“A. Yes, I need to correct him, because it was in - when I made the statement like nine months ago that was the assets. Today, if I would make a similar statement, it would be between 600 and 800 million.

MR JUSTICE MOSTYN: Really. Your total net worth.

A. Yes, and I can give the –

MR JUSTICE MOSTYN: Between 600 and 800 million.

MR CUSWORTH: As of now, you have lost in the last nine months about $1 billion worth of assets?

A. Yes.

MR JUSTICE MOSTYN: Okay.

A. Yes, I can explain if it's necessary.

MR JUSTICE MOSTYN: No, I am just processing that, okay.

MR CUSWORTH: You have never asserted or relied on that fact before today, have you? There has been no updated evidence from you about the state of your assets.

A. It is not important.”

- The husband’s evidence is not that surprising. The schedule summarising his investment property portfolio, disclosed on 25 June 2021, identifies numerous commercial properties, mainly in New York. These properties are all co-owned, in varying shares, with other investors. The properties are said to be worth $10.17 billion with mortgages of $6.65 billion. The properties are thus all highly leveraged. The overall debt-to-assets ratio is 65%. The equity is $3.52 billion of which the husband’s share is $1.47 billion (41.8%).

- It would not take much movement downwards from the top figure for the husband’s share of the equity to fall to $700 million. Mathematically, a reduction of the $10.17 billion figure by 18.1% to $8.33 billion results in a halving of the value of the husband’s share of the equity. It seems to me plausible that the blows to the global economy since June 2021 could have resulted in such a reduction in the value of the property portfolio. But as the husband rightly says, it is not important. The result of this case does not differ depending on whether the husband is worth $700 million or $1 billion or $1.7 billion.

- The parties certainly lived a billionaire lifestyle during their marriage. The nature of the parties’ relationship was such that money (and particularly the detail of family expenditure) was never a concern. I described their lifestyle in my maintenance pending suit judgment. At [12] I stated:

“It is common ground that during the marriage the parties enjoyed an extremely high standard of living. They had the use of properties around the world (including a property located in the heart of the Cap d’Antibes, to which I will return later in this judgment). The parties employed a significant number of staff at the West London property, as I have described above, and in their other properties. It is agreed that the parties would spend a great deal of time travelling, typically by private plane or first-class commercial flights, and staying in high-end hotels or villas at significant cost.”

- They ran at least five fully staffed homes in fashionable places such as The Hamptons, New York City, Paris, Miami, Cap d’Antibes, Capri and London.

- The wife and the children have their primary residence at the family home in West London, and when in London the husband lives in an apartment near the family home. The family home is over 8,500 square feet in area. Its agreed value is £35,000,000 and the mortgage is £21,500,000. It is a property of exceptional amenity, but with extraordinarily high running costs. It has six stories, five bedrooms, and an indoor heated pool in its basement. It has a private garden and access to a communal garden. The parties had a retinue of staff at the family home. They formally employed two rota chefs, a house manager, two or three housekeepers, a laundress and two full-time nannies, in addition to a multitude of contractors (gardeners, pool maintainers, builders, plumbers, electricians and handymen).

- In the maintenance pending suit judgment, I described and analysed the annual expenditure. According to a schedule produced by the husband on 25 June 2021, in 2019, the last calendar year of the marriage, the expenditure was £4.78 million. Mr Cusworth KC submits that an analysis subsequently made of the American Express statements shows that this figure is understated. Be that as it may, the rate at which the family lived was phenomenally high. This is not a common-or-garden big-money case; this is a case of the super-rich who, as I stated in my previous judgment (quoting F Scott Fitzgerald), are truly different to you and me.

- This family’s custom of unrestrained expenditure has been practised in the litigation. Prodigious amounts of legal costs have been incurred. The parties’ Forms H filed at the start of the trial show a combined expenditure on these financial remedy proceedings of £4,314,769, broken down as follows:

|

Wife |

Husband |

|

Counsel |

482,148 |

562,700 |

|

Disbursements |

110,374 |

119,786 |

|

Solicitors |

1,593,275 |

1,446,486 |

|

Total |

2,185,797 |

2,128,972 |

Since the date of her Form H (29 September 2022) the wife has incurred a further £317,382 in financial remedy costs, giving a final total for her of £2,503,179.

- I gather that the parties have spent much the same in the Children Act proceedings. To spend over £8 million in family litigation in such a short period must be almost a record. The scale and intensity of the financial dispute between the parties, and the amounts spent on it, demonstrate the enduring vigour of the law of unintended consequences. The intended consequence of the modified PNA was to spell out with clarity the financial outcome in the event of divorce, and in so doing to prevent, or at least seriously circumscribe, any future litigation. In fact, the exact opposite has happened. The parties have furiously and expensively litigated, probably more intensely and extensively than would have occurred in a routine financial remedy case without a PNA.

The PNA

- The parties executed the PNA in accordance with the law of the State of New York on 2 March 2012, some six weeks before the marriage. As stated above, the husband’s net worth was disclosed in the sum of $1,018,215,671. The wife’s net worth was stated to be $4,471,500. Both parties had advice from, and were represented by, distinguished lawyers and there has been no suggestion of deficiency or pressure within the process leading up to the execution of the PNA.

- The parties signed a subsequent Modification Agreement on 23 March 2014. In her evidence, the wife described how this was presented to her in completed form as a birthday present. It increased the financial provision to be made to the wife pursuant to the PNA. As with the PNA, there has been no suggestion that the process leading to its execution was in any way flawed.

- The PNA creates a regime of separate property and includes a waiver of spousal maintenance claims in consideration of the provision made in the agreements. The key features of the agreements are as follows:

a. The preamble to the PNA states that it is intended to be in full satisfaction of all the parties’ rights arising out of the marriage or its dissolution except with respect to issues relating to custody and child support of any children of the marriage. To reinforce their mutual intention, the PNA concludes by stating in Article 17, in uppercase and in bold type:

“EACH PARTY TO THIS AGREEMENT FULLY UNDERSTANDS AND AGREES THAT HE OR SHE IS RELINQUISHING VALUABLE PROPERTY RIGHTS BY SIGNING THIS AGREEMENT.”

b. The parties acknowledged that they had received independent legal advice and that each had made clear and comprehensible financial disclosure (Article 2 and Exhibits A and B).

c. Separate property is defined in Article 3 and any claims in respect of such property is waived in Article 4.

d. The right to claim maintenance or alimony is waived in Article 5.

e. Article 6 establishes the rights that arise on an Event of Marital Dissolution, which is defined, for the intents of the case before me, in Article 11 as the commencement of divorce proceedings by either party. That occurred on 22 December 2020, and so for the purposes of the PNA this was a marriage of 8¾ years (to be exact, 103 months). An important provision is article 6.2.1 which permits the wife, in the event of the breakdown of the marriage, to remain in the primary residence of the parties until the youngest child of the marriage attains 21 years of age, with the husband discharging the mortgage repayments, and paying for major repairs and the household staff, with the wife bearing all other expenses of the property.

f. The terms of Article 6 are of central relevance to the dispute that I have to resolve and will be addressed in detail later in this judgment.

g. Article 13 provides that on the occurrence of an Event of Marital Dissolution, the husband shall pay the wife’s legal fees necessary to resolve all issues between the parties, including issues relating to child custody, access and child maintenance, but capped at $750,000. Further, it provides that if either party should commence proceedings to set aside the agreement, or to claim spousal support other than in accordance with the terms of the agreement, then that party shall pay all the legal costs of the other party.

h. Article 16.3 provides that the agreement, its validity and interpretation, and the rights of the parties under it, shall be governed and construed under the laws of New York.

i. The Modification Agreement provides that on the first happening of an Event of Marital Dissolution, or the wife becoming a US citizen, the husband will transfer to the wife a one-half interest in the Miami apartment and the residence in Southampton, New York.

