This judgment was handed down remotely by the judge and circulated to the parties' representatives by email and release to The National Archives. The date and time for hand-down is deemed to be Friday 3 November 2023 at 10:00am

Mrs Justice Cockerill:

INTRODUCTION

- In late 2007, as clouds gathered in the sub-prime mortgage market, the Claimant ("L30") paid US$100m to the Defendants ("CS") for certain Notes ("the Notes"), rated AAA, which formed the basis of what is known as a synthetic CDO transaction. Such transactions are complicated indeed some of the banking witnesses in this case struggled to explain the concepts themselves.

- But the bottom line is this: the financial crisis hit, L30 lost its money in 2010 and seeks to claim that money back. It says that this was more than a bad deal. It says that in selling the transaction CS made representations about the business packaged within the CDO transaction, that the representations were false, made either negligently or deliberately, and that L30 would not have done this deal if the representations had not been made.

- L30 has likened the transaction to a Russian doll; that analogy is apt; and it in part explains the complexity of the issues which have been raised and hence fall to be decided. The Notes were not self standing; they were linked via a credit default swap ("CDS") to the credit of a reference portfolio which comprised 100 residential mortgage-backed securities ("RMBS"). Each RMBS itself packaged a number of underlying individual mortgage transactions, in that it comprised rights to cash-flows arising from pools of underlying mortgage loans. Of those 100 RMBS, 7 RMBS were ones which had been packaged, securitised or underwritten by CS (or its affiliates) (the "CS RMBS[1]").

- The bare essence of the claim is that:

i) In relation to the CDO transaction CS represented that it was unaware of any conduct on its part which tainted the credit quality of the Notes or the CS RMBS or which otherwise undermined the reliance which could be placed by an investor in L30's position on the credit ratings ascribed both to the Notes and the CS RMBS;

ii) However CS knew that the credit risk which L30 believed it was buying was not the credit risk it was actually buying; in that it knew that the CS RMBS embedded within the CDO transaction were either affected by or were exposed to a material risk of being affected by certain misconduct in the selling of the RMBS between 2005 and 2007. This is referred to as "the RMBS Misconduct";

iii) Those allegations of misconduct are complicated they comprised about 70 pages of pleading and (in schedule form) 5 pages of the List of Issues. At the centre of them however were allegations that CS had represented to the CS RMBS investors certain things about the rigorousness of its compliance and due diligence processes and (in particular) that decisions as to loans were not "farmed out". It is said that these representations were, to the knowledge of CS and numerous people involved in the RMBS process, untrue.

- The misrepresentation case therefore encapsulates a myriad of issues, some factual, some legal: was there any RMBS Misconduct in relation to the CS RMBS? Are there representations in relation to the CDO transaction and if so what? With what intent and what knowledge were they made? Did they induce L30 to buy the Notes? This latter question includes legal issues as to the right test for what L30 needs to have known or understood or been aware of in relation to such representations.

- There are also issues as to limitation. This claim was commenced in late 2018. No legally aware reader will have missed the elephant in the room: on the face of it, all of these claims are long since time barred. There are therefore questions as to whether L30 lacked, as it says it did, the requisite knowledge or information to start the limitation clock running.

- Finally there are issues on negligence, as a backup if the fraud case does not work, but the other features of misrepresentation are present; and a rarity an unlawful means conspiracy case which is a genuine alternative to the primary case.

- These issues are dealt with in greater detail below, under the following headings:

i) Factual Background

ii) The Trial

iii) Limitation

iv) Were the CDO Representations made?

v) Were the CDO Representations relied on?

vi) Falsity: RMBS Misconduct (Summary)

vii) Knowledge of Falsity

viii) Other Issues

a) Negligence

b) Unlawful Means Conspiracy and Irish Law

ix) Conclusion

x) Appendices:

a) Appendix 1: RMBS Misconduct (detailed findings)

b) Appendix 2A: CDO Representations (pleaded)

c) Appendix 2B: CDO Representations (revised for trial)

d) Appendix 3: RMBS Misconduct allegations

FACTUAL BACKGROUND

Agreed Background to the types of securities involved in the Transaction

- As already stated, the Notes were a CDO, with the underlying reference assets being a portfolio of RMBS. The exposure to that portfolio of RMBS was synthetic, created through use of a CDS.

- This overview, taken largely from a helpful document agreed by the parties, summarises the general features and characteristics including in respect of the specifics relevant to the Notes themselves, of:

i) RMBS;

ii) Collateralised debt obligations ("CDOs"); and

iii) CDS and their use in a synthetic CDO structure.

RMBS

- An RMBS is a type of asset-backed security in which, as the name indicates, the securitized assets are residential mortgage loans. As with any asset-backed security, an RMBS is a structured financial instrument.

- A single RMBS may be backed by thousands of individual mortgage loans. These loans are originated by companies offering mortgage finance to residential property owners. The originator may be connected with the sponsor entity, or may instead be a third party company which sells on loans it has originated to be securitised by a different financial institution.

- The process of securitising an RMBS starts with the pooling of residential mortgages by a "sponsor" entity, which has originated or otherwise acquired those assets in order to pool them. This pooling of assets usually takes place in an entity related to the sponsor known as the depositor. The depositor then typically conveys the pool of loans to a special purpose securitisation trust, which then issues securities that are backed (or collateralised) by the assets and sells them into the market. The RMBS securities entitle investors to a periodic payment of interest, which flows primarily from the monthly revenue generated by the underlying mortgages, and a return of principal upon maturation of the securities.

- RMBS securities are split into tranches to be sold to investors with different purchasing requirements. As such, RMBS generally consist of multiple tranches, which are typically differentiated by their risk profiles, and thus credit rating. No particular underlying mortgage is assigned to a particular tranche of the RMBS; rather, the mortgages as a pool collectively back all of the tranches in a particular RMBS. In general, lower risk / higher credit-rated tranches (referred to as "senior" tranches) have lower yields than higher risk / lower credit-rated tranches ("mezzanine" and "junior" tranches). Cash flows in an RMBS are structured such that the senior tranches receive the first "cut" of principal / interest payments when those are made, before mezzanine and junior tranches; and generally any losses of principal or shortfalls of interest from the portfolio of loans as a whole are similarly borne starting from the most junior tranches and moving upwards to the senior tranches.

- Purchasers of RMBS receive interest and principal amounts repaid by the original mortgage borrowers of the individual loans that were pooled into the RMBS, but are also exposed to the risk of those borrowers failing to keep up repayments or defaulting. As such, where a sufficient number of those underlying borrowers fail to make repayments, or (for example) default on their loans, this may ultimately lead to the RMBS suffering a loss. Such losses are felt first by the higher risk / lower credit-rated tranches (i.e. the junior tranches), are often referred to as "writedowns".

CDOs

- A CDO is a financial instrument that is similar to an RMBS insofar as it pools a number of underlying assets (in this case debt instruments) into an investment vehicle that then issues new bonds or notes to investors. Like RMBS, the securities issued by the CDO are typically divided into tranches with varying interest rates and credit parameters. The assets held by a CDO can be any type of debt obligation, including, but not limited to, corporate debt, RMBS or even tranches of other CDOs.

- As described in the context of RMBS above, tranches of a CDO will be categorised by risk profile. A CDO is generally divided into multiple tranches, with senior tranches generally the first to receive returns and last to suffer any loss. The point at which a tranche would start to suffer a loss is commonly described as the "attachment point" and expressed as a percentage of the value of the underlying pool of assets. The term "detachment point" is commonly used to describe the point at which a tranche would suffer a total loss.

- CDOs may be "managed" or "static" in terms of their pools of underlying assets. "Managed" deals require a CDO manager, who, subject to the specific terms of the CDO and within stipulated investment parameters, "manages" the underlying collateral or assets during the life of the CDO by actively trading in the underlying assets for example, by substituting out non-performing assets. By contrast, a "static" structure generally means that during the life of the CDO the pool of underlying assets is fixed from the outset. This removes the need for a CDO manager, although the initial selection of the portfolio is often made by, or with, the assistance of a manager.

- It is not always necessary for a CDO to acquire the assets that form the basis of the CDO. Instead, it is possible to create exposure to the chosen assets without purchasing the actual assets via a derivative structure, typically by using a CDS. CDOs constructed in this manner are referred to as synthetic CDOs. The way a CDS works to create this exposure is described below.

