DECISION

Introduction

1. The form of the hearing was V (video) via the Tribunal video hearing system. A face to face hearing was not held because a remote hearing was appropriate.

2. The documents to which we were referred are a document bundle of 177 pages and a generic bundle of 808 pages.

3. Prior notice of the hearing had been published on the gov.uk website, with information about how representatives of the media or members of the public could apply to join the hearing remotely in order to observe the proceedings. As such, the hearing was held in public.

matters under appeal

4. When Mrs O'Hare brought her appeal, she was appealing against both failure to notify penalties and discovery assessments relating to a failure to pay the higher income child benefit charge (HICBC) for five tax years from 2015/16 to 2019/20.

5. Prior to the hearing, HMRC conducted a review that led to a change of position, namely an acceptance that Mrs O'Hare had a reasonable excuse for her failure to notify. The result of this conclusion was that HMRC now accepted that no penalties arose and the first two years of assessment, which had relied on extended time limits, were now out of time.

6. As a result, HMRC invited the Tribunal to allow the appeals against those matters.

7. We announced at the hearing our decision that these appeals would be allowed and record that here. The following appeals are allowed:

(1) Failure to notify penalties of £572.30 in respect of the years 2015/16 to 2019/20; and

(2) Discovery assessments of £54 for the tax year 2015/16 and £232 for the tax year 2016/17.

8. The appeals that remain, and which are the subject of the remainder of this decision are:

(1) Discovery assessment of £608 for 2017/18;

(2) Discovery assessment of £1,091 for 2018/19;

(3) Discovery assessment of £1,753 for 2019/20;

These add up to £3,452.

facts

9. The core facts for this appeal were not disputed and are recorded below. Other factual issues were in dispute and are recorded later in the decision:

(1) Mrs O'Hare claimed child benefit in the relevant years;

(2) Her adjusted net income exceeded the HICBC threshold and that of her spouse for the relevant years;

(3) She was not issued with a notice to file a self-assessment return and did not make one;

(4) She did not make a notification of liability to HICBC in relation to these years;

(5) She received a letter from HMRC dated 20 April 2021 highlighting her potential liability to HICBC;

(6) She called HMRC to discuss the matter on 28 April 2021;

(7) Discovery assessments were issued on 11 May 2021;

(8) Mrs O'Hare sent a letter of appeal to HMRC on 23 May 2021;

(9) HMRC issued a view of the matter letter on 19 May 2022, upholding the assessments;

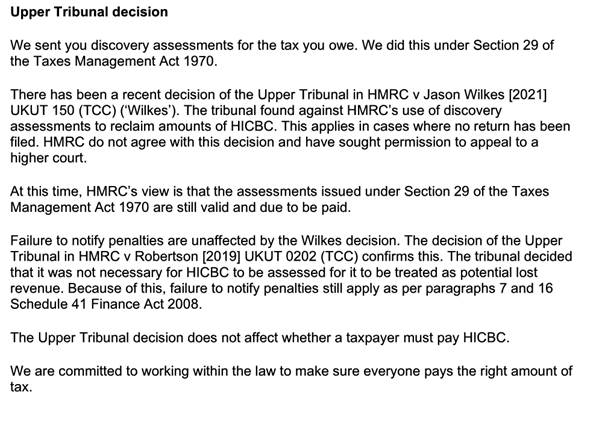

(10) HMRC issued a review conclusion letter on 27 June 2022, again upholding the assessments;

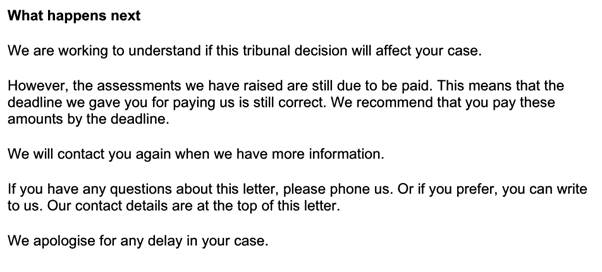

(11) Mrs O'Hare appealed using a form relating to appeals regarding child benefit on 19 July 2022, but to the social entitlement chamber; and

(12) HMRC applied to transfer the appeal to the tax chamber, which it duly was.

law

10. The HICBC came into effect on 7 January 2013 and arises under section 681B of the Income Tax (Earnings and Pensions) Act 2003 ("ITEPA 2003").