The disputes about the agreement

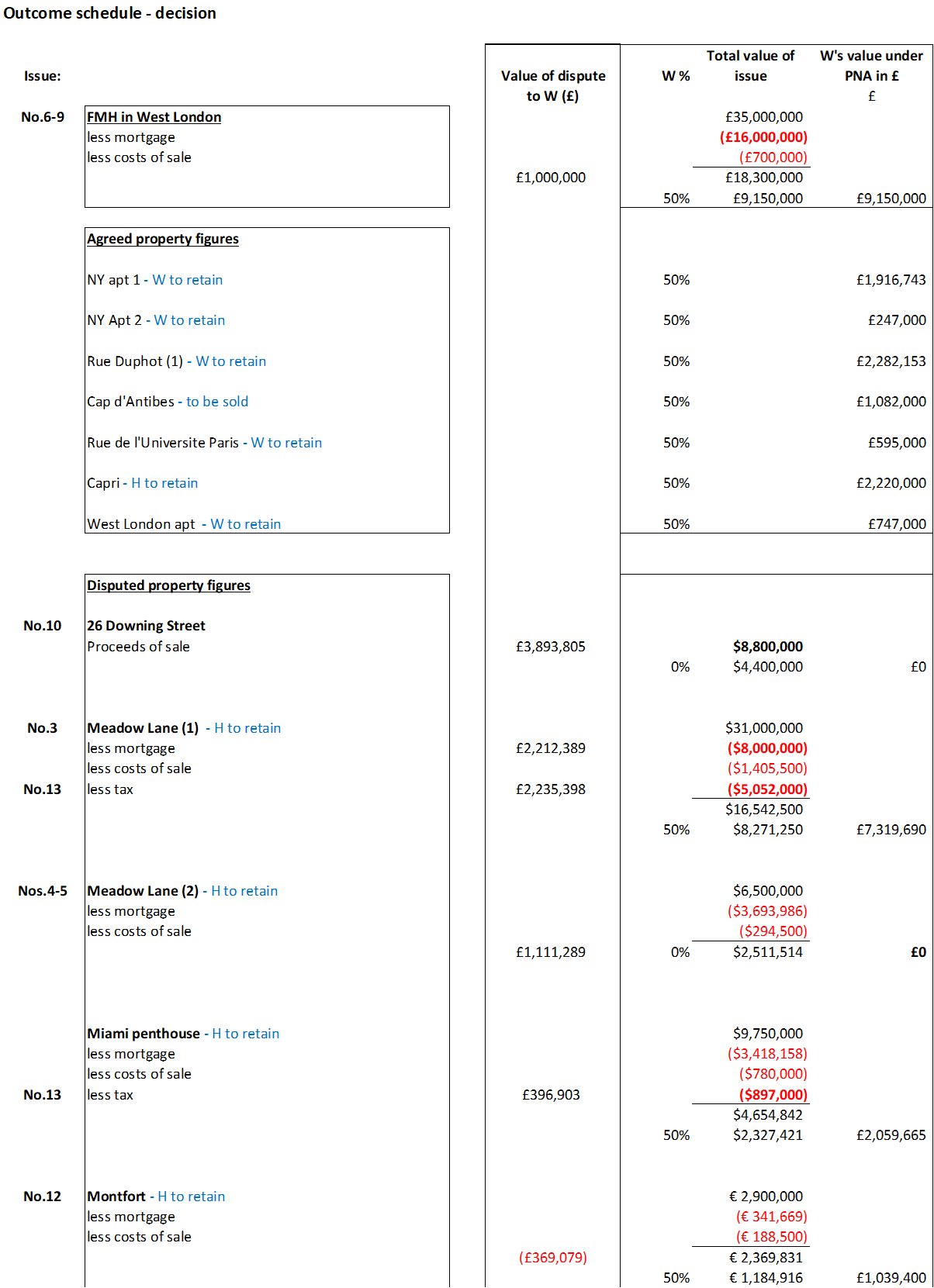

- Notwithstanding the detail and clarity of the modified agreement, there are numerous disputes between the parties as to its true meaning. I required the issues to be expressed narratively in a Scott Schedule and numerically in a spreadsheet (“the Outcome Schedule”).

- On the face of it there are 17 separate issues, although Issue 17 is nothing to do with the interpretation of the agreement. Further, I think that some of the issues are duplications. One issue was resolved by agreement on the last day of the hearing. I consider there are 10 separate issues, to which I now turn.

Issues 1 & 2: The failure by the husband to set up the Joint Investment Fund

- Article 6.1 provides for the establishment by the husband of a ‘Joint Investment Fund’ (“JIF”). The husband was to fund it and the parties were to share its growth and value equally.

- Specifically, Article 6.1 provides:

“Within three years from the date of the marriage, Michael shall establish, from his Separate Property assets, a joint investment fund (the “Joint Investment Fund”), in the name of both parties or in the name of an entity owned by both parties, with a minimum balance of Ten Million ($10,000,000) Dollars. Each party shall have a 50% interest in the Joint Investment Fund (with Alvina’s share vesting from the date of the marriage)…”

- Article 6.1.2 goes on to reinforce the provision made to the wife by the JIF to give her a guaranteed (or “floor”) amount depending on the length of the marriage.

- Specifically, Article 6.1.2(b) provides:

“If an Event of Marital Dissolution occurs after the establishment and full funding of the Joint Investment Fund and before the ten year anniversary of Michael’s management of the Fund, but in no event beyond the thirteenth anniversary of the parties’ marriage, Michael shall be entitled to the contents of the Joint Investment Fund, provided that he shall pay to Alvina a cash amount equal to the greater of (i) half the value of the Joint Investment Fund, or (ii) the cash sum of Five Million Dollars ($5,000,000) plus an amount equal to the product of (x) the number of full months the parties were married prior to the Event of Marital Dissolution up to a maximum of 120 months, and (y) $41,667. Such cash amount shall be paid to Alvina as a tax-flee distributive award payable as follows: (1) $1 million within ten days from the Event of Marital Dissolution; (2) an amount equal to the remaining sum due, less $1,500,000, within ninety days from an Event of Marital Dissolution; and (3) a payment of $500,000 each year on the first, second, and third anniversary of an Event of Marital Dissolution.”

- Thus, the Event of Marital Dissolution having occurred on 22 December 2020, the wife was to receive half the value of the JIF, or, if more, a sum calculated as follows: [$5,000,000 + (103 x $41,667) = $9,291,701]. This was payable as follows:

|

1-Jan-21 |

$1,000,000 |

|

22-Mar-21 |

$6,791,701 |

|

22-Dec-21 |

$500,000 |

|

22-Dec-22 |

$500,000 |

|

22-Dec-23 |

$500,000 |

|

$9,291,701 |

- However, unbeknown to the wife, the husband did not establish the JIF. His explanation was that he believed that the subsequent purchase by him in joint names of other properties pursuant to the Modification Agreement, and voluntarily, satisfied this obligation. He was wrong about that. He now accepts the advice from his New York attorney Allan Mantel who wrote on 20 June 2022 that the New York court would not accept that these property purchases constituted a substitute for the JIF.

- Much has been made by Mr Cusworth KC of the husband’s failure to establish the JIF but there is no numerical difference between the parties in relation to these issues in the Outcome Schedule. The entry for each party in that Schedule is $9,291,700. The wife’s position in the Scott Schedule is stated thus:

“Floor provision in PNA [is] only applicable as a floor. If needs require a greater sum in replacement, that is legitimate.”

- The husband’s position is that there is no evidence of any loss. In [11] above I gave the figure for the increase in the husband’s fortune from the date of the marriage until June 2021. That increase was 70.03%. If the husband had in fact established the JIF there is no reason to think that it would have increased at a rate markedly higher than the rate of increase of the value of the husband’s overall assets. An increase of 70.03% would mean that the JIF would have been worth $17,003,000 in June 2021, and in my opinion certainly no more today. The wife’s 50% share would thus be worth today no more than $8,501,500, rather less than the amount provided for by the “floor” of $9,291,700.

- I accept the husband’s submissions. The figure I use in the Outcome Schedule is $9,291,700. The husband’s breach of the agreement, while regrettable, is redressed by using that figure. There is no warrant for assessing the household needs for the purposes of the award of child support in a more liberal way than I would do otherwise because the husband failed to comply with that term of the agreement. The argument is a non- sequitur.

Issue 3: The mortgage on Meadow Lane (1), Southampton, New York

- This property was purchased by the husband in his sole name in September 2006 with a mortgage of $8 million. The mortgage now is $13 million. The wife correctly says that the $5m increase in the mortgage debt derives from a re-mortgage in 2016 when the husband raised a lump sum amount to pay off his first wife’s mortgage under a long-standing obligation in a court order.

- The wife’s position is that she did not agree to the re-mortgage. The husband’s position is that the wife did agree to it; that the debt to his ex-wife was genuine; and that there is no basis for artificially excluding the value of this re-mortgage. Mr Chamberlayne KC submits that this was not ‘wanton expenditure’ within the add-back jurisprudence.

- The original Article 6.6 provided:

“Southampton Residence. Michael is the sole owner of a house located at Meadow Lane, Southampton, New York (“the Southampton Residence”). In the event that the Southampton Residence is sold prior to an Event of Marital Dissolution, Michael agrees to pay to Alvina an amount equal to one-half of the excess of the net sales price (defined as the gross sales price less broker’s fees, transfer taxes, and customary closing costs, but not deducting any mortgage) of the Southampton Residence over $20 million, but in no event less than a minimum of $1 million. For example, if the Southampton Residence sold for a net sales price of $25 million during the marriage and prior to an Event of Marital Dissolution, Michael would pay to Alvina the sum of $2.5 million. In the event that Michael still owns the Southampton Residence at the time of an Event of Marital Dissolution, he shall pay to Alvina the sum of $1million within ninety days of such Event.”

This original agreement shows that the existence of a mortgage was recognised, although its value would not be taken into account in computing the wife’s relatively modest share of the proceeds of sale if the property were sold prior to the breakdown of the marriage. It also shows, on the facts as they have unfolded, that the wife would have got $1 million under this unmodified term in circumstances where the property has not been sold.

- As stated above, the Modification Agreement provided that Article 6.6 was amended to provide that the husband would on the earlier of the breakdown of the marriage, or the wife becoming a US citizen, transfer to her a one-half interest in this property. Nothing was said in the MA about any mortgage, but it was implicit that the wife’s half share would be subject to such mortgage as existed at the time the transfer took place. There was nothing in the MA freezing the mortgage at the level at which it stood at the date of its execution; there was nothing in the MA prohibiting the husband from, in accordance with his customary practice, mortgaging the property for his personal purposes. The wife knew perfectly well that it was the husband’s customary practice, indeed it was the very essence of his entrepreneurial spirit, to raise money on existing properties to fund investment in other projects or to meet his own personal needs. The wife was well aware of the husband’s fractious relationship with his first wife and the financial obligations under the order and, indeed, was a drafter of proposed emails to be sent to the first wife’s lawyers.