CDS and Synthetic CDOs

- Put simply, a standard CDS is a contract that transfers credit risk associated with a third party entity or asset from one party (the "Protection Buyer") to another (the "Protection Seller"). In consideration for the Protection Buyer paying the Protection Seller periodic premiums, the Protection Seller agrees to pay out an agreed sum contingent on the occurrence of certain defined credit events. If a credit event occurs, this will generally trigger payments from the Protection Seller to the Protection Buyer; this is the "swap" element, as the Protection Buyer has effectively swapped the risk of that credit event with the Protection Seller, such that the Seller has taken on that credit risk in respect of the underlying asset. In many ways, a typical CDS functions similarly to insurance, whereby the Protection Buyer pays an agreed upon premium and the Protection Seller provides a payment if the underlying third party entity or asset defaults, i.e. causes losses.

- The definitions of credit events are critical parts of CDS documentation as they describe the circumstances in which payments may flow from the Protection Seller to the Protection Buyer and how settlement may occur. Standard RMBS credit events were defined by ISDA, with Protection Sellers making monthly floating payments equal to the incremental losses on the underlying reference assets reported in any given month.

- In the context of a synthetic CDO, the CDS element is used to create exposure to an asset without the need to purchase the actual asset. Rather than the issuer of the CDO actually acquiring the asset (for example, the portfolio of RMBS), it becomes a Protection Seller, entering into a CDS with a counterparty (the Protection Buyer), which is usually an affiliate of the broker/dealer arranging the CDO. The Protection Seller then has a contractual exposure to the credit risks of the underlying reference asset without actually owning it, and receives compensation/premiums in return from the Protection Buyer. As such, where the reference asset is performing, the CDS counterparty (the Protection Buyer) will make regular payments to the CDO issuer (which, in turn, funds payments to the CDO investors). Following a credit event, however, the CDO issuer will be required to make payment(s) pursuant to the credit protection it has sold to the CDS counterparty (the Protection Buyer), which it funds from the investment made into the CDO by investors, reducing the principal amount of the bonds / notes held by those investors. At the transaction's maturity, the proceeds of the investments (if any) are used to repay the remaining principal amount of the bonds / notes to investors.

- In order to fund the premiums which it needs to pay to the Issuer under the terms of the CDS, and to hedge its exposure, the counterparty will typically enter into hedging arrangements with other market participants, for example in the form of further CDSs (where the swap counterparty is the Protection Seller). The following section concerning the Notes addresses only the relationship between the Issuer and Noteholders and the Issuer and the swap counterparty and does not address any hedging transactions which took place between the counterparty and other market participants.

CS's RMBS business a brief outline

- The RMBS business and RMBS Misconduct allegations are considered discretely in one of the Appendices to this judgment. The key background information about it can be summarised thus.

- The business model of CS' Structured Products group on the RMBS side (the "RMBS Group") during the Relevant Period was to acquire loans through various acquisition channels and then either to package these loans into RMBS, which Credit Suisse (USA) LLC ("CSSU") sold to investors, or to sell them as part of a portfolio of loans to other financial institutions through "whole loan sales".

- CS' business of acquiring loans onto its own book was known as the Conduit. The Conduit had four separate "channels", (1) the "Bulk Channel"; (2) the "Mini-Bulk Channel"; (3) the loan-by-loan channel ("LBL Channel"); and (4) the "Wholesale Channel".

- In respect of loan pools in the Bulk and Mini-Bulk Channels, acquisition was processed by CSSU "Trading Desks". At points during the Relevant Period, the Co-Heads of Non-Agency Trading in the RMBS Group were Mr Daniel and Mr Schoen while Messrs Dodman (Subprime), Schoen (Scratch and Dent), Daniel (Fixed Rate), and Vibert (Adjustable-Rate Mortgage, or "ARM") all headed a desk.

- The Trading Desk produced a bid price for the loan pool which was offered by the seller. If the bid was accepted by the seller, then CSSU carried out due diligence on the loan package. Sometimes sellers imposed stipulations (called "trade stips") on which the sale of the pool was conditional.

- Following the due diligence results, CSSU and the seller agreed a final pool of loans it would purchase.

- Through the LBL Channel, approved sellers could access an online CSSU portal whereby an automated process compared the seller's input loan characteristics with CSSU's acceptable loan parameters and automatically produced to the seller a denial or a purchase price for the loan.

- The Wholesale Channel process was of CSSU originating its own loans. A broker inputted the prospective loan characteristics into an online portal which automatically issued either an initial approval (with or without conditions) or a denial. If the loan was approved, the broker would be instructed to send the full loan file to a Fulfilment Centre - a third party designated to underwrite CSSU's Wholesale loans subject to criteria given to them.

- A critical part of the process for the purposes of this dispute was the due diligence ("DD") process, to ensure that loans being acquired and securitised were sufficiently good quality .

- Other than the Wholesale Channel, where CSSU was the underwriter, CSSU performed pre-acquisition due diligence on loans (sometimes by way of sample in relation to certain categories of loans). CSSU's due diligence process varied by acquisition channel.

- Due diligence in the Bulk Channel was overseen by the Credit and Underwriting Group, headed by Mr Sacco, though it was principally "Bulk" due diligence managers such as Mr Nordyk of that group who supervised it. Due diligence in the LBL and Mini-Bulk channels (and underwriting in the case of the Wholesale Channel) was overseen by the Funding and Fulfilment Group, which supervised and was responsible for the Fulfilment Centers. The Head of this group was Mr Othman.

- Due diligence reviews principally involved three main elements: (1) a credit review; (2) a compliance review; and (3) an appraisal review.

- In the Bulk Channel, loans were allocated an "event level grade" referred to as EV1, EV2 and EV3 in respect of their credit and compliance review. The import of an EV grade is in issue between the parties.

- CS operated a Quality Control ("QC") process on loans it acquired. This was run by the Credit and Underwriting Group. QC was a monthly process which involved subjecting a sample (usually 3%) of the total loan volume purchased through the Bulk, Mini-Bulk and LBL Channels and originated through the Wholesale Channel to a QC review.

- The process of putting together an RMBS deal was a continuum. A part of the process and generally what one might term an "early stage" part involved the making of presentations, illustrated by Presentation Slides. To some extent these were put together to educate newcomers to the market or newcomers to business with CS. To some extent of course, since CS was in the business of putting together a successful product the Presentation Slides formed part of a sales effort. The Presentation Slides were not intended as contractual documents. Often it can be seen that points made in the Presentation Slides are summaries, or "jumping off points". The presentation would be oral and in large measure the Presentation Slides were intended to summarise or navigate what was being said. Any representations which came from a presentation would have to be representations which were the result of the oral and slide presentations. Those might coincide and the result might be that a presentation did result in a representation being made in the form of something which appears on a slide. However what was said/shown needs to be assessed against the full background of the presentations and the other documents which succeeded these early stage communications.

- There were then Offering Documents namely the Prospectus and the ProSupp. They provided information required by law about the offering of securities. The Prospectus (which has been described as covering a whole "shelf") set out general information, and often indicated a range of possible approaches which could be adopted in the ProSupp for any particular deal. The ProSupp (itself lengthy) "supplemented" that Prospectus with specific information for a particular deal as well as a good deal of material provided for a regulatory purpose in accordance with the SEC's Regulation AB. It provided detail about the structure and nature of the warranties being provided. For example it might explain that the Seller acquired loans from third parties and that, as part of the securitisation, it "will make certain representations and warranties to the depositor and the trustee regarding the mortgage loans", and refer to the repurchase/substitution obligation. It would describe the contracts pursuant to which the RMBS were created - the Pooling and Servicing Agreements ("PSAs") - and summarise representations to be found in that document. It would also contain a number of sections upon which L30 relies indicating that it was a document upon which some reliance was intended to be placed (such as "you should rely on information contained in this document

") and giving (for example) some information about the mortgage pool indicating that the information in the ProSupp was believed to be representative of the characteristics of the loans to be included in the mortgage pool.

- The securitisation of loans and their offer to investors took place pursuant to a detailed contractual framework, with heavy legal involvement from specialist law firms working with market standard documentation. The relevant contractual (and other) documents for these arrangements extended to many hundreds of pages of carefully drafted text.

- As just noted, the PSA is the contract pursuant to which the loans were transferred to the trust, and which sets out the terms on which they do so. As L30 submitted, the PSA does not necessarily affect whether representations were made elsewhere. However the PSA must form a part of the context against which the existence of such alleged representations is considered.