11. The HICBC imposes a charge to tax equal to the child benefit received for those individuals who have adjusted net income of over £60,000 in the tax year. The tax charge is reduced proportionally where adjusted net income ("ANI " ) is between £50,000 and £60,000, but the way in which this applies is not in dispute in this case. ANI is defined in ITEPA 2003, s 681H.

12. Until the Finance Act 2022 ('FA 2022') came into force on 24 February 2022, section 29(1)(a) TMA 1970 provided, as far as relevant to this appeal, that:

"29(1) If an officer of the Board or the Board discover, as regards any person (the taxpayer) and a year of assessment—

(a) that any income which ought to have been assessed to income tax, or chargeable gains which ought to have been assessed to capital gains tax, have not been assessed, or

...

the officer or, as the case may be, the Board may, subject to subsections (2) and (3) below, make an assessment in the amount, or the further amount, which ought in his or their opinion to be charged in order to make good to the Crown the loss of tax."

13. Subsections (2) and (3) of section 29 TMA only apply where the taxpayer has made and delivered a return and cannot apply in this case as Mrs O'Hare did not make a Self Assessment Tax Return in the years assessed.

14. In relation to assessments under section 29 TMA to collect the HICBC, a series of decisions relating to an appeal brought by Mr Jason Wilkes (ultimately confirmed by the Court of Appeal in HMRC v Wilkes [2022] EWCA Civ 1612 ('Wilkes CA')) held that the HICBC was "neither 'income' nor even charged on income" nor was it "income which ought to have been assessed to income tax" or an "amount which ought to have been assessed to income tax" (see Wilkes CA at [29]). Accordingly, the HICBC could not be assessed under section 29(1)(a) TMA.

15. Section 29 TMA 1970 was amended by the Finance Act 2022 ('FA 2022'). Section 97 amended section 29(1)(a) to read "that an amount of income tax or capital gains tax ought to have been assessed but has not been assessed". The change in wording introduced by section 97 FA 2022 reversed the decisions in the Wilkes cases and allowed HMRC to make discovery assessments, subject to the usual conditions, in relation to the HICBC and some other things.

16. This new wording had retrospective effect to tax year 2020-21 and before, but only if the assessments were "protected assessments". The relevant provisions in section 97 are as follows:

"(3) The amendments made by this section—

(a) have effect in relation to the tax year 2021-22 and subsequent tax years, and

(b) also have effect in relation to the tax year 2020-21 and earlier tax years but only if the discovery assessment is a relevant protected assessment (see subsections (4) to (6)).

(4) A discovery assessment is a relevant protected assessment if it is in respect of an amount of tax chargeable under—

(a) Chapter 8 of Part 10 of ITEPA 2003 (high income child benefit charge),

...

(5) But a discovery assessment is not a relevant protected assessment if it is subject to an appeal notice of which was given to HMRC on or before 30 June 2021 where—

(a) an issue in the appeal is that the assessment is invalid as a result of its not relating to the discovery of income which ought to have been assessed to income tax but which had not been so assessed, and

(b) the issue was raised on or before 30 June 2021 (whether by the appellant or in a decision given by the tribunal).

(6) In addition, a discovery assessment is not a relevant protected assessment if—

(a) it is subject to an appeal notice of which was given to HMRC on or before 30 June 2021,

(b) the appeal is subject to a temporary pause which occurred before 27 October 2021, and

(c) it is reasonable to conclude that the temporary pausing of the appeal occurred (wholly or partly) on the basis that an issue of a kind mentioned in subsection (5)(a) is, or might be, relevant to the determination of the appeal.

(7) For the purposes of this section the cases where notice of an appeal was given to HMRC on or before 30 June 2021 include a case where—

(a) notice of an appeal is given after that date as a result of section 49 of TMA 1970, but

(b) a request in writing was made to HMRC on or before that date seeking HMRC's agreement to the notice being given after the relevant time limit (within the meaning of that section).