- These matters seem to me to favour taking the true mortgage position. On the other hand, on the basis that equity treats as done that which is agreed to be done, the husband is in effect requiring the wife to pay half of the lump sum raised to discharge his obligations under a divorce order to his first wife. Further, I am not satisfied that the wife knew about the raising of this re-mortgage in 2016 for this particular purpose. Indeed, Mr Cusworth KC demonstrated in his cross-examination of the husband, that he had not given a correct account in his witness statement where he said that the borrowing against Meadow Lane was used to meet living costs and improvements to the property as well as to meeting obligations to his first wife. On the contrary, the contemporaneous documents include a completion statement which shows quite clearly that the entirety of the re-mortgage money went to pay off the mortgage of the husband’s first wife.

- In my judgment, a reasonable interpretation of the Modification Agreement is to be gained by asking what the Commuter on the Bronx Subway would have said in answer to this question:

“Should the wife’s half share that was promised to her in 2014 in the Modification Agreement be depredated by a further mortgage to pay off her predecessor’s own mortgage? ”

I am convinced that such a reasonable person would say:

“It would be unfair, and therefore outside the contemplation of the parties, that such a further debt should be taken into account against the wife’s promised share.”

Therefore, the figure that I use in the Outcome Schedule for the mortgage against Meadow Lane (1) is $8 million.

Issues 4 & 5: Does the Modification Agreement cover Meadow Lane (2)?

- This next-door property was purchased by the husband in his sole name on 10 April 2014, a few weeks after the signing of the Modification Agreement on 23 March 2014. It is therefore not covered by it. It could only be covered by Article 6.7 of the PNA if the parties had lived in it as a primary or vacation residence, and they did not. Article 6.7 provides:

“Future Residences. In the event that either 26 Downing Street, the Paris Apartment, or the Miami Apartment are sold during the marriage and prior to an Event of Marital Dissolution, any residence (a) purchased as a residence in which the parties reside as a family either as a primary or vacation residence, or (b) purchased as an investment property but subsequently resided in by the parties as a family either as a primary or vacation residence, shall be titled in the joint names of the parties (or otherwise deemed jointly owned by the parties) with each party having a 50% interest in such property. Any other residences which the parties choose to put in joint names (or hold title through an entity in which both parties are members or partners) shall be considered to be equally owned by the parties, with such property to be sold upon an Event of Marital Dissolution and the net proceeds of sale equally divided.”

The parties never lived in this property as a vacation residence. Indeed, it was purchased in a derelict condition, no doubt with the intention of renovating it and perhaps incorporating it into the domain of the next-door property. But such plans were never put into effect, and it stands derelict to this very day. The wife claims that 50% of the value of the equity in that property, or around $1.25 million should be attributed to her. This is an argument bereft of merit. The figure of zero will be used by me in the Outcome Schedule.

Issues 6, 7, 8 & 9: Should the mortgage on the family home be taken at £18m or £16m?

- A great deal of forensic energy has been expended on this issue, and some quite serious allegations have been bandied around. Yet the sum at stake, so far as the wife is concerned, is £1 million. While this is objectively a large amount of money, it is but a small element of the overall value to which she claims she is entitled under the modified PNA.

- The family home in London was purchased for £30.2 million in 2017 in joint names. A mortgage of £19.6 million was raised with a five-year term. Of this, £4.53 million was to be repaid over the term at the rate of £940,000 per annum; the balance was interest only. All of this was arranged by the husband; such transactions were his meat and drink.

- In 2020, having made only two such capital repayments, the husband renegotiated the mortgage. The borrowing was increased, and a fresh five-year term was commenced. In so doing the interest-only element of the mortgage was reset at £18 million and the repayment element was reset at £4.5 million, now repayable up to 2025. The husband did not make a capital repayment in 2020. In this way he raised £4.6 million which was used to buy in his sole name an adjacent property to preserve the amenity of the family home.

- The wife says she did not consent to the remortgage; it was presented to her as a fait accompli. A great deal of time was spent scrutinising the wife’s signature on various documents, although these did not include the critical document, namely the formal legal charge (presumably in Form CH1), which would have been submitted to the Land Registry for registration.

- The wife is adamant that she did not sign the mortgage offer dated 23 January 2020. She says that the signature on that document, purportedly dated 24 January 2020, was not made by her. The husband is equally adamant that she signed it in his presence. I fear that his memory must be at fault because Mr Cusworth KC convincingly demonstrated that the wife did not sign that document.

- The evidence establishes that there was a practice within this family of proxies signing documents on behalf of the principals. The wife was well aware of this. Indeed, much to the surprise of all, in her oral evidence she averred that she did not sign the offer for the 2017 mortgage either. I have no reason to doubt that evidence. It showed that she was well aware that the 2017 mortgage documents had been signed on her behalf and that she condoned such practices.

- Mr Cusworth KC took the husband through the contemporaneous emails. These showed that on 3 February 2020 the bank emailed the husband saying that they needed the wife’s signature on the mortgage offer. At that time, the wife was in London and the husband was in New York. On the same day a member of the husband’s staff in New York replied to the bank saying “please find the document attached as requested. The original will be sent via FedEx today.” The document attached was the mortgage offer dated 23 January 2020, now bearing the wife’s signature purportedly made on 24 January 2020. It looks as if someone signed the mortgage offer on 3 February 2020 on behalf of the wife and backdated that signature to 24 January 2020.

- A similar conclusion is reached when consideration is given to the “cooling off” document purportedly bearing the signatures of the parties and dated 4 February 2020. The husband accepted that the date had been overwritten; it had originally given a date in January 2020. The husband accepted that the signature on the document was not made by him; he did not know if the other signature on the document purportedly made on the document by the wife was made by her. It certainly looks as if someone also signed that document on the wife’s behalf.

- The proxy-signing practice was also in use on 14 February 2020 when a “Deed of Confirmation” was purportedly signed by the wife in the “presence” of a witness (a member of the husband’s staff), who gave her address in New York City. It was also signed by the husband in the “presence” of another witness (another member of his staff) who gave his address in New York City. The husband said he did not know if he made “his” signature. The husband doubted that the wife was in New York on 14 February 2020. It would seem that she was not.

- It may well be the case that there has been proxy-signing of the wife’s signature on the three documents and that she did not sign any of them. However, if this did in fact occur, it is obvious that this was a practice condoned by her. That may account for her surprising inertia when the bank asked her for details of her allegation that her signature had been forged. On a number of occasions, the bank asked for evidence so they could investigate the matter properly. But the wife deliberately declined to cooperate in that investigation, with the result that the bank closed its enquiries. It seems to me that it is arguably an abuse of process - a procedural abuse - for the wife to raise this serious issue so late in the day in circumstances where she has eschewed the opportunity, in conjunction with the bank, to get to the bottom of it. Even now her position as stated in the Scott Schedule is a paradigm example of fence-sitting. She says:

“No finding is required as to whether or not W signed the re-mortgage documentation. It is clear from the evidence that no finding that she signed the documents is in any way possible.”

Yet the husband was very extensively and rigorously cross-examined by Mr Cusworth KC about this matter.

- However, in circumstances where the money raised by the re-mortgage has been used to purchase a neighbouring property in the sole name of the husband in which the wife will not share, and where it is clear that the wife did not actively participate in the raising of the mortgage, I am convinced that the Commuter on the Bronx Subway would be of the view that it would not be a reasonable interpretation of the agreement for her to have to share in the higher mortgage figure of £18 million. The figure that I will use in the Outcome Schedule is £16 million.

- In reaching that conclusion I make it clear that I am not making any positive findings of falsification against the husband.

Issue 10: Is the wife entitled to a credit of half the net sale proceeds of 26 Downing Street?

- Article 6.2 states:

“The parties acknowledge that Michael has signed a contract to purchase a townhouse located at 26 Downing Street, New York for a purchase price of $14.25 million, which the parties intend to utilize as their primary residence and which shall be considered a joint asset of the parties vesting at the date of closing. Michael shall be permitted to finance the purchase price by taking a mortgage on the property of up to $10 million. The contents of 26 Downing Street (or any replacement residence) shall also be considered the joint property of the parties, except for artwork which disposition shall by governed by paragraph 6.9 of this Agreement.”

- Article 6.2.1 states:

“Within thirty days from the occurrence of an Event of Marital Dissolution, if there are children of the marriage under the age of twenty-one, Alvina shall have exclusive occupancy and shall be permitted to remain in the 26 Downing Street (or if this property has been sold, in the parties’ then primary residence) until the youngest child of the marriage attains the age of twenty-one. Michael shall be responsible for making the monthly mortgage payments, payment of any real estate taxes, major repairs (subject to his being given the opportunity to arrange for such repairs), and maintaining at his expense the household staff (subject to a cap of $60,000 per year, not including a nanny, if applicable) for the 26 Downing Street (or equivalent payments for any replacement primary residence) during Alvina’s period of exclusive occupancy of the residence and Alvina shall pay all other expenses attendant to the primary residence. Alvina shall maintain the primary residence in reasonably good condition during the period of her exclusive occupancy. Upon the youngest child of the marriage attaining the age of twenty-one, the 26 Downing Street or any replacement primary residence then owned by the parties) shall be placed on the market for sale and the net proceeds of the sale, after the payment of the mortgage, broker’s fees, and all reasonable and customary clothing expenses, shall be equally divided between the parties. Michael shall not be entitled to a credit for paying down mortgage principal, if any, during Alvina’s exclusive occupancy of the residence (or otherwise).”

- When they signed the PNA on 2 March 2012 the parties were about to purchase their primary residence in Downing Street, New York for $14.25 million with borrowing of up to $10 million. They duly did so and lived there, as their primary residence until May 2017. It was sold on 25 July 2018, with net proceeds of sale of $8.8 million, 14 months after the purchase in May 2017 of the family home in London. That property was purchased for £30.2 million with a mortgage of £19.63 million, the husband putting in about £10.6 million of his own money.