- Each PSA contains a long list of representations and warranties. For example, taking the PSA for CSMC 2007-3, it is a document of nearly 300 pages (with schedules and exhibits). The following features are worthy of note:

i) The parties were the Seller (DLJ, an affiliate of CSSU), the Depositor (Credit Suisse First Boston Mortgage Securities Corp, another affiliate of CSSU), the Servicers (Wells Fargo, SPS and others) and the Trustee (US Bank);

ii) The Mortgage Loans were conveyed to the Trustee in trust for the benefit of Certificateholders by the Depositor (who had in turn been assigned the Mortgage Loans by the Seller under an Assignment and Assumption Agreement);

iii) There is a discrete section which addresses representations and warranties given by the Seller, which are then set out in a series of schedules;

iv) Under the agreement the Seller makes the representations and warranties applicable to the Mortgage Loans. 29 of these are listed in a schedule. Some are made to the Depositor and some to the Trustee and to others;

v) These representations/warranties relate to an exceptionally wide range of matters including that:

a) The Mortgage Loans are not 30 days or more delinquent and that there are no material defaults under their terms;

b) All taxes, insurance premiums, water, sewer and municipal charges which have become due had been paid;

c) Each Mortgage Loan at the time it was made complied in all material respects with applicable federal, state or local laws;

d) The Mortgage Loan complies with all the terms, conditions and requirements of the originator's underwriting standards in effect at the time of origination;

e) The Mortgage File contains each of the documents specified in the PSA;

f) Each Mortgage Loan has a loan-to-value ratio of 100% or less.

vi) The Depositor made only very limited representations concerning the conveyance of good title;

vii) There were no representations about the Seller or the Depositor's knowledge of the state of affairs, or about its procedures;

viii) There is a scheme which addresses the consequences of breach of representation/warranty the existence of which suggests that the existence of some breaches was regarded as at the very least possible (though it has been described by the Court of Appeals of the Fifth Circuit in Lone Star Fund v Barclays as "inevitable"). In summary, upon discovery of any breach that "materially and adversely affects the interests of the Certificateholders

in any Mortgage Loan" the party discovering the breach is to give prompt notice of the same, with the Seller promising that within 90 days of such notification of a material and adverse breach, it will either cure the breach, substitute a compliant loan, or repurchase the Mortgage Loan;

ix) Under the terms of the PSA that is the sole remedy:

"It is understood and agreed that the obligation under this Agreement of any Person to cure, repurchase or substitute any Mortgage Loan as to which a breach has occurred and is continuing shall constitute the sole remedy against such Persons respecting such breach available to Certificateholders, the Depositor, the Trustee or the Trust Administrator on their behalf."

x) The result is that under the PSA the risk of breaches was place on the Seller.

L30 and the Rhineland Programme

- In 2002, a German bank, IKB Deutsche Industriebank AG ("IKB") established an asset-backed commercial paper conduit which became known as the Rhineland Programme. The Rhineland Programme consisted of a Delaware corporation (the Rhineland Funding Capital Corp or "RFCC") and a series of special purpose companies, most of which were registered in Jersey ("the Rhineland SPCs"). Bedell Trust Company (later known as Ocorian) provided administrative and operational support to the Rhineland Programme, and (along with a then associated law firm, Bedell Cristin), provided professional directors for the Rhineland SPCs. L30 became one of the Rhineland SPCs following its incorporation on 4 January 2007. RFCC issued short-term secured commercial paper and lent the money so raised on to the Rhineland SPCs for them to invest especially in CDOs.

- At first, IKB itself was responsible for identifying potential investments for the Rhineland SPCs and advising those companies which investments they should purchase. However, in 2006 IKB incorporated a subsidiary called IKB Credit Asset Management GmbH ("IKB CAM") to take over this role, which was returned to IKB upon IKB CAM's dissolution in 2008.

- The procedure that was followed when IKB CAM made a recommendation was documented in a Tradeable Securities Investment Advisory Agreement dated 21 December 2006 (the "TSIAA"). In summary, the TSIAA provided for IKB CAM to make a recommendation to the Rhineland Programme's Tradeable Securities Investment Committee (the "TSIC"), which would consider and approve the recommendation. The recommendation would then be sent on, together with the TSIC's approval, to a Rhineland SPC whose directors would consider and approve the acquisition of the investment. IKB CAM would then assist the Rhineland SPC to conclude the acquisition of the investment from the seller. Certain administrative tasks, such as the execution of any funding agreement required between the Rhineland SPC and RFCC, would be arranged by Société Générale, the Rhineland Programme's administrator.

- In addition, IKB was a liquidity facility provider to the Rhineland SPCs. This meant that IKB was obliged to lend the Rhineland SPCs money in certain circumstances, including where a Rhineland SPC lacked the funds to make debt repayments to RFCC.

The Notes: structure

- L30 purchased the Notes from the Third Defendant ("CSSU") acting through its agent Credit Suisse Securities (Europe) Limited ("CSSEL") for USD 100m in a transaction which was entered into on or around 13 July 2007.

- The Notes were issued by Magnolia Finance II plc ("Magnolia") and were structured as a synthetic CDO. CSSEL and CSI were the arrangers of the Notes. The underlying reference assets for the CDO were 100 RMBS (described as the "Reference Obligations"). The Reference Obligations were set out in a Reference Obligation Schedule (the "Reference Portfolio") shown in Annex B of a Series Memorandum dated 25 July 2007 ("the Series Memorandum"). The Series Memorandum is a document 196 pages in length.

- The Series Memorandum had been preceded by Termsheet (i.e. documents setting out draft indicative terms, subject to documentation, pricing, and relevant approvals). The Term Sheets for the proposed Notes sent on behalf of CSI and CSSU to IKB CAM were about 30 pages long. They recorded that the selection of the Reference Obligations for inclusion in the Reference Portfolio was the responsibility of Principal Global Investors ("PGI"). The Reference Portfolio was (subject to certain adjustment rights) static, i.e. once fixed prior to the sale of the Notes, the Reference Obligations did not change. As such, L30, as the investor / purchaser of the Notes, was exposed to the performance of those 100 RMBS (and their underlying mortgage loans) for as long as it held the Notes.

- The Notes therefore represented "long" exposure on the part of L30 to the Reference Obligations, in that they broadly simulated a scenario in which it was holding itself the Reference Obligations (subject to their weighting in the Reference Portfolio and to the attachment and detachment point provisions). The exposure to each Reference Obligation was weighted up / down (as appropriate) in the Reference Portfolio such that they each had a notional value of USD 10 million, despite the "original principal amount" of the individual Reference Obligations (which, broadly, reflected the value of each underlying RMBS) being of differing values. As a result of this weighting, the Reference Portfolio had a total notional value of USD 1 billion, reflecting the USD 10 million notional value of each of the 100 Reference Obligations.

- So, for example, tranche "M5" of the RMBS "JP Morgan Alternative Loan Trust, Series 2006-S4" (row 56 of Annex B of the Series Memorandum) had an "original principal amount" of USD 4,375,000 and therefore was weighted upwards by approximately 228.57% to create the synthetic exposure to the notional amount of USD 10 million in the Reference Portfolio. But in respect of the Reference Obligation in the next row (i.e. row 57), its "original principal amount" of USD 43,279,000 needed to be weighted downwards by approximately 23.11% in order to create the USD 10 million notional value.

- The Notes were linked to a tranche of the CDO that had an attachment point of 9% and detachment point of 19%. This meant that the principal value of L30's investment would not be diminished by any negative performance of the Reference Obligations until notional losses on the Reference Portfolio reached USD 90 million (i.e. 9% of USD 1 billion). L30 would suffer a total loss on its investment if the notional losses reached (and stayed at) USD 190 million or more (i.e. 19% of USD 1 billion).