(8) For the purposes of this section an appeal is subject to a temporary pause which occurred before 27 October 2021 if—

(a) the appeal has been stayed by the tribunal before that date,

(b) the parties to the appeal have agreed before that date to stay the appeal, or

(c) HMRC have notified the appellant ("A") before that date that they are suspending work on the appeal pending the determination of another appeal the details of which have been notified to A."

17. In broad terms, the retrospective changes made by section 97 FA 2022 do not apply to an appeal that was made to HMRC on or before 30 June 2021 in one of two circumstances:

(1) The appeal concerned the issue identified in the decisions in the Wilkes cases and that issue was raised by a party or the FTT before that date, or

(2) The appeal was subject to a temporary pause on or before 27 October 2021 because of that issue.

18. The ability of HMRC to raise assessments under section 29 TMA is also subject to time limits. For the purposes of this appeal, the relevant time limit is set out in section 34 as follows:

"34(1) Subject to the following provisions of this Act, and to any other provisions of the Taxes Acts allowing a longer period in any particular class of case, an assessment to income tax or capital gains tax may be made at any time not more than 4 years after the end of the year of assessment to which it relates.

34(2) An objection to the making of any assessment on the ground that the time limit for making it has expired shall only be made on an appeal against the assessment.

..."

Parties arguments

Appellant's contentions

19. The appellant contended that the assessments should be removed because:

(1) She claimed child benefit for her children at a time that HICBC did not exist and neither her, nor her spouse, were higher earners at the time the children were born;

(2) The first she heard about HICBC was the letter received in 2021, which she found quite frightening to receive. Although she is a regular watcher of the news, she had been completely unaware of the HICBC and did not see any media coverage;

(3) She immediately called HMRC and dealt with a helpful person who explained it all to her on a long phone call;

(4) The process has taken over 3 years from the first letter from HMRC and has been very stressful;

(5) She is aware of self-assessment because her father was self-employed, but had no idea that receiving a government benefit could push her into needing to file a return when her only other income was dealt with via PAYE;

(6) It is not fair that HMRC have left it so long to contact relevant people, because this has led to a build up of HICBC and interest that increases her liability. She feels that HMRC must have known there was a problem of people not realising they were subject to it, but did nothing about it, despite having all the relevant information. She was given no chance to put it right until there was a lot of money at stake;

(7) Since this all started, she has spoken to a number of other people, all of whom have had the same experience as her - they didn't know about it until HMRC got in touch years later;

(8) She did not receive any letters in 2019, when HMRC claims they sent a letter. She responds to all correspondence from HMRC, which she has had periodically. Her response when she received the 2021 letter was within a week;

(9) While she also did not receive the letter dated 9 September 2021 which HMRC claimed to have sent, she did call HMRC on 29 October 2021 and the adviser read the letter out to her and she interpreted that as a pause on her case - that she needed to wait for HMRC and that they would contact her again.

20. HMRC submits that:

(1) The discovery assessments were valid because the HMRC officer established that:

(a) the Appellant had received payment of Child Benefit in the tax years now under appeal,

(b) the adjusted net income of the Appellant exceeded £50,000 in those years (and was higher than her spouse or partner's income),

(c) the Appellant had not completed a self-assessment tax return declaring the HICBC for the years under appeal.

(2) Having discovered these matters, the officer identified that an amount that ought to have been chargeable to income tax had not been so charged. This discovery of a loss of tax was notified to the Appellant on 20 April 2021;

(3) HMRC has met the conditions for a valid discovery assessment on the basis of a reasonable belief in an insufficiency of tax;

(4) While the appeal was made before the 30 June 2021 cut off date, HMRC contend that there has been no temporary pause of Mrs O'Hare's case and therefore HMRC's discovery assessments are protected;

(5) The letter sent by HMRC on 9 September 2021 cannot be construed as representing a temporary pause because the conditions in section 97(8) are not met, in particular the letter did not indicate that HMRC were suspending work pending the determination of another appeal, because it stated that HMRC are working to understand the impact of the appeal; and

(6) There are no other reasons for the assessment to be reduced on appeal;

Discussion

21. Mrs O'Hare did not dispute that, based on her new understanding of the HICBC rules, she should have notified her liability to the HICBC charge, but she did not. She also did not challenge the calculation of the amounts.