- If Downing Street had been sold just before the purchase of the family home in London its net proceeds of $8.8 million would surely have been put towards the purchase price of that family home, with the husband providing that much less of his own money. It seems to me to be obvious, and in accordance with normal practice, that the proceeds of sale of the previous main family property would be put towards the purchase price of the new one. By the same token, if the new family property was in fact purchased shortly before the sale of the previous one, and bridging finance was obtained to enable that to happen, then the normal practice would be to use the proceeds of the previous home, when available, to discharge the bridging finance. It would not make any difference if the bridging finance was provided by a commercial lender, or (as here) by the purchaser using his other funds.

- I am certain that the Commuter on the Bronx Subway would say that of course the proceeds of Downing Street of $8.8 million should be treated as if they were used to purchase the London property.

- If that had happened, the husband would have put from his other funds that much less than the £10.6 million he in fact put towards the purchase of the London property. The wife’s interest in the equity of the London property would of course be the same, but that equity would encompass the proceeds of sale of 26 Downing Street. Accordingly, I agree with Mr Chamberlayne KC that were the wife to receive a credit for half the net proceeds of 26 Downing Street that would represent a double recovery. It would not reflect the fair interpretation of Article 6.2 that the proceeds of Downing Street of $8.8 million should be treated as if they were used to purchase the London property.

Issue 11: Should the wife be entitled to 100% or 50% of Rue Duphot Nos. 2 and 3?

- Article 6.3 provides:

“Paris, France Apartment. The parties currently hold joint title to an apartment located at Rue Duphot, 75001, Paris, France (the “Paris Apartment”). There is no mortgage on the Paris Apartment and neither party shall encumber the Paris Apartment without the express written consent of the other party. The Paris Apartment shall continue to be jointly owned by the parties, with each party having equal decision-making authority concerning the property, through an Event of Marital Dissolution. Upon the occurrence of an Event of Marital Dissolution, Alvina shall receive sole title, ownership and occupancy rights to the Paris Apartment and the contents thereof (excluding artwork, the disposition of which is covered in paragraph 6.9 herein) and Michael waives any rights therein and thereto. Michael shall execute all documents necessary to transfer title of the Paris Apartment to Alvina as soon as is practicable following an Event of Marital Dissolution (and shall be responsible for any and all taxes or other expenses associated with such transfer, if any) and Alvina shall retain sole and exclusive ownership of the property and shall be entitled to dispose of the property in any way she deems appropriate.”

At the time of the PNA, the parties held jointly one apartment at Rue Duphot (“Rue Duphot (1)”), and there is no dispute that it goes to the wife under the PNA. It is agreed between the parties that she will retain that property. However, on 2 October 2017 a second apartment at Rue Duphot (“Rue Duphot (2)”) was purchased in joint names for €575,000 with a mortgage of €510,000. And on 16 October 2018 a third apartment at Rue Duphot (“Rue Duphot (3)”) was purchased in joint names for €870,000 with a mortgage of €600,000. Rue Duphot (2) and (3) adjoin Rue Duphot (1) and the three apartments are in the process of being knocked together to create one magnificent apartment.

- The wife’s case is that a reasonable interpretation of Article 6.3 is that its terms should cover any property adjoining Rue Duphot (1) which is purchased with the intention of conjoining Rue Duphot (1) with it. The problem with that interpretation is that the parties purchased the adjoining apartments in joint names. If they had intended them to be knocked together with Rue Duphot (1) they could easily have purchased those adjoining apartments in the wife’s sole name. At [40] above I set out the terms of Article 6.7 concerning future residences, which I repeat for convenience:

“Any other residences which the parties choose to put in joint names (or hold title through an entity in which both parties are members or partners) shall be considered to be equally owned by the parties, with such property to be sold upon an Event of Marital Dissolution and the net proceeds of sale equally divided.”

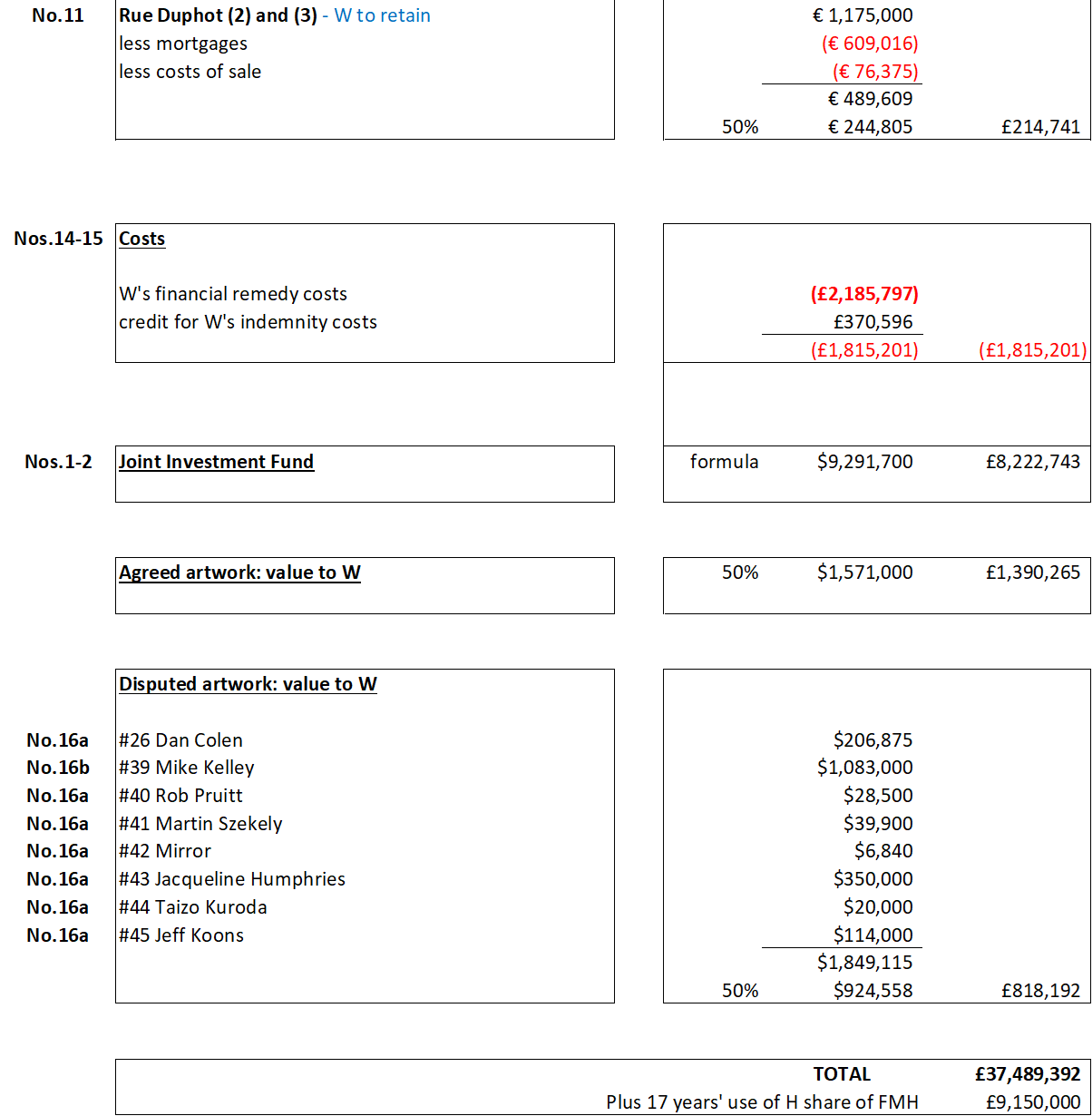

I cannot see how this does not exactly deal with Rue Duphot (2) and (3). The parties have agreed that these apartments will be retained by the wife. The value that the wife will receive under the PNA in relation to these apartments is half of their anticipated net proceeds of sale or €244,805, and that is the figure I will use in the Outcome Schedule.

- As the wife will retain the apartments, she has to give credit for the value of the husband’s half share. The parties are agreed on which properties will be retained by the wife, and their advisers will bring into account all the relevant credits and debits when calculating the money or money’s worth to be provided to the wife by the husband under the PNA.

Issue 12: Montfort

- There was an issue about another French property called Montfort. The issue related to its value in circumstances where the wife is going to retain it. There was no dispute that whatever its value, half would be attributed to the wife under the agreement. However, on the final day of the hearing it was agreed that the husband will now retain this property and that the value attributed to it will be €2.9 million, rather than the lesser figure provided by the Single Joint Expert. I will therefore use the agreed figure of €1,184,916 for half of the net proceeds in the Outcome Schedule.

Issue 13: Latent tax

- It is agreed that there is latent US capital gains tax on the Southampton residence (Meadow Lane (1)) in the sum of $5,052,000 and on the Miami penthouse in the sum of $897,000.

- The husband argues that in accordance with authority and convention, these latent taxes should be allowed when calculating the net proceeds of sale which will be shared with the wife when calculating her entitlement under the PNA. The wife argues that this is completely unreal because the husband will never pay such taxes, not least because he has millions of dollars of unused losses which he will be able to apply to extinguish the tax liability were he ever to sell the properties. The husband’s response is that a tax loss is no different from cash in the bank. Money is fungible, and it can take many shapes and forms. His tax loss is an asset, a chose in action, just as real as a piece of property or money in the bank. The PNA does not require him to use cash to reduce debt on properties, and so by parity of reasoning he should not be required to use an asset, namely a tax loss, to reduce a specific debt on the two properties namely latent taxes.