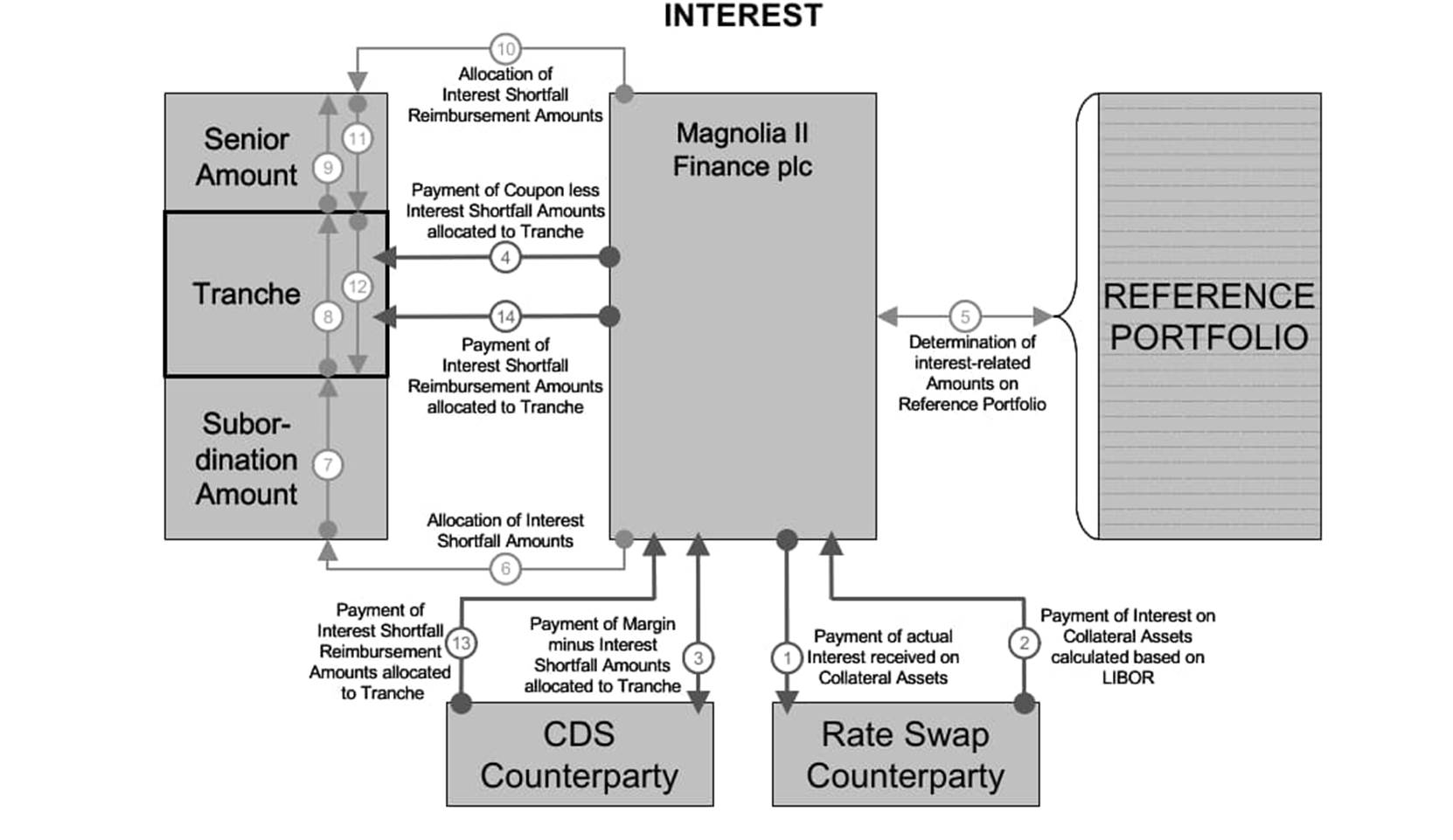

- The CDO's synthetic exposure to the Reference Obligations was created through an embedded CDS (described in the Series Memorandum as the "Credit Swap Transaction"). The parties to that Credit Swap Transaction were Magnolia (for the CDO, effectively as the Protection Seller) and the Fourth Defendant ("CSAG") acting through its Cayman Islands Branch, as the swap counterparty/Protection Buyer. For this reason, the Notes are sometimes referred to as "the Magnolia Notes".

- Under the terms of the Credit Swap Transaction, CSAG (acting through its Cayman Islands Branch) would be obliged to make certain fixed payments to Magnolia and L30 was, in turn, entitled as holder of the Notes to certain payments from Magnolia. In certain circumstances (broadly, those that would amount to a credit event in respect of the Reference Obligations), Magnolia would make payments to CSAG (through its Cayman Islands Branch) to reflect settlement for such credit events in the Reference Portfolio. These processes were complex, and are described in detail in the Series Memorandum but, in essence, if the RMBS performed, L30 would receive the equivalent of interest payments and repayments of principal, while if the RMBS did not perform, then such payments would not be received (or would be received in reduced amounts), and the value of L30's principal investment (described in the Series Memorandum as "Aggregated Outstanding Principal Amount") in the Notes would also fall.

- The structure of the Notes can be summarised in graphic form thus (a diagram to which L30 frequently made reference as highlighting the exposure of L30 to the credit risk of the RMBS):

The CDO Transaction: proposal and discussions

- Prior to the CDO Transaction which forms the basis of these proceedings, IKB and IKB CAM had worked frequently with CS in relation to synthetic CDO transactions. Loreley special purpose vehicles purchased more than 150 CDOs before this transaction.

- Following a meeting with CS employees in December 2006 during which Mr Volker de Haan of IKB CAM expressed interest in investing in further CDO transactions, Mr Bernard Stroobandt (of CSSEL) provided various indicative proposals during the early months of 2007. IKB CAM in turn provided its feedback on these proposals. To give context, the bundle of documents relating to the CDO runs to 991 documents.

- By May 2007, CS had formulated outline terms of a new synthetic CDO to be issued with the involvement of PGI, which would act as manager (if the tranches were to be managed, which was at that stage still to be determined). PGI was also intending to purchase certain junior notes in the proposed CDO for its own account and/or accounts managed by it.

- On 16 May 2007, Mr Stroobandt sent Mr Jörg Zimmermann of IKB CAM an email with an initial proposal for a bespoke synthetic CDO, with the pool either selected by PGI (in static format) or managed by PGI (in managed format). The 16 May email explained that the tranche being offered was:

"USD 105,000,000 Aaa/AAA (Moody's, S&P) tranche. No investment in AA required.

Spread: 1.40% in managed format or at 1.60% in static format

Pool. Min Rating A2"

- Attached to the 16 May email was a term sheet (the "16 May Termsheet") and a spreadsheet with a list of the proposed constituents of the Reference Portfolio entitled "PGI Pool.xls" (the "RMBS Spreadsheet").

- The 16 May Termsheet Stated on its front page that:

i) The proposed CDO would be managed by PGI;

ii) It would have a "Reference Obligation Notional Amount" of US$1 billion;

iii) The issuer would be Magnolia;

iv) The Notes would have an attachment point of 8.5% and a detachment point of 19% (and therefore a principal amount of US$105 million);

v) The initial Reference Portfolio would consist of the 100 RMBS listed in the appendix to the document (92% subprime, 8% Alt-A), all of which were assigned a credit rating of "A2/A or higher"; and

vi) The rating of the Notes would be "Aaa/AAA" ("[s]ubject to change due to continuing data integrity checks related to the characteristics of the Reference Portfolio and pending feedback from the rating agencies").

- It then contained a page entitled "Important Notices" and consisting of various disclaimers (see page 4 of the 16 May Termsheet). This:

i) Set out information about PGI, the proposed portfolio and the proposed Credit Default Swap embedded in the Notes;

ii) Contained, in Section III (entitled "Portfolio Manager"), the subheadings "Disciplined Portfolio Construction" and "Credit Analysis", under the latter of which appeared the bullet point "Fundamental analysis with internal ratings";

iii) Set out in Section VI (entitled "Certain Risk Factors") various risk warnings beneath the statement: "Before making an investment decision, prospective investors in the Notes should consider carefully, in the light of their own financial circumstances and investment objectives, all the information set forth in the Series Memorandum and the final transaction documents, including the risk factors described therein";

iv) Included the following description of "risk factors":

| "Risky Investment: |

Investing in the Notes involves substantial risks and is suitable only for sophisticated investors who have the knowledge and experience in financial and business matters necessary to enable them to evaluate the risks and the merits of an investment in the Notes. The Notes will not be principal protected and investors in the Notes are exposed to full loss of principal. Only prospective investors who can withstand the loss of their entire investment should buy the Notes. |

| [

] |

|

| Asset Backed Securities Market: |

The Reference Obligations will consist of asset backed securities, which are subject to a variety of risks that may adversely affect creditworthiness and/or performance of the Issuer and that could adversely affect demand for the Notes generally. Each prospective investor must make its own independent determination of the value and credit quality of the Reference Obligations. |

| Reference Portfolio Composition and Portfolio Considerations: |

Any illustrative calculations and note breakeven information herein, or in a supplement hereto, is based on a hypothetical profile of the Reference Portfolio constructed on the basis of securities which could be representative of the Reference Portfolio to which the Issuer has exposure. The profile of the final Reference Portfolio is likely to be different, perhaps materially, from that included in the hypothetical profile used for modeling purposes. The Reference Portfolio will generally be made up of mezzanine grade residential mortgage-backed securities. |

| Residential Mortgage- Backed Securities: |

On the Closing Date, the Reference Portfolio will consist predominantly of asset-backed securities that are residential mortgage-backed securities. Residential mortgage-backed securities represent interests in pools of residential mortgage loans secured by one- to four-family residential mortgage loans, including second lien mortgage loans. Residential mortgage loans are obligations of the borrowers thereunder only and are not typically insured or guaranteed by any other person or entity. The rate of defaults and losses on residential mortgage-backed securities will be affected by factors affecting the underlying residential mortgages, including general economic conditions and those in the area where the related mortgaged property is located, the borrower's equity in the mortgaged property and the financial circumstances of the borrower. |

| [

] |

|

| Credit Ratings: |

Credit ratings of debt securities represent the rating agencies' opinions regarding their credit quality and are not a guarantee of quality. Rating agencies attempt to evaluate the safety of principal and interest payments and do not evaluate the risks of fluctuations in market value and, therefore, credit ratings may not fully reflect the true risks of an investment. Also, rating agencies may fail to make timely changes in credit ratings in response to subsequent events, so that an issuer's current financial condition may be better or worse than a rating indicates. Consequently, credit ratings of the reference obligations will be used only as a preliminary indicator of investment quality". |

v) It also explained that the terms set out in the 16 May Termsheet were draft indicative terms which would be superseded by the Series Memorandum, Programme Memorandum and other documentation with respect to the Notes.