22. However, we need to consider whether the discovery assessment was valid in accordance with the provision, as amended on a retrospective basis.

23. Since Mrs O'Hare's appeal was submitted before the 30 June 2021, HMRC may only raise a discovery assessment on the basis of failing to notify liability to HICBC if it is a protected assessment. Neither party sought to assert that the assessments were protected under section 97(5) of FA 2022.

24. In this case, the key question is whether the appeal was subject to a temporary pause in accordance with sub-sections 97(6) and (8) of FA 2022.

25. A temporary pause has to have been in place by 27 October 2021 and is defined in section 97(8). There are three possible ways in which a temporary pause can be found:

(1) The appeal has been stayed by the tribunal by that date;

(2) The parties have agreed to stay the appeal by that date; or

(3) HMRC had notified the Appellant ("A") before that date that they are suspending work on the appeal pending the determination of another appeal, the details of which have been notified to A.

26. Neither party suggested to us that the appeal had been stayed by the Tribunal or by agreement between them. However, Mrs O'Hare argues that the third type of temporary pause applied to her, by virtue of the letter of 9 September 2021 which she did not receive, but was read to her over the phone by an HMRC officer.

27. As a matter of fact, we find that HMRC did issue the 9 September 2021 letter, but that Mrs O'Hare did not receive it. Since the contents of the letter were communicated to her over the telephone, we have considered its contents. However, given the outcome below, we do not need to consider whether such a set of factual circumstances could have amounted to a "notification" within the relevant timeframe and therefore do not express an opinion on it.

28. In order to assess whether a temporary pause was established, we need to consider the exact wording of that letter. The heading of the letter is "Further information about your High Income Child Benefit Charge case". The letter thanks Mrs O'Hare for her May letter and then records details of recent decisions as follows:

29. It then goes on under a heading of "What happens next":

30. We also had notes from a telephone call that Mrs O'Hare made to HMRC. The call handler records in their notes that they "explained what the holding letter says with regards to the status of her case, the recent Tribunal decision, and that we will contact her if her case is affected by the Tribunal outcome." The notes go on to record that the call handler was "advised to not resend the Holding letter due to the current pause". Mrs O'Hare confirmed at the hearing that this was not explained to her on the call.

31. We need to decide whether the letter and/or the phone call amounts to HMRC notifying Mrs O'Hare that they are "suspending work" on her appeal "pending the determination of another appeal".

32. We do not consider that they do. The wording under "what happens next" in fact states, in fairly explicit terms, that HMRC are still working on Mrs O'Hare's appeal to decide whether or not the decision in Wilkes is relevant to her appeal. We do not consider that this can amount to a suspension of work pending the determination of Wilkes because HMRC had not yet decided whether or not the determination in Wilkes would be relevant to her appeal. The reader of that letter could not reasonably have concluded that no further work was continuing.

33. On that basis, we consider that the assessments were "protected assessments" and therefore the retrospective effect of the changes to section 29 applied to the assessments raised on Mrs O'Hare.

34. We also find that the HMRC officer made a discovery of an insufficiency of tax under section 29 and that the belief of that officer was a reasonable one. Therefore the assessments were validly raised.

35. With regards to Mrs O'Hare's submissions on the fairness of the charge, the assessments and the time it took HMRC to contact her, we note that none of these arguments are matters that can displace or alter the assessments as raised. The time limits for raising the assessments are set out in statute and have been met with regards the matters under appeal.

36. For the reasons given above, we dismiss the appeals and the assessments stand good.

Right to apply for permission to appeal

37. This document contains full findings of fact and reasons for the decision. Any party dissatisfied with this decision has a right to apply for permission to appeal against it pursuant to Rule 39 of the Tribunal Procedure (First-tier Tribunal) (Tax Chamber) Rules 2009. The application must be received by this Tribunal not later than 56 days after this decision is sent to that party. The parties are referred to "Guidance to accompany a Decision from the First-tier Tribunal (Tax Chamber)" which accompanies and forms part of this decision notice.

ABIGAIL MCGREGOR

TRIBUNAL JUDGE

Release date: 16th OCTOBER 2024