- In White v White [2001] 1 AC 596, Lord Nicholls stated at 612:

“Finally, Mrs White criticised the use of net values, arrived at after deducting estimates of the costs and capital gains tax likely to be incurred if the farms were sold. Mr White still owns and uses the farms. The farms have not been sold. Counsel submitted that the use of net values in this situation should be discontinued. I do not agree. As with so much else in this field, there can be no hard and fast rule, either way. When making a comparison it is important to compare like with like, so far as this may be possible in the particular case. In the present case a comparison based on net values is fairer than would be a comparison of Mrs White' cash award and the gross value of the farms. Under her award Mrs White will have money. She can invest or use it as she pleases. Mr White's equivalent, as a cash sum, is the net value of the farms. The farms have to be sold before he can have money to invest or use in other ways. What will be his financial position if he is able to retain the farms or parts of them? Will he better off financially? Dairy farming is currently languishing in the doldrums. On the evidence there is no reason to suppose that the farms are likely to yield a better financial return at present than the investment return to be expected if Mr White sold up and invested the net proceeds.”

- From this dictum a convention has arisen whereby latent tax which cannot be avoided, and which will likely be payable when a property is sold, is almost invariably deducted when computing the value of a property to go on the asset schedule. For example, in DR v GR & Ors (Financial Remedy: Variation of Overseas Trust) [2013] EWHC 1196 (Fam) at [50](iv) I stated:

“Fourth, the figure for capital gains tax presupposes a distribution of all the assets to the beneficiaries. Although the normal rule as stated in White v White [2001] 1 AC 596 is that latent capital gains tax should be allowed the court must nonetheless be realistic. I consider it reasonable to allow this latent sum but I will bear in mind that it may be a long time before any such tax is paid by the husband (or anyone else) and that in the meantime the husband will continue to have the use of the assets.”

- However, in K v L [2010] EWHC 1234 (Fam) [2010] 2 FLR 1467 Bodey J held:

“57. Mr. Pointer's submission is that latent CGT (estimated at over £10 million, mostly in respect of the S Ltd shares) should not be taken off the gross value of the assets. This is because the shares are held offshore and as he (rightly) submits they need never be brought onshore, thus attracting CGT. The wife accepted this in cross-examination. She can readily meet her claimed outgoings as per paragraph 30 above out of the S Ltd dividends remitted into this country and subjected to tax here, without touching the capital. Further, the wife told me in terms of her wish and intention to leave the shares to the children, just as they originally came to her. She has no significant capital needs, as she is completely content with her present home, which has quite recently been fully renovated.

58. Miss Stone submits that CGT should clearly be taken off, as is the entirely conventional practice in these cases. This is because the wife should be entitled to access her resources how she likes, as and when she might wish to do so. That includes remitting the proceeds to this jurisdiction, in which case she would have to pay CGT. So the only way to compare like with like is by the use of 'after CGT' figures across the board.

59. Clearly it is forensically advantageous to the wife for the gross value of the assets to be reduced by the incidence of the latent CGT (and by taking the date of separation to value the shares) because the husband's award would represent a greater proportion of the whole. Conversely, it is forensically advantageous for the husband for latent CGT not to be taken into account (and for the shares to be taken at today's value) as his award would then represent a correspondingly smaller proportion. Lord Nicholls dealt with the CGT point in White v. White above, when he said:

"Counsel submitted that the use of net values in this situation should be discontinued. I do not agree. As with so much else in this field, there can be no hard and fast rule, either way. When making a comparison it is important to compare like with like, so far as this may be possible in the particular case."

60. Given the wife's clear evidence about her wishes and intentions regarding the S Ltd shares, coupled with the modest way in which she has lived for her entire life, I agree with Mr. Pointer that the likelihood of her ever actually having to pay out significant amounts of CGT on them is a very modest one. It would require a volte-face in respect of both her stated intentions and her historic lifestyle. Accordingly, if this issue were an important one (which I do not think it is) I would not be inclined to deduct CGT on the entirety of the wife's holding. Equally, however, in the fullness of time and as things turn out, she may wish to bring some of her fortune into this jurisdiction, as she has done on some occasions in the past, thus attracting CGT on the proportion remitted. There is no way of anticipating this in any informed way. So taking a broad brush, I would deduct latent CGT on an arbitrary £10 million worth of her shareholding, but would not deduct it from the balance of the share holding. I consider that this discretionary although speculative approach is open to me, as there is 'no hard and fast rule' and because I think it is the best way to produce a fair and realistic determination on the issue, given the unusual facts of this particular case. The gross kitty therefore reduces in size accordingly.”

- I made similar comments in BJ v MJ (Financial Remedy: Overseas Trusts) [2011] EWHC 2708 (Fam), [2012] 1 FLR 667 where I said:

“69 This list does not include the asset and liability referable to C's business referred to above at para 30. Nor does it include, contrary to Mr Castle's arguments, the tax that H would pay were he to receive all the assets and remit them here. This is completely unreal. The whole point of the structure is to avoid paying tax, and H has never remitted any offshore income. Mr Castle argues that not to include it would result in an unfair imbalance as W would be able to remit onshore and would therefore have more freedom with, or at least fewer strings attached to, her money. But in order to have the benefit of the money here H does not need to remit income.”

- In my judgment the usual convention should apply here. This is not a case where the court is blinding itself to a truth that a party will never pay such latent tax because he has entered into arrangements the whole object of which is to avoid paying that very tax. In this case the taxes are very real, and the husband will have to pay them with money or with other assets in the shape of tax losses. The wife would be given very short shrift if she suggested that the calculation of the net value of these two properties should ignore the latent taxes because the husband has money in the bank and could just pay off the taxes. I agree with Mr Chamberlayne KC that there is no difference in principle or substance between the husband paying a tax debt in cash or eliminating it by deploying a loss.

- Accordingly, I take the above latent tax figures of $5,052,000 and $897,000 into account in my calculations. The result is that the Outcome Schedule will show the net proceeds of the Southampton residence to be $16,542,500, of which the wife is entitled to half - $8,271,250 - under the PNA. And it will show the net proceeds of the Miami penthouse to be $4,654,842, of which the wife is also entitled to half or $2,327,421.

- Following circulation of this judgment in draft I have been informed by junior counsel for the wife that the Outcome Schedule failed to reflect costs of sale and latent tax on two properties to be retained by the wife namely an apartment in New York and Rue Duphot (1). I have now been given the omitted figures. It has not been explained to me why the Outcome Schedule was wrong. Nevertheless, there is no reason to believe that the new information is inaccurate and I have therefore adjusted the Outcome Schedule to show the correct net value of those two properties.

Issues 14 and 15: Should any of the wife’s legal costs paid by the husband be reimbursed to him?

- Article 13 provides, so far as is relevant to this case:

“Legal Fees and Indemnification in Event of Suit to Enforce

13.1 Upon the occurrence of an Event of Marital Dissolution, Michael shall be responsible for Alvina’s reasonable legal and expert fees (such legal fees to be provided by one partner and one associate at a law firm of Alvina’s choosing) necessary to resolve all outstanding issues between the parties through entry of a decree dissolving the marriage, including, but not limited to any legal or expert fees related to child custody and access issues and child support, with Michael’s share of such fees not to exceed the sum of $750,000.

13.2 If either party commences an action or proceeding to set aside or vacate this Agreement in whole or part or obtain distribution of property, or spousal support, other than as provided in and consistent with the provisions of this Agreement, then in such event that party shall be responsible for paying all of the other party’s reasonable attorneys’ fees and costs incurred in defending against such action or proceeding provided that such action proceeding, counterclaim or defense results in a decision, judgment, decree or order dismissing or rejecting said claims.”

- The husband’s stance is based on a very literal reading of these provisions, which I do not believe that the Commuter on the Bronx Subway would consider was a fair reflection of the mutual intention of the parties. The husband says that in the Children Act proceedings he has paid the wife’s costs in the sum of £2,337,122. He relies on a letter written on 12 August 2021 where his then solicitor wrote:

“My client does not expect your client to pay her legal fees on the [Amex] card and he shall therefore pay them directly upon receipt of the invoice (accepting the detailed time narrative which is likely to accompany the invoice is privileged and will not be provided). I will be writing separately in due course in relation to legal fees in any event, as whilst my client will continue to meet them he is only doing so in accordance with the parameters of the nuptial Agreements with which I am sure you are familiar.”

Accordingly, the husband says that the cap of $750,000 or £663,717 should apply and the wife should therefore be required to reimburse him to the tune of £1,673,405 (i.e. £2,337,122 less £663,717). To achieve this the husband says the wife must give credit for £1,673,405 in the calculation of the value to be received by her under the PNA by placing a negative figure in that amount in the column in the Outcome Schedule headed “W’s value under PNA in £”.

- I have no doubt that, inasmuch as this term is relied on to add back costs incurred and paid by the husband in the Children Act proceedings, it should be construed with the concept of fairness at the forefront of my mind. The first point to be made is that the limitation of $750,000 is completely arbitrary. I am not setting out in this judgment, which will be made public, the findings of the circuit judge. I will merely point out that to have this arbitrary cap in place irrespective of what future litigation about the welfare of the children might entail has the potential to be extremely unfair. Further, there is nothing in the agreement to prevent the husband paying the wife’s legal costs of the children proceedings on a voluntary basis over and above the capped figure of $750,000. Indeed, it is clear to me that is what he has done, and he has gone on to proclaim his largesse to the circuit judge. On 4 April 2022 his leading counsel stated to the circuit judge:

“We have a situation now where, if nothing substantial changes on an interim, my client is left pretty much where he was for another eight weeks, in circumstances where your Honour will know that he, and he alone, is paying for the costs of these proceedings.”