- The proposed Reference Portfolio set out in the 16 May Termsheet (and attached in the RMBS Spreadsheet) comprised the same 100 RMBS as ultimately made up the Reference Portfolio for the CDO Transaction (i.e. the Reference Obligations). The Reference Obligations included 7 RMBS in the securitisation of which the Defendants or their affiliates had played some role (i.e. the CS RMBS).

- The RMBS Spreadsheet provided details of 100 Reference Obligations and indicated that each such Reference Obligation carried a Moody's credit rating of A2 or higher and a Standard & Poor's credit rating of A or higher. It also set out information regarding the characteristics of the underlying pools of mortgage loans contained within each of the 100 RMBS, including in relation to: (i) FICO score (a form of credit score), (ii) loan to value ratios ("LTVs"), (iii) occupancy, (iv) property type, and (v) delinquency performance. The first tab of the RMBS Spreadsheet, entitled "Important Notices and Disclaimers", contained inter alia the words:

"Information and opinions presented in this material have been obtained or derived from sources believed by Credit Suisse to be reliable, but Credit Suisse makes no representation as to their accuracy or completeness. Credit Suisse accepts no liability for loss arising from the use of this material. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances".

- On or around 29 May 2007, Mr Zimmermann confirmed that IKB CAM wished to proceed in relation to the "AAA" tranche in the prospective CDO Transaction only. He also said that it preferred a static, rather than managed, format. He asked that the 16 May Termsheet be updated to reflect those changes and to give IKB CAM the right to substitute alternative RMBS for the Reference Obligations, provided that the substitutions did not affect the mark-to-market value of the portfolio. This led to the preparation of a revised termsheet which was sent to Mr Zimmermann by Mr Stroobandt on 30 May 2007 (the "30 May Termsheet"). Amongst other changes, the 30 May Termsheet no longer addressed Series B or C notes (since it was now clear that IKB CAM was not interested in these) and the former Section III ("Portfolio Manager") was replaced with two new sections entitled "Portfolio Selection" and "Noteholders' Removal and Substitution Rights" respectively (as the transaction was no longer to be managed). No change was made to the risk factors and disclaimers quoted above.

IKB CAM's evaluation of the CDO transaction

- Meanwhile, following provision of the proposed Reference Obligations with the 16 May Termsheet, IKB CAM had begun its analysis of the proposed transaction. One of L30's main witnesses, Dr Bauknecht described how this included feeding data provided by CS in relation to the Reference Obligations into the "CDOROM" software provided by Moody's Investors Service Limited ("Moody's"). This software was a risk modelling tool, to evaluate the credit risk of the proposed transaction. One of the purposes of this exercise was to determine the likely impact of raising the attachment point from 8.5% to 9%, which IKB CAM was contemplating. CS also provided IKB CAM with access to its proprietary analytics platform called "Locus", which provided some information as to the characteristics of the underlying pools of mortgage loans for the Reference Obligations, including the distribution of FICO score, LTVs and second liens.

- IKB CAM also requested, and CSSEL provided, various additional information regarding the Reference Obligations. In particular:

i) On or about 16 May 2007, Mr de Haan asked about the proportion of the loans securitised into each Reference Obligation which were secured by a second lien mortgage. Relevant data was provided to him by Mr Stroobandt on 18 May 2007;

ii) On 22 May 2007, Mr Zimmermann asked Mr Stroobandt to provide, for each Reference Obligation, the Moody's rating for its servicer and its current CDS spread. Mr Stroobandt sent him this information on 23 May 2007;

iii) On 29 May 2007, Mr Zimmermann asked Mr Stroobandt to provide "cash flow runs" for the Notes. These were sent to him by Mr Stroobandt on 30 May 2007;

iv) On 31 May 2007, Mr Zimmermann asked Mr Stroobandt to provide "write ups" (i.e. short descriptions of an RMBS) for eight of the Reference Obligations. Mr Stroobandt provided these later that day.

- Mr Zimmermann and his colleague Mr Hubert Langer (who was a credit analyst) then prepared a document entitled "INVESTMENT PROPOSAL for 'Magnolia II CDO' to Rhineland Funding Capital Corp." dated 31 May 2007 (the "Investment Proposal"). The Investment Proposal provided an overview of the proposed transaction and set out the results of IKB CAM's analysis of the Reference Obligations and its evaluation of the CDO structure. The Investment Proposal set out IKB CAM's analysis of the expected losses and loss coverage ratios for all 59 bonds for which CS had provided information and statistical data through its "Locus" platform, which included some but not all of the Twelve CS RMBS.

- Having considered the risks, IKB CAM recommended an investment of US$100 million in the Notes. The recommendation was said to be based on: "the good risk-return-profile for the Class [A] (Aaa/AAA) yielding up to 150bps" and "the underlying portfolio constraints (minimum rating of A2)", i.e. the fact that each of the 100 RMBS in the proposed Reference Portfolio was assigned a credit rating of A2 or higher. A strength of the proposed transaction was identified as: "Rating levels of underlying assets (min. A2/A rating)". Two conditions were identified, namely: "1. Subject to Documentation (Legal Department of IKB CAM). 2. Rating Agency Confirmation for the proposed Ratings on the Notes by Moody's and S&P".

- On 5 June 2007, the proposed investment was presented to IKB CAM's Investment Committee, which comprised Messrs Frank Braunsfeld, Frank Lehrbass and Claus-Dieter Wagner, with Messrs Zimmermann and Langer also present. The IKB CAM Investment Committee decided to recommend that (subject to the same two conditions mentioned above) one of the Rhineland SPCs (which was not at that stage identified) should purchase US$100 million of Notes, as recorded in IKB CAM's Record of Recommendation. The decision was communicated to CSSEL that day by Mr Zimmermann, who informed CS that the purchase had been recommended to a Rhineland SPC.

- On or by 11 June 2007, the recommendation of IKB CAM's Investment Committee was approved by three members of IKB CAM's Advisory Board (Mr Ortseifen, Mr Braunsfeld and Mr Wagner).

Credit Suisse hedging arrangements

- As had been explained in an email from CSSU's Mr Roland Jawurek on 17 May 2007, which was forwarded to Mr Zimmermann on the same day by Mr Martin Rudolph, CSSU stated that it planned to hedge the short exposure to the CDO tranches under the CDS embedded in the CDO.

- On 6 and 7 June 2007 and following IKB CAM's communication of its recommendation in relation to the CDO Transaction, Mr Jean Francois Dreyfus of CS's Correlation Trading (US) desk acting on behalf of CS AG Cayman branch entered into delta hedges with Mr David Higgs' Hedge Trading (EUR/US) desk acting on behalf of CSI in relation to the CDO to reflect the anticipated sale of the Notes.

L30's approval of the purchase of the Notes

- By 11 June 2007, IKB CAM had identified L30 as the appropriate Rhineland SPC to purchase the Notes. On that date, it wrote to L30, Société Générale (which was responsible for administering the Rhineland SPCs), Wilmington Trust SP Services Ltd and RFCC recommending the CDO Transaction, enclosing a copy of IKB CAM's Investment Proposal and Record of Recommendation, and asking that the prospective investment be considered by the TSIC.

- On 11 June 2007, three officers of the TSIC (Messrs Mark Filer, Wolfgang Güth and Andrew Watt) wrote to L30 confirming that they had considered the recommendation and were satisfied that the CDO Transaction: (1) fell within the applicable credit and investment policy; and (2) would be in L30's best interests. This letter stated that any decision to invest "shall solely be a decision of [Loreley 30]".

