in my judgment, the fact that, notwithstanding these matters, there is no evidence of dissipation, militates powerfully against a conclusion that there is such a risk.

- The Claimants seek to rely on the nature of the conspiracy as supporting such a risk. As far as FESCO is concerned, the only steps which FESCO itself is said to have taken are: (1) that it has continued to seek to enforce the Maple Ridge and Sian loans in the Maple Ridge LCIA arbitration and the Sian Liquidation proceedings; and (2) that it has sought and obtained relief against ZM before the Moscow Arbitrazh Court. That a party would deploy those legal processes is not in my view good evidence that it may seek to dissipate assets.

- Furthermore, in the case of FESCO, there is evidence that it is a substantial company with extensive assets both in Russia and overseas. It is the largest logistics company in Russia, and comprises over 100 entities globally. Its overseas assets portfolio includes port, railway, and logistics capabilities and operations in many countries, especially in the Asia-Pacific Region. It owns 28 vessels, directly or indirectly; and has a container fleet of 83,298 units. It has recently started a new railway service between Russia, Netherlands, Italy and Germany. Many of these assets would, of their nature, be difficult to dissipate.

- The fact that many of these assets may be in Russia, and thus be difficult to enforce against, is not of itself evidence of a risk of dissipation. Insofar as the Claimants raise the possibility that FESCO might repatriate to Russia its overseas assets, I regard there as being little support for this expression of fear. The matter most relied on by the Claimants is what is said to be a 'general policy of the Russian state to encourage movement of assets back to Russia by Russian entities and businesspersons (ie "repatriation" of assets).' The Claimants have adduced evidence to the effect that President Putin 'has long encouraged Russian companies and wealthy individuals to repatriate capital and assets held overseas.' This encouragement would appear, however, to be inapplicable to an entity such as FESCO. Mr Zvyagintsev's evidence, which seemed to me entirely plausible, was as follows:

(1) That FESCO's operations outside Russia have in various respects recently increased, not decreased (including a larger marine tonnage, more containers in its fleet, new representative offices in Central Asia, and new services and shipping lines between Vietnam, Turkey and Russia);

(2) In relation to the repatriation policy: 'While it may be true that a number of Russian companies have transitioned their offshore holdings to Russian Special Administrative Regions, the structure and operations of the FESCO Group differ significantly from those companies

FESCO's international subsidiaries are not simply securities holding entities, rather they have core operational roles within the business. The idea of a complete or a substantial "repatriation" of such assets would be wholly incompatible with the nature and location of FESCO's international operations.'

(3) Repatriation would be damaging to FESCO's operations, for at least the following reasons: (a) the preference of its clients since 2022 for vessels with ownership structures which minimise connexions with Russia; (b) the nature of its global operations requires it to have a physical presence in its various clients' jurisdictions; and (c) engagement with local banking institutions and service providers is essential to FESCO's operations.

- I have also taken into account, for reasons which I have given, that FESCO and Halimeda have at least respectable defences to the claims made against them.

- In these circumstances I do not consider that the Claimants have shown a real risk of dissipation of assets.

- I also consider that, as a matter of justice and convenience, the case is not one in which a notification injunction should be granted. Certainly it appears to me that that sought by the Claimants in their application would be very onerous for FESCO, for the reasons given by Mr Zvyagintsev in paragraphs 53-57 of his witness statement. Although Mr Lord KC said that the financial thresholds could be adjusted if the court thought fit, this did not appear to me a sufficient answer to the point. While the court is often prepared to make some adjustment to such thresholds, the scale of the adjustment here would need to be very material to have the effect that any resulting order were not extremely onerous. Any resultant order would be practically a different order from the one which the Claimants sought in their application to which the Defendants have responded in evidence and argument. Given this, and given the paucity of evidence of a risk of dissipation, and my assessment of the overall merits of the case, insofar as it is possible to estimate at this stage, as one in which the Defendants have at least respectable defences, I do not consider that it is appropriate to grant an injunction as sought.

ROSATOM

- ROSATOM argued that there was no good arguable case against it. I am prepared to accept, however, that there is, again in large measure because of Mr Gadzhiev's evidence in relation to the August 2020 meetings.

- I do not, however, consider that it is necessary to delve into this in greater detail, because I am of the clear view that there is no real risk of dissipation supported by solid evidence.

- ROSATOM is a Russian state corporation, established by the Russian Federation and tasked with implementing Russia's government policy on nuclear power and the use of nuclear energy. ROSATOM has a direct interest or shares in 52 companies, all but one registered in Russia. Outside Russia it has no bank accounts or real estate, but does have trademarks registered in many countries, some vehicles (for example cars of employees of foreign missions) and some office equipment in Belarus. Thus, as Mr Riem says in his witness statement, the vast bulk of ROSATOM's assets are already within Russia, as has always been the case. This, which may give rise to difficulties of enforcement, does not support the grant of a freezing (or notification) order. Insofar as any significant assets are overseas (in particular the trademarks) there is no real risk of their dissipation because of their nature.

- As to the ROSATOM Group, whose relevance for these purposes ROSATOM does not concede, but whose position is in evidence, this comprises over 400 organisations. It has assets of around US$67 billion and operates in some 50 countries. The evidence is that its main overseas assets cannot be dissipated, because they are largely either production assets (ie nuclear or hydroelectric power plants), uranium mines, uranium exploration licences or other joint ventures relating to uranium or other trading operations.

- The evidence before me indicates that in 2022 ROSATOM took steps to expand its support for major overseas projects. These are largely if not entirely the subject of intergovernmental agreements between the Russian Federation and the government of the relevant overseas state; and ROSATOM acts as a competent authority for the purpose of implementing the relevant agreement on behalf of the Russian Federation. These agreements have to be carried out in accordance with the legislation of the state parties and on the basis of international treaties to which the relevant states are party. I agree with the submission made by ROSATOM that it is very difficult to conceive that ROSATOM could or would liquidate, dissipate or repatriate any significant proportion of such of these assets as it owns.

- Furthermore, there is no evidence that, since the commencement of these proceedings, ROSATOM has taken steps to seek to dissipate or repatriate any assets.

- There is, therefore, in my judgment, no solid evidence of a real risk of dissipation.

- As to the issue of the justice and convenience of the order, I consider that it would not be just or convenient for an injunction to be granted. Here I have not only taken into account my assessment of the strength of the case as being one to which there are at least respectable defences, and the lack of cogent evidence of a risk of dissipation, but also the nature of the relief sought. The order sought would be very onerous for an organisation such as ROSATOM, for the reasons given in paragraphs 41 to 45 of Mr Riem's witness statement.

Mr Garber and GHP

- The case in relation to Mr Garber and GHP needs careful separate consideration.

- The allegations against Mr Garber and GHP are limited. This is unsurprising as Mr Garber sold Domidias in late September 2020. I have already set out a summary of the matters alleged against him.

- I have concluded that these do not amount to a good arguable case.