And on 1 July 2022 his (different) leading counsel stated to the circuit judge:

“This is a billionaire father who is paying nearly now £1 million in maintenance per year to the mother, plus all the house bills, plus all the school bills, and all the legal fees to the mother. There is no order that was required for him to do that.”

- In my judgment it would be grossly unfair for these provisions to be relied on to require the wife to reimburse the husband with her Children Act costs paid by him, and I decline to do so. I am satisfied that the husband represented to the circuit judge that he was paying the wife’s costs with no strings attached. His solicitor’s letter of 12 August 2021 was overreached by those representations.

- The husband’s stance in relation to the financial remedy costs is even more relentless. He says that the wife must give credit not only for her financial remedy costs of £2,185,797 which he has paid, but also for his financial remedy costs of £2,128,972. One of the reasons for such high costs was the husband’s woeful non-compliance with his voluntary agreements to pay costs and all outgoings, and latterly with his obligation under my maintenance pending suit order to pay a monthly allowance and to discharge all outgoings. I had to deal with enforcement applications on two occasions on each of which I made an order for indemnity costs against the husband.

- The husband does not seek to escape that costs liability which he accepts in the full amount of £260,601 claimed by the wife for those hearings. He therefore seeks under the terms set out above a credit in the Outcome Schedule of £2,185,797 + £2,128,972 - £260,601 = £4,054,168.

- In my judgment it would be grossly unfair, on the facts of this case, for the wife to be required, in effect, to pay the husband’s indemnity costs of these proceedings. I reach that conclusion having regard to the general rule as set out in FPR 28.3(5) of no order as to the costs of a final financial remedy hearing. That general rule can be displaced under FPR 28.3(7)(a) - (e) by reference to the conduct of the parties, but there has been no relevant conduct on the part of the wife justifying its displacement. I therefore flatly refuse to reach a conclusion about the meaning of the PNA which has the effect of requiring the wife to pay the husband’s costs on the indemnity basis.

- On the other hand, I cannot see any good reason why the wife should not pay her own costs of the financial proceedings with credit for the orders for costs which she has obtained. In addition to the £260,601 already mentioned the wife argues that I should make an order in her favour for her costs of the maintenance pending suit proceedings, which were reserved to me at this final hearing. The wife’s Form N260 for that hearing states that she incurred costs of £109,995. Following the distribution of this judgment in draft I have been informed by the wife’s junior counsel that there were further costs not captured in her Form N260 for the maintenance pending suit hearing totalling £44,692. No explanation was given as to why these costs were omitted from the form. I am not prepared to enlarge the husband’s liability on the basis of this late submission. It is not acceptable that the Form N260, endorsed with a statement that the costs did not exceed the stated amount, should have been inaccurate. It is in order to emphasise the imperative necessity of Form N260 being completed accurately that I make a different decision on the includability of this new figure to the one I made in relation to latent tax under [71].

- FPR 28.3(4)(b)(i) provides that an application for maintenance pending suit is not covered by the no-order-for-costs general rule in FPR 28.3(5). The wife plainly prevailed on that application and is entitled to her costs of it. In my judgment those costs should be assessed on the indemnity basis because the husband’s conduct leading up to that hearing, and his stance at that hearing, took the case “out of the ordinary”. That is the criterion which I apply when considering whether an order for costs should be made on the indemnity basis. I am required under CPR PD 44 para 9.1 to consider making a summary assessment and I do so in the sum of £109,995.

- Accordingly, in my judgment the wife should pay her own costs in the financial remedy proceedings. This means that she must “reimburse” the husband with the sum he has paid of £2,185,797 less the value of the orders for indemnity costs which I have made in the sum of £370,596. This means that the negative figure of £1,815,201 is used in the Outcome Schedule.

Issue 16: Disputed artwork

- Article 6.9 provides:

“Artwork. The parties acknowledge that they have purchased certain items of artwork together prior to the marriage, which they hereby consider to be their joint property. These items include works of art by Tracy Emin, Candida Hofer, David Sherry, Terence Koh, and photographs by Yul Brenner. The parties acknowledge that Michael has gifted a Marc Chagall painting to Alvina prior to the marriage and this painting shall be considered Alvina’s Separate Property for purposes of this Agreement and Alvina has gifted a Kirshner drawing to Michael which shall be considered Michael’s Separate Property for purposes of this Agreement.

Any other artwork purchased (or received by exchange) in the joint names of the parties during the marriage, or by a business entity in which each party is a member, and prior to an Event of Marital Dissolution, shall be considered the joint property of both parties. Upon the occurrence of an Event of Marital Dissolution, all artwork defined as the joint property of both parties shall be valued by a mutually agreed upon appraiser and divided between the parties in as equal a manner as possible, with the party receiving a greater value of artwork paying any sums necessary to the other party so as to equalize the values, subject to any financing attributable to such art or any loans which the parties have agreed in writing were used to acquire such art. For example, if the total value of the artwork considered to be the joint property of the parties at the time of an Event of Marital Dissolution is $5 million and, after dividing the various pieces of artwork between them, Michael has $3 million worth of art and Alvina has $2 million worth of art, Michael shall pay to Alvina the sum of $500,000 so as to equalize the value of the property being divided.”

Under this provision, for a work of art to be “considered” as joint property, it must have been bought in joint names. This suggests a degree of formality in the acquisition which simply was not present. All of the art was purchased in the name of the husband, but he does not take any point about that. The schedule of art has 45 items on it. 32 of the items are mutually agreed by the parties to be jointly owned. Three are agreed to be gifts from the husband to the wife. One item is agreed to be owned exclusively by the wife. One item (number 28 on the schedule) is agreed by the wife to have been a gift from her to him (notwithstanding that he maintains it is jointly owned). This leaves eight items where there is a dispute. For seven of these items the wife says they are jointly owned while the husband says that they are his alone. For one item the husband says that it is joint while the wife says it is hers alone.

- Under cross-examination there was this exchange between the husband and Mr Cusworth KC:

“A. …There is no "we". There is never any emails from Alvina where she basically express ownership in any of these pieces. So ... you can't just go around and ask for ownership, because you're going with somebody in a store, in a gallery and buy a piece of art and you say, "I like it". I mean this is where I feel the cost element of this -- I feel it is abusive, because it's against common sense. Either you own it or you don't own it. At least a point where you say: I have ownership of this art.

Q. What happened to the first 34 items on the list then, Mr Fuchs? Why are they, as you accept, jointly owned?

A. Because I gave them to her and I was saying that to her.

Q. You gave them to her?

A. Yes.

Q. As gifts?

A. No, as where we bought them together and we have consents, but I feel I'm acting here a little bit like a hungry crocodile. The more you offer and the more you give, the more you are asking.

Q. Forgive me, Mr Fuchs, your art portfolio in 2019 was worth £29 million, wasn't it, very valuable, and these are only tiny pieces around the edge; yes?

A. Yes.

Q. So we are not talking about somebody biting your arm off to grab large chunks of your portfolio. We are talking about a few pieces that she says she was particularly interested in and bought with you and discussed with you while you were married?

A. Yes, and this.”

- The husband was unable to explain to me why, if the great majority were recognised as being jointly owned, these seven items were different. In his final submissions, Mr Cusworth KC stated that he would not resist a finding by me that all of these items were jointly owned.

- In my judgment this is a particularly sterile dispute given that the parties have agreed how the pieces will be physically distributed. The parties are battling for me to make findings purely for personal financial advantage.

- In my judgment there is no solid evidence showing why the eight disputed items should be treated any differently to the 32 items where there is no dispute that they are to be treated as joint items.

- I therefore rule that the eight disputed items are all to be treated as jointly owned with the result that half of their value will be used in the Outcome Schedule. The wife seeks the sale of the Mike Kelley piece as she believes that its value is more than the $1,083,000 in the expert’s report. I decline so to order. Its value will be taken at $1,083,000, and it will be retained by the husband.

Issue 17: Compensation for stolen jewellery

- Issue 17 is whether the husband should pay the wife €300,000 compensation for the theft of her jewellery. I do not understand how this matter has been allowed to arise as an issue in this phase of the proceedings. It has nothing to do with the construction of the PNA.