- On 15 June 2007, short notice was given that a board meeting of L30 would be held to consider and, if deemed fit, approve the CDO Transaction. The meeting, attended by Mr Paul Anderson (as alternate for Mr Alan Dart) and Ms Rebecca Bates (as alternate for Mr Edward Buckland), both professional directors provided by Bedell Cristin Trust Company, took place the same day and entry into the CDO Transaction was approved. According to the minutes of this meeting:

i) The Chairman "tabled a letter plus enclosures dated 11 June 2007

from the Investment Adviser", namely the letter (and enclosures) referred to above;

ii) The Chairman "tabled a Notification of review dated 11 June 2007

from the duly delegated members of the Investment Committee";

iii) The board approved the intended purchase of the Notes, "[a]fter full consideration of" the documents referred to "and noting in particular, (i) the good risk-return profile for the Class A (Aaa/AAA) yielding up to 150 bps [and] (ii) the underlying portfolio constraints (minimum rating of A2)".

The negotiation of the transaction documentation

- On 25 June 2007, CSSU's Mr Fiachra O'Driscoll sent Mr Zimmermann a draft of the Series Memorandum for the CDO Transaction ("the 25 June Draft"). The 25 June Draft was marked as a draft, "Subject to completion dated [

] June 2007 PRELIMINARY SERIES MEMORANDUM" and bore, in red letters, the following warning:

"The information in this preliminary prospectus is not complete and may be changed. This preliminary prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities, nor shall there be any sale of these securities in any jurisdiction where the offer or sale thereof is not permitted, nor has it been approved by the Irish Stock Exchange or the Irish Financial Services Regulatory Authority".

- The 25 June Draft also:

i) Stated on page 2 (square brackets in the original):

"It is expected that, on the relevant Issue Date, each of the Series [3A1] Notes will be rated "Aaa" by Moody's Investors Service Limited or any successor to its credit ratings business ("Moody's") and "AAA" by Standard & Poor's Rating Services, a division of The McGraw-Hill Companies, Inc. or any successor to its credit ratings business ("S&P")".

ii) Stated on page 4:

"Save as provided below, the Issuer [i.e. Magnolia] has taken all reasonable care to ensure that the information contained in this Series Memorandum is true and accurate in all material respects and that in the context of the issue of the Notes, there are no other material facts which would make misleading any statement herein or in the Programme Memorandum.

The Issuer accepts responsibility for the information contained in this Series Memorandum (save for the section entitled "Information Relating to Counterparty") and to the best of the knowledge and belief of the Issuer (which has taken all reasonable care to ensure that such is the case), the information contained in this Series Memorandum is in accordance with the facts and does not omit anything likely to affect the import of such information".

iii) Had a heading "Investor Suitability" on page 18, beneath which it stated:

"

Before making an investment decision, prospective purchasers of, or investors in, any Series of Notes should conduct such independent investigation and analysis regarding the Issuer, such Notes, each of the Reference Obligations (as defined in Appendix A to the section of this Series Memorandum entitled "Credit Swap Transaction" herein), each obligor in relation to the Charged Assets (as defined herein) securing such Notes (including the Investment Provider and the Custodian), the Counterparty under the related Charged Agreements and all other relevant persons and such market and economic factors as they deem appropriate to evaluate the merits and risks of an investment in such Notes. As part of such independent investigation and analysis, prospective purchasers of, or investors in a Series of Notes should consider carefully all the information set out in this Series Memorandum, including the considerations set out below, and the Programme Memorandum.

Investment in a Series of Notes is only suitable for investors who have the knowledge and experience in financial and business matters necessary to enable them to evaluate the information contained in this Series Memorandum and the merits and risks of an investment in such Notes in the context of the investor's own financial, tax and regulatory circumstances and investment objectives".

iv) Contained a section entitled "RISK FACTORS", which started on page 19, and contained a number of statements, some of which are set out below;

v) Under the heading "The Arrangers' and the Counterparty's business activities may create conflicts of interest between them and you" on page 22, stated:

"Certain of the Reference Obligations (including the underlying real estate obligations backing the Reference Obligations) may comprise or consist of obligations of issuers or obligors, or obligations sponsored or serviced by companies, for which the Arrangers, the Counterparty or one of their affiliates have acted as underwriter, agent, placement agent or dealer or for which one of their affiliates has acted as lender or provided other commercial or investment banking services. In addition, the Arrangers, the Counterparty or one of their affiliates may act as Auction Agent (as defined herein) in an Auction (as defined herein). The Arrangers, the Counterparty or one of their affiliates may act as placement agent and/or initial purchaser in other transactions involving issues of collateralised debt obligations or other investment funds with assets similar to those of the Issuer, which may have an adverse effect on the Notes.

[

]

The Counterparty and its affiliates may deal in any obligations or other securities of any Reference Entity (including, but not limited to, any Reference Obligations) or any borrower or issuer of the underlying real estate obligations backing the Reference Obligations (an "Underlying Obligor"), may enter into other credit derivatives involving entities that may include the Reference Entities, Underlying Obligors or their affiliates or sponsors (including credit derivatives to hedge its obligations under a Credit Swap Transaction), may accept deposits from, make loans or otherwise extend credit to, and generally engage in any kind of commercial or investment banking or other business with, any Reference Entity, Underlying Obligor, any affiliate or sponsor of any Reference Entity, Underlying Obligor or any other person or other entity having obligations relating to any Reference Entity, the Underlying Obligor or affiliate or sponsor of such Reference Entity or Underlying Obligor, and may act with respect to such business in the same manner as if such Credit Swap Transaction did not exist, regardless of whether any such relationship or action might have an adverse effect on any Reference Obligation (including, without limitation, any action which might constitute or give rise to a Credit Event), or on the position of the Issuer, the related Noteholders or any other party described herein or otherwise. The Counterparty and its affiliates may, whether by reason of the types of relationships described herein or otherwise, on the date hereof or at any time hereafter, be in possession of information in relation to any Underlying Obligor, Reference Obligation, Reference Entity or any of such Reference Entity's sponsors or affiliates, that is or may be material in the context of the Credit Swap Transactions and the other Transaction Documents and that may or may not be publicly available or known to the other parties to the Transaction Documents and which information the Counterparty or such affiliates may be prohibited from using for the benefit of the Issuer. A Credit Swap Transaction and the other Transaction Documents do not create any obligation on the part of the Counterparty and its affiliates to disclose to any other such party any such information (whether or not confidential)".

vi) Under the heading "You have no rights in the Reference Obligations or any Charged Assets" on page 24, stated:

"

This Series Memorandum is not intended to and does not provide any financial or other information with respect to any Reference Entity or any obligor of any of the Charged Assets or any financial or other risks relating to the business or operations of any Reference Entity or obligor of any of the Charged Assets in general, or to the obligations of any Reference Entity or obligor of any of the Charged Assets in particular.

None of Magnolia, the Arrangers nor any of their respective affiliates assumes any responsibility for the adequacy or accuracy of any information about any Reference Entity or obligor of any of the Charged Assets (including any Investment Provider) contained in any publicly available filings of the Reference Entity or obligors (including any Investment Provider) of any Charged Assets".

vii) Under the heading "No provision of information in relation to the Reference Obligations or any obligor of any Charged Assets" on page 25, stated:

"Other than as explicitly set out in this Series Memorandum and the Programme Memorandum, neither Magnolia nor the Counterparty nor any of their respective affiliates (i) has provided or will provide prospective investors in any Series of Notes with any information or advice with respect to any Reference Obligation, any Charged Assets or their obligor(s) or itself or Investment Provider or the Custodian or (ii) makes any representation as to the credit quality of any Reference Obligation, any Charged Assets or their obligor(s) or itself or any Investment Provider or the Custodian. Further, Magnolia and either of the Arrangers, the Counterparty or any of their respective affiliates may have acquired, or during the term of the Notes may acquire, information (public and non-public) with respect to any Reference Obligation, any Charged Assets or their obligor(s) or itself or any Investment Provider or the Custodian which will not be disclosed to you".

viii) Under the heading "Credit Ratings" on page 28, stated:

"Credit ratings of debt securities represent the rating agencies' opinions regarding their credit quality and are not a guarantee of quality. Rating agencies attempt to evaluate the safety of principal and interest payments and do not evaluate the risks of fluctuations in market value; therefore, credit ratings do not fully reflect the true risks of an investment. Also, rating agencies may fail to make timely changes in credit ratings in response to subsequent events, so that an issuer's current financial condition may be better or worse than a credit rating indicates".

ix) Under the heading "RMBS Securities" on page 29, stated:

"The Reference Obligations will consist of residential mortgage-backed securities ("RMBS Securities") backed by subprime, midprime and prime mortgage loans, which are subject to a variety of risks that may adversely affect creditworthiness and/or performance of the Issuer that in turn could adversely affect demand for the Notes generally. Each prospective investor must make its own independent determination of the value and credit quality of the Reference Obligations".

x) Contained (starting at page 34) a section entitled "TERMS AND CONDITIONS" under which it was stated that "The following are the terms and conditions (the "Conditions") of each Series of Notes in the form in which they will be set out in the Constituting Instrument (as defined below) applicable to such Series of Notes and endorsed on the Notes of such Series in definitive registered form (if any);"

xi) Contained, in Section 1(e) of the Terms and Conditions (on page 39), certain representations which were deemed to have been made and agreed by each purchaser of Notes including:

"(1) it has such knowledge and experience in financial and business matters that it is capable of evaluating the merits, risks and suitability (including for tax, legal, regulatory, accounting and other financial purposes) of its prospective investment in such Notes and/or has consulted with its own legal, regulatory, tax, business, investment, financial and accounting advisers to the extent it has deemed necessary;

(2) it has made its own investment decisions based upon its own judgment and upon any advice from such advisers as it has deemed necessary and has determined that an investment in such Notes is suitable and appropriate for it;

[

]

(4) it is able to bear any loss in connection with such Notes (including loss of the entirety of its original principal investment) and is otherwise capable and willing to assume such risks;

(5) in making such investment it is not relying on the advice or recommendations of or any view expressed by the Issuer or the Arrangers or any of their affiliates (or any representative or agent of any of the foregoing);

(6) it has received and read the Programme Memorandum and this Series Memorandum and/or has been given the opportunity to review all such documentation and all other documentation relating to such Notes (including, without limitation, the documentation comprising the related Charged Agreements, the related Constituting Instrument and all documentation incorporated by reference therein) at the offices of the Arrangers and it understands all such documentation read by it including in particular, but without limitation, the sections of this Series Memorandum headed "Investor Suitability" and "Risk Factors"".

- On 5 July 2007 and 7 July 2007, Mr Thomas Schirmer, an in-house lawyer employed by IKB CAM, provided CS with detailed comments on the drafting of the 25 June Draft.

- On 9 July 2007, Mr Zimmermann informed Mr Stroobandt that the Rhineland SPC which would purchase the Notes would be L30. That same day Mr Jawurek responded to Mr Schirmer setting out CSSU's responses to Mr Schirmer's comments on the 25 June Draft, which included suggestions for changes to that document. Mr Schirmer replied with some further comments on 10 July 2007. These exchanges led CSSU to prepare a further draft of the Series Memorandum, which Mr Jawurek sent to Messrs Schirmer and Zimmermann on 11 July 2007 ("the 11 July Draft"). The 11 July Draft again contained (inter alia) the statements quoted at paragraph 78 above, save that the passage corresponding to that quoted from page 2 of the 25 June Draft omitted the words "It is expected that".

- Some limited changes were made to the 11 July Draft on 12 July 2007 and 13 July 2007 following further discussions between Messrs Jawurek, Schirmer and Zimmermann, including to reflect the fact that Standard & Poor's Rating Services ("S&P") would rate the Notes "AAA/watch negative" on the issue date rather than "AAA".

- On 13 July 2007, Mr Jawurek sent Mr Zimmermann (and others) what his email described as "the final, black Series Memorandum".

- The definitive version of the Series Memorandum, as filed with the Irish Stock Exchange, was dated 25 July 2007.

Interactions with the rating agencies

- Meanwhile, in parallel with its interactions with IKB CAM, CS was in contact with Moody's and S&P in relation to their provision of ratings for the CDO Transaction.

- As far back as 27 April 2007, Mr Yale Chang had individually informed S&P's Mr Christopher Meyer and Moody's Ms Min Xu that what would become the CDO Transaction was expected to proceed. His emails to each were in closely similar form, outlining the capital structure of the proposed CDO Transaction, explaining that the expected closing date was 22 May 2007 and attaching some analysis of the transaction in spreadsheet form. However, the spreadsheet attached to the email to Mr Meyer had been generated using S&P's "CDO Evaluator" software, whilst that attached to the email to Ms Xu made use of Moody's equivalent, CDOROM.

- Ms Xu quickly responded, requesting the CUSIPs (unique identifying numbers assigned to securities) for the Reference Obligations. These were provided by Mr Chang the same day.

- Having analysed the portfolio, Mr Meyer provided S&P's preliminary feedback on the Reference Obligations on 1 May 2007 in the form of five spreadsheets. In later exchanges on 11 June 2007, Mr Meyer confirmed that the results had not changed because there had been no "rating migration" affecting the Reference Obligations since early May.

- The next material interaction with the rating agencies took place at the time of the 25 June Draft, when Mr Meyer and Ms Xu provided input into the drafting of the Series Memorandum. In particular, on 25 June 2007 Mr Meyer asked that a notice of any "Adjustment" (as defined) should be required to be sent to a specified S&P email address, whilst Ms Xu provided various comments on rating-related aspects of the drafting. These comments were reflected in the 11 July Draft. Ms Xu then provided further drafting comments on the 11 July Draft on 12 July 2007, which were again reflected in subsequent versions of the Series Memorandum.

Final ratings and L30's purchase of the Notes

- On 12 July 2007, Moody's provided a signed rating letter to be held in escrow whilst S&P sent CS a draft rating letter for the CDO Transaction.

- The CDO Transaction was entered into during a telephone call between Mr Jawurek and Ms Inna Ivanova of Société Générale, which took place at approximately 2pm UTC on 12 July 2007, with a settlement date of 13 July 2007. A written confirmation of the trade was faxed to IKB and L30 at 3.02pm on 12 July 2007. As reflected in the trade confirmation, L30 purchased the Notes from CSSU, which acted through its agent, CSSEL.

- Finally, on 13 July 2007:

i) The board of Magnolia (Mr Michael Whelan and Ms Jennifer Coyne, professional directors supplied by Deutsche International Corporate Services (Ireland) Limited as the administrator of Magnolia) voted to approve the issuance of the Notes, with an issue date of 13 July 2007. The minutes of this meeting record inter alia that the board of Magnolia accepted a proposal from CSI to issue the Notes, that the board of Magnolia had thereby approved on behalf of Magnolia the documents presented to them including the Series Memorandum, and that CSI was "authorised to distribute copies of the Programme Memorandum relating to the Programme and Series Memorandum and to offer the Notes for sale on behalf of the Company in accordance with the terms thereof";

ii) Moody's released its letter assigning the Notes a rating of "Aaa";

iii) S&P issued a finalised rating letter which gave the Notes a rating of "AAA/Watch Neg"; and

iv) The transaction documents were executed, the Notes being issued to CSSU and then transferred to L30 pursuant to the trade confirmation.

- In light of S&P's decision to impose the "watch negative" on its rating, Mr Jawurek agreed with Mr Zimmermann immediately prior to closing that the attachment point of the Notes would be increased if, following S&P's review, that action was necessary to raise the S&P credit rating to "AAA". However, S&P's review resulted in the removal of the "watch negative" and the affirmation of its "AAA" rating on 24 July 2007 without the need for any such step.

The rescue of the Rhineland Programme by KfW

- From 27 to 29 July 2007, less than a fortnight after the conclusion of the CDO Transaction, IKB experienced what it later described as a "crisis weekend". There were doubts about IKB's liquidity situation and, to stabilise the situation, the German public sector banking institution Kreditanstalt für Wiederaufbau ("KfW") assumed (inter alia) IKB's liquidity commitments to the Rhineland Programme, amounting to 8.1 billion. Four of IKB's board members left the bank as a consequence of this crisis. PricewaterhouseCoopers was instructed to undertake a special review of IKB's business and made findings critical inter alia of the Rhineland Programme's risk management, portfolio monitoring and excessive concentration on subprime investments.

- As a result of the rescue and its assumption of IKB's obligations, KfW became a liquidity facility provider to the Rhineland SPCs, including L30, and their largest creditor.

- Following a subsequent restructuring of the Rhineland Programme in 2012, KfW became the sole liquidity provider and sole substantial creditor to the Rhineland SPCs.

The performance and redemption of the Notes

- According to notices issued to the Noteholders by Magnolia, between about the beginning of October 2008 and the end of April 2009 CSAG delivered to Magnolia a series of Floating Amount ("Writedown") Notices relating to (inter alia) certain of the Reference Obligations.