Conclusion on the wife’s entitlements under the modified PNA

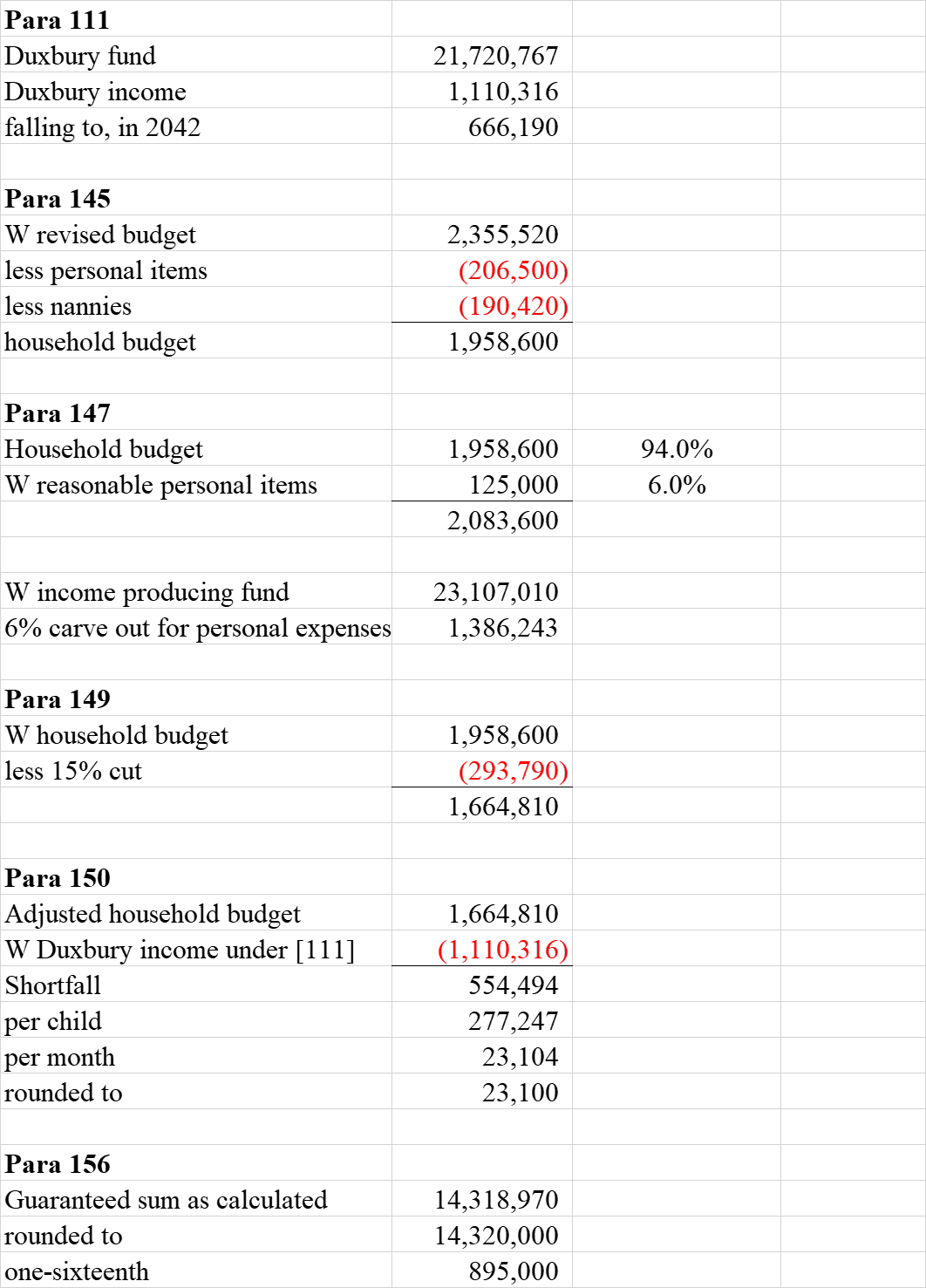

- Schedule 1 contains the Outcome Schedule incorporating my rulings. The total value which must be provided to the wife pursuant to the terms of the modified PNA is £37,489,392. In addition, the wife has 17 years’ use of the husband’s share in the family home worth £9.15 million.

- The parties are agreed as to how assets should be distributed and will work out the cash payment that needs to be made by the husband to the wife to reflect my decision.

- In addition to her entitlement of £37,489,392 under the PNA the wife seeks further payments of £750,000 as a refurbishment fund for the family home; €300,000 compensation for stolen jewellery (as mentioned above); and £450,000 as a form of parachute payment to ease her transition to a standard of living which she says will be several levels below that which she has enjoyed hitherto. These applications are misconceived. They are in plain breach of the terms of the PNA which the wife accepts as binding. They are refused.

- The sum of £37,489,392 is the cornerstone of my calculations set out below of the sum to be received by the wife to fund her household. It must therefore be received by the wife net in her hand and not be depredated by tax. To the extent that he had not done so already the husband must indemnify the wife in respect of any taxes that may arise in respect of any transfers of property or other assets into her sole name.

- Once the wife has received her full entitlement under the PNA the parties’ remaining claims for financial remedies will be dismissed on the clean break basis in life and in death (although the husband being domiciled outside England and Wales there is no possibility of a claim under the Inheritance (Provision for Family and Dependants) Act 1975).

The wife’s capital needs

- In this phase of my decision, I need to calculate how much the wife will have as a Duxbury fund on the assumption postulated by Mr Cusworth KC on her behalf, namely that the family home in London aside, all the assets distributed to her under the modified PNA are to be treated as cash to provide for her capital needs, with the residue furnishing a Duxbury fund.

- I therefore turn to examine the wife’s reasonable capital needs.

- She intends to stay in the family home until B is 21 pursuant to her entitlement under Article 6.2.1. The husband will be paying the instalments on the actual mortgage which is of course more than the deemed figure of £16 million which I have ruled is to be used in the Outcome Schedule. Therefore, the parties’ lawyers need to agree figures to ensure that the wife receives money or money’s worth of £28,339,392, being her PNA entitlement of £37,489,392 less the deemed value of her half share in the family home of £9,150,000. The values of all the items in question having been either agreed or ruled on by me, it will be a very simple task to add up the values of the items being distributed to the wife and to subtract that figure from £28,339,392, to give the residual sum to be paid by the husband to the wife in cash.

- As mentioned above, the wife says she needs £750,000 for refurbishment costs of the family home. She also says she needs £165,000 for a car fund. She says she needs £6 million to buy a holiday home. There was no oral evidence about these claims. The husband does not accept any of them.

- In my view the claims for refurbishment costs and for a car fund are reasonable capital needs of the wife, which she should pay from her own funds. Given the standard of living enjoyed during the marriage it is not unreasonable for the wife to acquire a holiday home from her own funds. I take a figure of £4 million for this purpose. I am sure that it will be clearly appreciated that while it is reasonable for the wife to spend her own capital for these purposes (with a consequential reduction in her Duxbury income) it is completely unreasonable that the husband should directly pay for any of them.

- It is also necessary for the wife to pay her outstanding costs of £317,382. This leaves the sum of £23,107,010, calculated as follows:

|

Value to wife under PNA |

37,489,392 |

|

less FMH |

(9,150,000) |

|

28,339,392 |

|

less unpaid costs |

(317,382) |

|

less refurbishment fund |

(750,000) |

|

less car fund |

(165,000) |

|

less holiday home |

(4,000,000) |

|

Income producing fund |

23,107,010 |

- For the reasons given below at [147] the wife should reasonably be expected to use 94% of this fund, or £21,720,767, as a Duxbury fund to meet the needs of her household. She should be entitled to carve out 6% of this fund, or £1,386,243, to meet her own personal needs unconnected to her role as primary carer of the children..

The reasonable annual income to be derived from the wife’s Duxbury fund

- My next step is to undertake a reverse Duxbury calculation on £21,720,767 to see how much income it will generate for the wife to put towards the cost of running her household.

- For the purposes of this reverse calculation, I apply four assumptions:

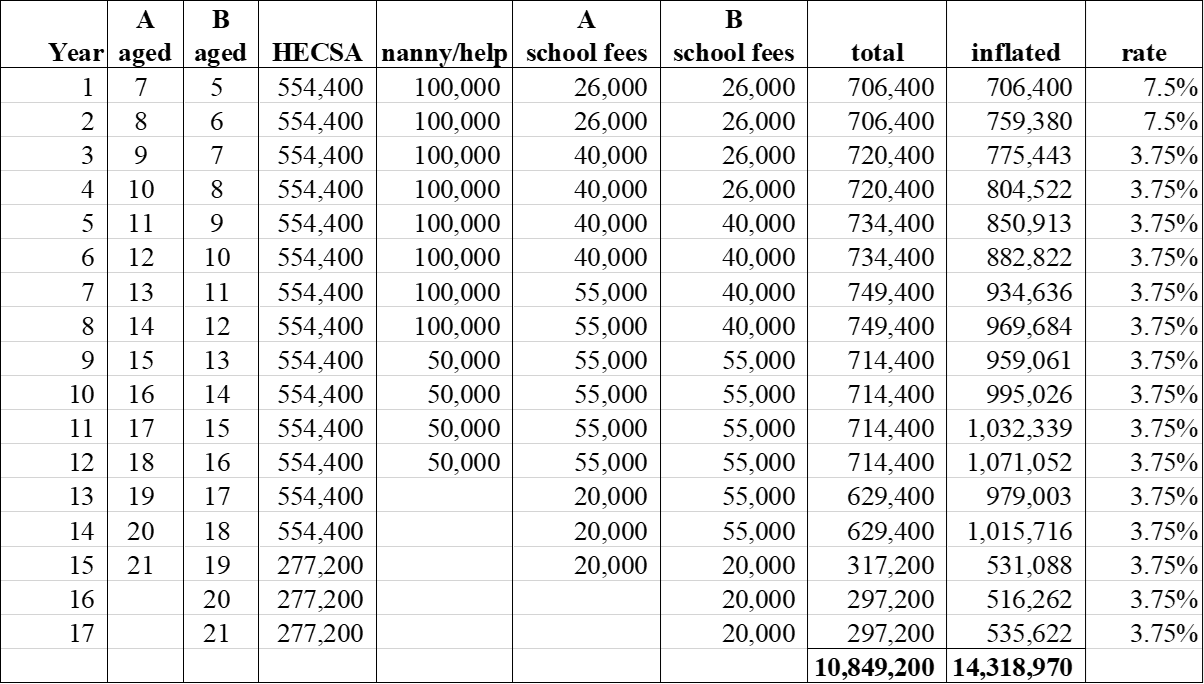

a. full amortisation of the fund during its 40-year existence to 2062;

b. no state pension;

c. in 2039, when the occupation of the family home comes to an end on the younger child attaining 21 years of age, an injection of £4 million (in today’s money) into the fund, as the wife will not then be needing as much as £13.15 million (again, in today’s money) in housing funds; and

d. in 2042, a 40% reduction in income at age 67 on retirement (as suggested by Mr Cusworth KC).