- Between L30's purchase of the Notes and 28 April 2010, certain Writedowns (i.e. realised losses in view of the non-performance of the Reference Obligations, as defined in page 144 of the Series Memorandum dated 25 July 2007) occurred in respect of Reference Obligations. These resulted in the triggering of CDS credit events. Consequently, Magnolia, as Protection Seller, was obliged to make payments to CSAG (through its Cayman Islands Branch) as Protection Buyer, with the result that the Aggregated Outstanding Principal Amount of the Notes held by L30 was reduced. As a result of the performance failures amongst the 100 Reference Obligations, that Aggregated Outstanding Principal Amount reached zero in March 2009, at which point the original USD 100 million principal value had been paid to CSAG under the CDS.

- By the end of April 2009, therefore the "Aggregate Outstanding Principal Amount" of the Notes (as defined in Condition 7(d) of the Notes) had been reduced to zero, at which it remained thereafter. On 26 April 2010, CSAG delivered to Magnolia a Notice of Redemption, notifying it that the Notes had been redeemed without payment. The Notes were delisted from the Irish Stock Exchange with effect from 28 April 2010, as it was a mandatory redemption condition of the Notes that they would be redeemed without payment in these circumstances (see Condition 7(b)(4) of the Notes in the Series Memorandum).

- In 2008, KfW put in place a press monitoring and/or alert system "to capture information on developments relating to the financial crisis". As will be explained further below, from 2008 onwards it also instructed both UK and US lawyers to, as Mr Bulgrin put it, "provide advice on potential legal avenues in both jurisdictions including what potential claims may be available at a general level in connection with SPC assets", and later to provide updates on litigation relating to the financial crisis.

The US Department of Justice Settlement

- From about 2009 the US Department of Justice ("DoJ") began to take an interest in deals involving RMBS, setting up an RMBS Working Group. In due course the investigations encompassed CS.

- In January 2017 the DoJ announced a $5.28 billion settlement with CS, related to CS's conduct in the packaging, securitization, issuance, marketing and sale of RMBS between 2005 and 2007.

- That settlement and the press release which accompanied it ("the 2017 Press Release"), formed an important plank of L30's case. It might indeed be said to be a foundational document for L30, with its case in closing starting with another detailed look at the document. L30 says that the Statement of Facts ("SoF") which accompanied the settlement contains admissions of fraud. It takes the DoJ Settlement and those alleged admissions as its starting point. It says that "CS' protestations of innocence ring hollow in light of that settlement.". The contents of those documents are therefore of some moment.

- The 2017 Press Release, dated 18 January 2017, said this:

"Credit Suisse Agrees to Pay $5.28 Billion in Connection with its Sale of Residential Mortgage-Backed Securities

The Justice Department announced today a $5.28 billion settlement with CS related to CS's conduct in the packaging, securitization, issuance, marketing and sale of residential mortgage-backed securities ("RMBS") between 2005 and 2007. The resolution announced today requires CS to pay $2.48 billion as a civil penalty under the Financial Institutions Reform, Recovery and Enforcement Act ("FIRREA").

Today's settlement underscores that the Department of Justice will hold accountable the institutions responsible for the financial crisis of 2008" said Attorney General Loretta E Lynch. "Credit Suisse made false and irresponsible representations about residential mortgage-backed securities, which resulted in the loss of billions of dollars of wealth and took a painful toll on the lives of ordinary Americans.

Credit Suisse claimed its mortgaged backed securities were sound, but in the settlement announced today the bank concedes that it knew it was peddling investments containing loans that were unlikely to fail" said Principal Deputy Associate Attorney General Bill Baer. "That behavior is unacceptable. Today's $5.3 billion resolution is another step towards holding financial institutions accountable for misleading investors and the American public.

This settlement includes a statement of facts which CS has agreed. That statement of facts describes how CS made false and misleading representations to prospective investors about the characteristics of the mortgage loans it securitized".

- The SoF accompanying the announcement, agreed by CS, contains the following passages[2]:

"[1] From May 2005 through 2007, Credit Suisse Securities (USA) LLC, itself and through certain of its U.S affiliates (collectively "Credit Suisse", securitized hundreds of thousands of residential mortgage loans into residential mortgage-backed securities ("RMBS"). It sold these RMBS for tens of billions of dollars to investors. In marketing and selling its RMBS, Credit Suisse made numerous representations about the quality and characteristics of the underlying loans. These representations were made to RMBS investors and potential investors, ratings agencies and others. As described below, in the diligence process, Credit Suisse repeatedly received information indicating that many of the loans reviewed did not conform to the representation that would be made by Credit Suisse to investors about the loans to be securitized.

II. Credit Suisse's Representation to Investors

[4] In connection with its RMBS offerings on principal transactions, Credit Suisse made representations about the loans it securitized. Those representations often varied from securitization to securitization. Credit Suisse made representations that, among other things:

1. The loans were originated generally in accordance with applicable underwriting guidelines, with exceptions to those guidelines being made when sufficient compensating factors were demonstrated by a prospective borrower.

2. For each loan, a determination had been made by the originator that the borrower had the ability to repay the monthly obligations on the loan and other debts.

3. Beginning in early 2006, Credit Suisse modified its representation in certain offering documents to state that each Correspondent loan was "in fact" originated in accordance with Credit Suisse's underwriting guidelines or guidelines that did not vary materially from such guidelines and that Credit Suisse "employed

certain quality assurance procedures designed" to ensure that such loans were originated in accordance with the underwriting guidelines.

4. Each loan had been originated in compliance with all federal, state and local laws and regulations, including all predatory and abusive lending laws.

5. For each loan, the adequacy of the mortgaged property as security for repayment generally had been determined by an appraisal in accordance with pre-established appraisal procedure guidelines for appraisals established by or acceptable by the originator.

6. The loans had various characteristics, including certain loan-to-value (LTV) ratios disclosed to the trustee in Mortgage Loan Schedules for each loan. The distribution of these LTVs in five-to-ten percent bands was also included in prospectus supplements. Other characteristics, such as borrower FICO scores, were disclosed as well. Credit Suisse represented to the trustee that these characteristics about the loans were complete, true and correct for the loans as of the cut-off date for the securitization.

7. None of the loans had a loan-to value ratio or, with respect to second lien mortgages, a combined loan-to-value ratio, in excess of 100 (i.e., none of the loans were "underwater").

8. Credit Suisse 'will not include any mortgage loan in [the RMBS] if anything had come to [its] attention that would cause it to believe that the representations and warranties of a seller will not be accurate and complete in all material respects in respect of the related mortgage loan'.

[5] Credit Suisse also represented that if it later learned that any loan RMBS breached its representations in a material respect, it would cure the breach or repurchase or substitute that loan from the RMBS.

[6] In various marketing materials, Credit Suisse made additional representations about the loans it securitized into RMBS, and its process for reviewing loans before it selected them to securitization. In these marketing materials, Credit Suisse told investors and others, among other things:

1. Credit Suisse conducted a 'rigorous due diligence process' for reviewing loans;

2. All final loan decisions were made by Credit Suisse senior underwriters, not third-party contractors.

3. Credit Suisse conducted 'quality control' reviews on its loans after purchasing or originating them.

[7] As Credit Suisse employees discussed internally, Credit Suisse made these representations in order to 'convince investors and insurers that [its] disciplined approach to underwriting [its] multi-layered origination process, and an eligibility matrix that utilize[d] a more layered risk of performance will result in an acceptable level of delinquencies for [its] products'.

III Credit Suisse's RMBS Business

[8]

The senior traders reported that a number of the loans had gone delinquent or into foreclosure within a few months after Credit Suisse sold the RMBS to investors. The Co-Head of the Structured Products Group responded, 'of course we would like higher quality loans. That's never been the identity of our conduit, and we're becoming less and less competitive in that space". Around the same time, one of the senior traders described his situation in a Bloomberg message: "I figure I could just capitulate

and keep buying all [these] crappy loans, but that would be suicide. And we still have almost $2.5B of conduit garbage to still distribute.

[9] In October 2005, Credit Suisse's Head of Credit and Underwriting wrote to two senior Credit Suisse traders and others, 'we are selling and securitizing loans with missing docs all the time through the other desks' (Missing documents included borrower credit reports, verifications of borrower income and assets, property appraisals and legal compliance documents such as HUD-1 statements and Truth in Lending Act disclosures.) The Head of Credit and Underwriting continued: 'it only becomes an issue when we are asked to repurchase the loan or we receive a complaint from a customer'.