- In applying these assumptions, I follow my own decision in CB v KB [2019] EWFC 78. In that case the wife was 45. I said this:

“53. Notwithstanding the relatively young age of the wife I consider it reasonable to work on the whole-life provision implicit in the Duxbury formula. This was a long relationship and there have been six children born. It is reasonable in such circumstances for the wife to be provided for until the end of her life. It is pre-eminently reasonable that the wife should be required to amortise - that is to say, to spend - her Duxbury fund. Indeed, I struggle to conceive of any case where in the assessment of a claimant’s needs it could be tenably argued that it was reasonable for her not to have to spend her own money in meeting them. After all, that is what money is for. The endgame of the contrary argument is that it would be reasonable for a respondent to have to fund a claimant’s testamentary ambitions. I cannot conceive of any case where that could be said to be reasonable.

54. The wife’s home is very large. She accepts that it would be reasonable for her to downsize in her autumn years. In my judgment it would be reasonable for her to release equity of £1.5 million when she reaches the age of 60. Moreover, at that point it is reasonable for her spending to reduce by a third. After all, virtually everybody moving into retirement and onto a pension has to reduce their spending.”

- As to the amortisation issue, I remain puzzled by the proposition that says it is a mere fact-specific question whether the provision by one spouse to meet the needs of the other spouse could include meeting a “need” to leave money to testamentary beneficiaries. In my opinion, it is a clear matter of principle. Accordingly, where a wife has received a substantial sum under a sharing or compensation claim, or under a PNA, it is hard to conceive that it would ever be reasonable to expect a husband to top up that sum to enable the wife to keep her capital intact to leave to testamentary beneficiaries.

- I suggest that this is entirely consistent with Lord Nicholls’ well-known passage in White v White [2001] 1 AC 596 at 609 under the heading “The next generation”, where he said:

“I agree that a parent's wish to be in a position to leave money to his or her children would not normally fall within paragraph (b) as a financial need, either of the husband or of the wife. But this does not mean that this natural parental wish is wholly irrelevant to the section 25 exercise in a case where resources exceed the parties' financial needs. In principle, a wife's wish to have money so that she can pass some on to her children at her discretion is every bit as weighty as a similar wish by a husband. A Duxbury type fund is intended to provide money for living expenses but not more. … In my view, in a case where resources exceed needs, the correct approach is as follows. The judge has regard to all the facts of the case and to the overall requirements of fairness. When doing so, the judge is entitled to have in mind the wish of a claimant wife that her award should not be confined to living accommodation and a vanishing fund of capital earmarked for living expenses which would leave nothing for her to pass on. The judge will give to that factor whatever weight, be it much or little or none at all, he considers appropriate in the circumstances of the particular case.”

- In that momentous case the long-standing criterion of resolving cases solely by reference to the reasonable requirements of the claimant was overturned, but no firm alternative technique was enunciated other than the criterion of fairness (at 589) and the application of the yardstick of equality as a check against the possibility of discrimination (at 605).

- What Lord Nicholls was saying is that while a claimant’s wish to leave money to her testamentary beneficiaries is not a reasonable need for the purposes of s. 25(2)(b) of the Matrimonial Causes Act 1973, the court may yet grant her an enhanced award enabling her to do so on application of the then protean criterion of fairness.

- It was not until the decision of the House of Lords in Miller v Miller, McFarlane v McFarlane [2006] 2 AC 618 that the concept of “sharing” as an element or strand of the requirement of fairness emerged. The three elements - sharing, needs and compensation - constituted compendiously the fairness requirement. Therefore, the claimant’s testamentary wish, which Lord Nicholls in White had left to a protean general “fairness” discretion on the part of the judge, now has to be accommodated within the sharing principle. Logically, it is only there that it can find expression. If a claimant has earned a right to share equally (or unequally) in the marital acquest, then what she receives is her money and what she does with it is her business alone. It only becomes the other party’s business if the claimant argues that her needs exceed her sharing entitlement and that she therefore requires her sharing entitlement to be topped up to meet those needs. The needs in that scenario cannot, as Lord Nicholls explained in White, encompass a testamentary wish.

- There is another reason in this case why full amortisation is clearly appropriate. Article 5.1 of the PNA provides:

“Based on each party’s assets, income, earning potential and the distribution of property each will receive pursuant to the terms of this Agreement, each party does hereby acknowledge that he or she has or will have ample financial resources to be self- supporting throughout his or her life and, therefore, each party does hereby waive, relinquish and release his or her rights to permanent maintenance or temporary maintenance, permanent alimony or temporary alimony, lump sum alimony, “quantum meruit alimony” or other permanent or temporary support of any kind from the other in the event the parties separate, divorce, annul or otherwise terminate their marriage to each other, as prescribed or authorized by the common law or any statute, including, without limitation, New York Family Court Act Article 4 and New York Domestic Relations Law Section 236, Part B(6), any amendment or successor thereto, or the similar law of any jurisdiction within or without the United States.”

Now, it is perfectly true that the preamble to the PNA states that while the agreement is in full satisfaction of all rights arising on divorce, it does not deal with issues relating to child support (see [22(a)] above). The wife’s claim before me is for child support, albeit for that type of child support permitted by the law (as I will explain) whereby the reasonable costs of her household, including herself, will be met by the husband to the extent that they are not capable of being met by her. This award will literally amount to “support of any kind … in the event the parties divorce” within the terms of Article 5.1, albeit, as a child support award, it is excepted from its operation. But I do not think that Article 5.1 can be ignored. What it implies is that if a claimant is seeking what I will call a Household Expenditure Child Support Award (“a HECSA”) then it is incumbent on the claimant to spend her own money in funding her household before she looks to the other party to meet, or contribute to, that cost. And spending her own money means being treated in the calculation of the other party’s liability, as amortising fully her Duxbury fund.

- In any event, the wife will, at the appointed time for her to expire, have unspent housing capital of £9.15 million in today’s money, which will on any view provide her children, even after the depredation of inheritance tax, with a very substantial inheritance. Further, I do not overlook the fact that these children will probably receive inheritances of vast size upon the demise of their father.

- A reverse Duxbury calculation on a capital sum of £21,720,767 for a woman aged 47 applying the assumptions set out above, provides a net of tax income of £1,110,316 per annum in today’s money until 2042 when it will fall by 40% to £666,190, again in today’s money.

The wife’s child maintenance claim

- I shall first examine the applicable legislation and the case-law.

- An unsecured child maintenance award may be made under the following statutes:

a. for any child, whether marital or non-marital, under paragraph 1(2)(a) of Schedule 1 to the Children Act 1989;

b. for a marital child, under s. 23(1)(d) of the Matrimonial Causes Act 1973 (where the child’s parents were divorced in England and Wales) or under s.17(1)(a)(i) of the Matrimonial and Family Proceedings Act 1984 (where the parents were divorced overseas).

I do not need to consider the power to award unsecured child maintenance under the Domestic Proceedings and Magistrates’ Court Act 1978.

- The award in each case is discretionary. The criteria governing the exercise of the discretion is similar, but not identical, under the statutes.

- Under Schedule 1, para 4(1):

“The court shall have regard to all the circumstances including:

(a) the income, earning capacity, property and other financial resources which each [parent] has or is likely to have in the foreseeable future;

(b) the financial needs, obligations and responsibilities which each [parent] has or is likely to have in the foreseeable future;

(c) the financial needs of the child;

(d) the income, earning capacity (if any), property and other financial resources of the child;

(e) any physical or mental disability of the child;

(f) the manner in which the child was being, or was expected to be, educated or trained.”

- Under s. 25(3) of the 1973 Act:

“the court shall in particular have regard to the following matters:

(a) the financial needs of the child;

(b) the income, earning capacity (if any), property and other financial resources of the child;

(c) any physical or mental disability of the child;

(d) the manner in which he was being and in which the parties to the marriage expected him to be educated or trained;

(e) the considerations mentioned in relation to the parties to the marriage in paragraphs (a), (b), (c) and (e) of subsection (2) above.”

Those considerations in s.25(2) are:

(a) the income, earning capacity, property and other financial resources which each of the parties to the marriage has or is likely to have in the foreseeable future, including in the case of earning capacity any increase in that capacity which it would in the opinion of the court be reasonable to expect a party to the marriage to take steps to acquire;

(b) the financial needs, obligations and responsibilities which each of the parties to the marriage has or is likely to have in the foreseeable future;

(c) the standard of living enjoyed by the family before the breakdown of the marriage;

(e) any physical or mental disability of either of the parties to the marriage;

- Section 18(4) of the 1984 Act provides:

“As regards the exercise of those powers in relation to a child of the family, the court shall in particular have regard to the matters mentioned in section 25(3)(a) to (e) of the 1973 Act.”

Thus, the criteria under the 1973 and 1984 Acts are identical. They differ from Schedule 1 in that under the 1973 and 1984 Acts the court is specifically directed to have regard to the standard of living enjoyed by the family before the breakdown of the marriage, and to any physical or mental disability of either of the parties to the marriage. These factors are not explicitly mentioned in Schedule 1, para 4(1) although they would no doubt fall for consideration under the general rubric of “all the circumstances”.

- A further difference is that, unlike a child maintenance claim under the 1973 or 1984 Acts, the court under Schedule 1 is not expressly required to give first consideration to the welfare of the child. This is of no significance. In J v C (Child: Financial Provision) [1999] 1 FLR 152 Hale J explained at [156]: